Wall Street's Crypto Arms Race: Morgan Stanley Files MSBT, Nasdaq Gets Tokenized, Bitcoin Holds $70.5k on Quadruple Witching Day

On the biggest derivatives expiry day of the first quarter, Bitcoin is quietly outperforming gold, Morgan Stanley filed its spot BTC ETF with ticker MSBT, the SEC just greenlighted Nasdaq's tokenized securities plan, and the Crypto Clarity Act is one Senate committee hearing away from reshaping the entire industry. The Wall Street pivot is no longer a future event. It's a Friday morning in March 2026.

Today is Quadruple Witching Day. Every quarter, on the third Friday of March, June, September, and December, stock index futures, stock index options, single-stock options, and single-stock futures all expire simultaneously. What gets added to the March 2026 edition: roughly $600 million in Bitcoin deep out-of-the-money put options also rolling off today, most of them positioned at $20,000 - a bet on catastrophic downside that never arrived.

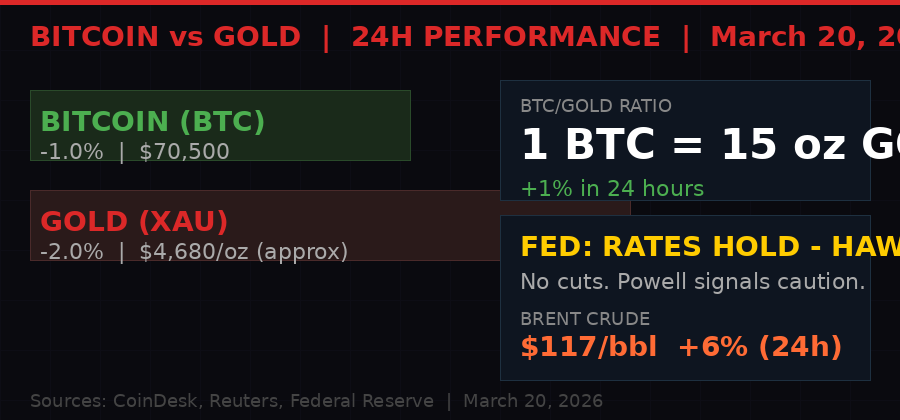

Instead, Bitcoin is sitting at $70,500. And it is doing something genuinely unusual on this particular witching day: it is outperforming gold.

The macroeconomic backdrop is ugly by any measure. Brent crude oil is trading above $117 per barrel, up more than 6% in 24 hours driven by the ongoing Middle East conflict. The Federal Reserve delivered a more hawkish-than-expected tone at Wednesday's meeting - no rate cuts coming, and Chair Powell's language pushed back hard against market expectations for imminent easing. The Nasdaq 100 ETF (QQQ) fell 0.5% in premarket. Crypto-related equities - Strategy (MSTR), Galaxy Digital (GLXY), Coinbase (COIN) - all red before the open.

But Bitcoin? Down 1%. Gold is down 2%. One bitcoin now buys 15 ounces of gold. And while that may sound like a small gap, the ratio moving in Bitcoin's favor during a genuine risk-off episode is a significant data point for anyone watching institutional behavior.

Backdrop settled. Now let's talk about what actually matters today.

Morgan Stanley Files MSBT: The Last Big Wall Street Holdout Moves In

Morgan Stanley set a ticker and $1 million in seed capital for its spot Bitcoin ETF this week. The ticker is MSBT. That seed capital number is symbolic - virtually every new ETF launches with nominal seed capital before institutional money flows in - but the filing itself is the signal. One of the three largest asset managers in the world, overseeing roughly $1.5 trillion in assets, is now formally in the Bitcoin ETF race.

For context: Morgan Stanley was notably cautious when the first wave of Bitcoin ETFs launched in January 2024. BlackRock's IBIT and Fidelity's FBTC launched to massive inflows, accumulating a combined $50+ billion in assets within their first year. Morgan Stanley's wealth management clients were reportedly restricted from proactively pitching the products to clients for months - advisers could only respond if clients asked first.

That caution is gone. The MSBT filing signals that Morgan Stanley's compliance and regulatory teams have cleared the path. More importantly, it signals that the firm has watched $50 billion flow into competitors' Bitcoin products and decided the cost of staying on the sidelines exceeds the reputational risk of Bitcoin's volatility.

Wall Street BTC ETF Landscape - March 2026

The Morgan Stanley move also matters for the $117 trillion global wealth management market. Wealth advisers at major brokerages now have cover to allocate client portfolios into Bitcoin through a regulated wrapper. That distribution pipeline is the real unlock - not the $1 million in seed capital in the filing.

What happens when a firm managing $1.5 trillion starts routing even 0.5% of portfolio allocations into Bitcoin? That is $7.5 billion in demand. This is not an academic question. We have already watched it happen with BlackRock. MSBT makes it happen again, with a different client base.

Strategy, Galaxy, Coinbase All Fell Pre-Market - Does MSBT Compete with Them?

Short answer: yes, and that is partly why crypto-adjacent equities are under pressure. Every dollar that flows into a regulated ETF is a dollar that does not need to go through a proxy vehicle like Strategy (MSTR) or a crypto exchange like Coinbase. The direct access ETF structure removes the premium investors were paying for Bitcoin exposure through equities. MSTR traded at a 2x+ premium to Bitcoin NAV for most of 2024. As ETFs proliferate, that premium compresses.

For Coinbase specifically, the threat is more nuanced. Galaxy and Strategy are positioning plays. Coinbase earns revenue on trading volume and - critically - from its USDC stablecoin arrangement with Circle. That second revenue line is now directly in the crosshairs of Washington.

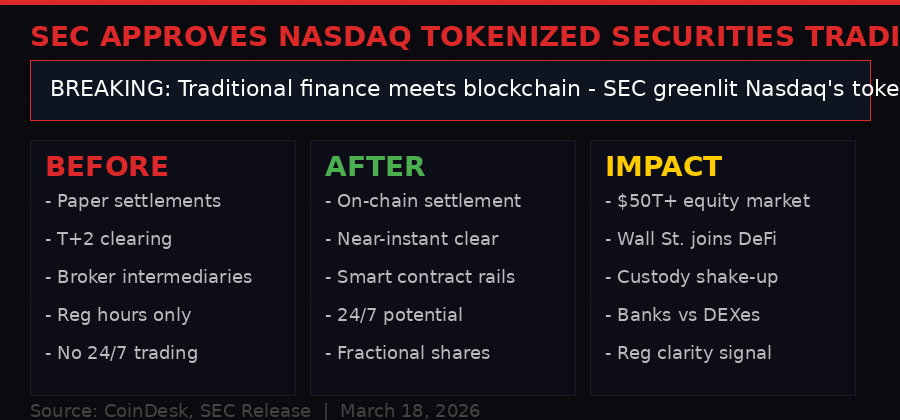

SEC Greenlights Nasdaq Tokenized Securities: The $50 Trillion On-Chain Migration Begins

Two days ago, on March 18, the Securities and Exchange Commission approved Nasdaq's proposal to support tokenized securities trading. This is a bigger deal than the headlines suggest, and it's being somewhat drowned out by the daily oil-and-Fed noise.

Tokenized securities are traditional financial instruments - stocks, bonds, ETFs - represented as tokens on a blockchain. The concept has been piloted by institutions for years in sandbox environments. JPMorgan has its Onyx platform. Goldman Sachs ran experiments on Digital Asset's DAML framework. BlackRock tokenized a Treasury fund on the Ethereum blockchain through its BUIDL product.

But the SEC's approval of Nasdaq's move is different. Nasdaq is not a pilot. Nasdaq is the second-largest stock exchange in the world, with over 3,000 listed companies and $25 trillion in total market cap. When Nasdaq integrates blockchain settlement rails, it does not remain a sandbox. It becomes infrastructure.

"This is the moment when tokenization stops being a buzzword and starts being a clearing mechanism. Every broker-dealer, every custodian, every fund administrator in the U.S. just got a direct mandate to figure out their on-chain strategy." - industry analyst reaction cited in CoinDesk coverage

What the approval enables in practical terms: Nasdaq-listed securities can now be issued, transferred, and potentially settled using distributed ledger technology under an SEC-approved framework. The T+2 settlement cycle - which has been a friction point in equity markets for decades - comes under pressure. Near-instant settlement becomes a legitimate regulatory path. Fractional share ownership at the institutional level becomes programmable.

For the crypto ecosystem, the implications cut multiple ways. First, it validates on-chain financial rails as legitimate market infrastructure - not just DeFi speculation. Second, it creates a direct commercial case for public blockchains (or private forks of them) in institutional finance. Ethereum, Solana, Avalanche, and purpose-built chains like Berachain all benefit from the legitimacy signal. Third, it puts decentralized exchanges and DeFi protocols in direct competition with regulated, SEC-backed tokenized market venues. That is a harder regulatory position to hold when you are operating on the same technical rails but without the compliance wrapper.

The custody question is particularly live. Who holds the private keys for tokenized Nasdaq securities? If it is a traditional custodian - BNY Mellon, State Street - they need crypto-native key management infrastructure. That is a multi-billion dollar service contract opportunity. If it is a crypto-native custodian - Coinbase Custody, Anchorage - they need to meet institutional-grade compliance standards that most were not built for originally.

The approval also lands at an interesting moment geopolitically. The EU's MiCA framework is already live. The UK is drafting its own crypto asset regime. Japan and Singapore have had frameworks for years. The SEC's Nasdaq move signals that the U.S. is no longer content to watch foreign jurisdictions establish the on-chain financial infrastructure standard. This is the shot across the bow at London and Frankfurt: American capital markets are going on-chain, and they are going to do it at Nasdaq scale.

Quadruple Witching: What $4.5 Trillion in Expiries Does to Bitcoin

Quadruple Witching gets its name from the chaotic, unpredictable price action that typically occurs when four types of derivatives expire simultaneously. The term dates to the 1980s when the simultaneous expiry of futures and options on indices was enough to move markets by 2-3% in a single afternoon session.

Today - March 20, 2026 - is that day for Q1. The four expirees: stock index futures (S&P 500, Nasdaq 100, Russell 2000), stock index options, single-stock options, and single-stock futures. The estimated notional open interest at expiry runs into the trillions. Some analysts peg Q1 2026 witching day open interest at approximately $4.5 trillion in combined notional exposure.

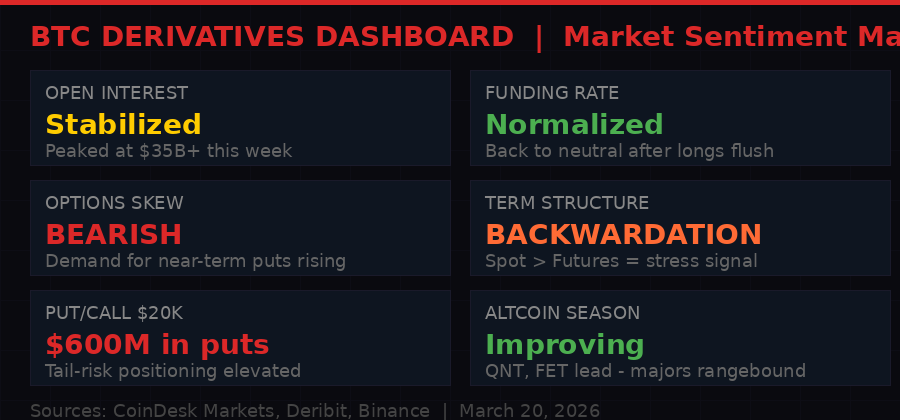

For Bitcoin, the connection is more mechanical than it might appear. The largest quarterly BTC options expiry of Q1 also falls today. CoinDesk reported that the $20,000 put option is currently the third most popular strike price ahead of today's expiry, with nearly $600 million in deep out-of-the-money puts highlighting what analysts call "tail-risk positioning." This is not a bearish directional bet. Professional options traders use deep OTM puts as portfolio insurance - paying a small premium for protection against a catastrophic drawdown that almost certainly won't happen.

When these puts expire worthless today - as they almost certainly will, with BTC at $70,500 - that $600 million in premium paid to sellers of those puts flows as profit to market makers. Market makers then delta-hedge their books, which can create mechanical buying or selling pressure depending on their net positioning. Today, with Bitcoin sitting above every major put strike, the delta-hedging dynamics favor buyers.

Q1 2026 BTC Options Expiry Snapshot

The broader derivatives picture, per CoinDesk's morning analysis, shows the market in a cautious-but-stable posture. Funding rates normalized after the recent long flush. Open interest has stabilized. The options skew has shifted toward put demand for near-term contracts, signaling that traders are hedging against further downside in the immediate term. The term structure is in backwardation - spot price higher than futures - which is historically a signal of near-term uncertainty rather than long-term bearishness.

QNT and FET are the altcoin outliers today, leading gains as the altcoin season index ticks up despite the majors sitting rangebound. This is consistent with late-cycle altcoin accumulation patterns: when BTC dominance holds steady but spot BTC is choppy, capital rotates to higher-beta plays.

Crypto Clarity Act: Senate Hearing Coming, Coinbase's Billions on the Line

While markets are focused on the witching hour, Washington is running its own slow-motion drama. The Crypto Clarity Act - the most comprehensive attempt to establish a regulatory framework for digital assets in U.S. history - is inching toward a Senate committee hearing. CoinDesk reported Thursday that the White House may be reviewing fresh legislative text, and lawmakers are weighing cross-deals with banks involving unrelated legislative provisions in exchange for their support.

Senator Cynthia Lummis, speaking earlier this week, said the discussion "is down to nuance" and that the bill will emerge from her committee in April. Senator Tim Scott confirmed market structure negotiations are advancing, with stablecoin yield language potentially drafted as soon as this week.

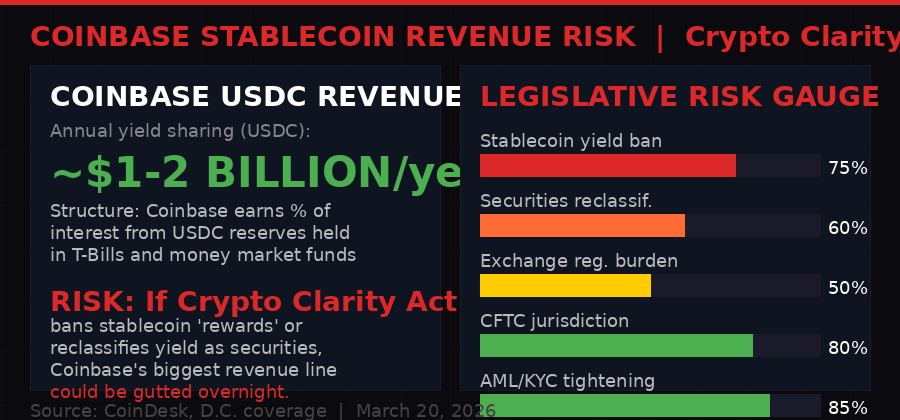

The stablecoin yield question is the one that matters most for Coinbase's balance sheet. Here is the structure: Coinbase earns a percentage of the interest generated from USDC reserves. Circle - the issuer of USDC - holds those reserves primarily in short-term U.S. Treasuries and money market funds. At current Fed funds rates (5.25-5.5%), that arrangement generates an estimated $1-2 billion per year in revenue for Coinbase.

The legislative risk: if the Crypto Clarity Act defines that yield-sharing arrangement as a "securities" activity, or bans stablecoin issuers from passing yield to distribution partners, Coinbase's single largest revenue line could be restructured or eliminated. CoinDesk notes that a "rewards loophole" in the current legislative draft may protect this revenue - but the language is still being negotiated. The risk is real and the dollar amount is enormous.

Crypto Clarity Act Key Provisions

Also in the legislative mix: an appeals court this week cleared the way for Nevada to temporarily ban prediction market Kalshi. The Ninth Circuit Court of Appeals denied Kalshi's legal effort to stave off an expected temporary restraining order from the state of Nevada. This is part of a broader state-vs-federal jurisdictional fight over whether prediction markets are financial products (CFTC jurisdiction) or gambling (state jurisdiction). The Supreme Court has not weighed in. The fight will escalate.

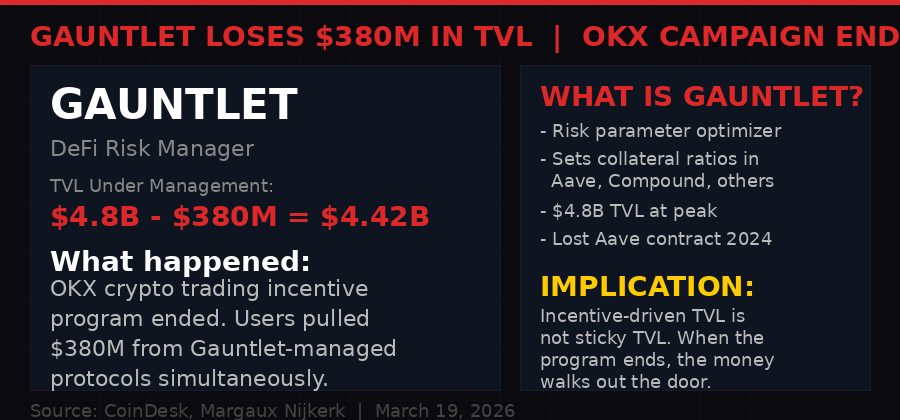

Gauntlet Loses $380 Million as OKX Campaign Ends: DeFi's Fake TVL Problem

DeFi's dirty secret got a very public airing Thursday. Gauntlet - the risk parameter optimization firm that manages collateral ratios and liquidation thresholds for protocols including Aave and Compound - saw $380 million in total value locked exit its managed protocols when OKX ended its crypto trading incentive campaign.

To understand why this matters, you need to understand what Gauntlet actually does. Gauntlet does not hold your money. It sets the rules for how much collateral you need to post to borrow, what triggers a liquidation, and how aggressive lending protocols can be with their risk parameters. Think of it as the actuarial firm for DeFi - it runs the math on how much risk a protocol can take before it breaks.

At its peak, Gauntlet managed risk parameters for protocols controlling $4.8 billion in TVL. That number just dropped by $380 million in a single cycle. The reason is mechanical: OKX ran a promotional campaign that paid users to deposit assets in specific DeFi protocols. Those users were not there for the yield on their collateral. They were there for the OKX incentive tokens. When the campaign ended, they left.

This is mercenary capital, and DeFi has a severe case of it. TVL figures across the sector are chronically inflated by incentive programs that attract deposits which have no intention of staying. Protocols report headline TVL numbers that look healthy. Then the campaign ends and the number collapses by 8-15% overnight. Real TVL - capital deposited by users who actually want to use the protocol's core functionality - is substantially lower than headline figures suggest for most protocols.

"The problem isn't Gauntlet. The problem is that $380M was sitting in these protocols because OKX was paying people to put it there. That's not TVL. That's a subsidy. And every DeFi protocol doing the same thing has the same time bomb ticking." - DeFi analyst commentary, March 19, 2026

For Gauntlet specifically, the OKX exit adds to a difficult stretch. In 2024, Gauntlet lost its contract with Aave, the largest DeFi lending protocol, after a governance dispute. That exit cost Gauntlet significant TVL and revenue. The company has worked to rebuild with other protocols, but the OKX exit demonstrates the fragility of TVL built on third-party incentive programs rather than organic user demand.

The broader implication for DeFi investors: when evaluating a protocol, ask how much of its TVL is genuinely sticky. Strip out incentive-driven deposits, liquidity mining yields that are paying users to be there, and cross-protocol borrowing loops. What you are left with is the real number. For many protocols, that real number is 30-60% lower than the headline TVL suggests.

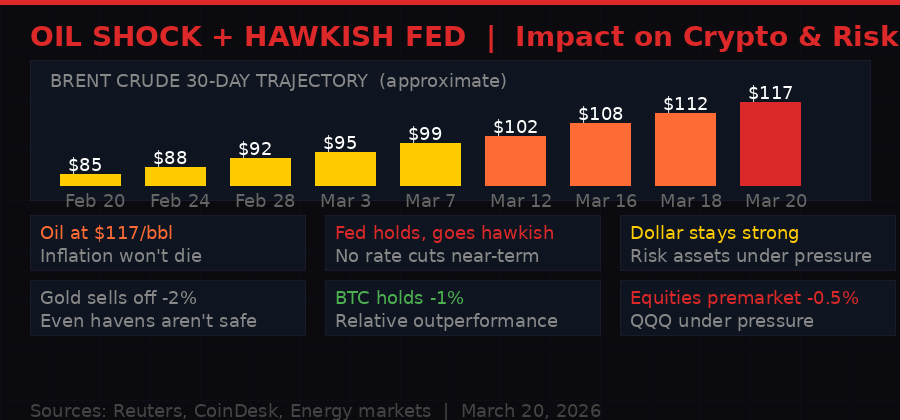

Oil at $117, Hawkish Fed, Stagflation Trap: What It Means for Crypto in Q2

Let's address the macro compression directly. The Federal Reserve held rates steady at its March meeting. That was expected. What was not fully expected was the hawkishness of the language accompanying the decision. Jerome Powell and the FOMC pushed back explicitly against market expectations for rate cuts, citing persistent inflation and - implicitly - the oil price surge as a complicating factor.

Oil at $117 per barrel is an inflation problem. Brent crude has moved from approximately $85 in late February to $117 today - a 37% surge in roughly 30 days driven by the escalating Middle East conflict and fears of supply disruption. That kind of energy price move feeds directly into CPI through gasoline, transportation costs, and industrial input prices. It also widens the gap between Brent and West Texas Intermediate (WTI) to levels not seen since 2013, signaling genuine global supply chain disruptions.

The Fed's reaction function is now caught in a stagflation trap. Inflation is being pushed higher by oil, which the Fed cannot control with interest rates. Growth is being squeezed by the same oil shock and by the weight of 5.25-5.5% rates that have been in place for over a year. Cutting rates helps growth but feeds inflation. Holding rates fights inflation but risks recession. There is no clean exit.

For Bitcoin, this macro environment is complex to read. The traditional narrative says Bitcoin should fall in a risk-off, high-rate environment - it is a speculative asset and rates create competition from safe yield. That narrative has clearly broken down somewhat, given that BTC is outperforming gold on a day when literally everything is selling. The Bitcoin/gold ratio improvement is not a fluke - it reflects genuine institutional allocation flows that are less sensitive to the daily rate narrative than retail traders are.

The more important dynamic for Q2: if oil stays above $100 and the Fed genuinely cannot cut, the dollar remains strong, and global equity markets stay under pressure. In that environment, Bitcoin's behavior depends heavily on whether it continues to attract institutional flows as a non-sovereign store of value (bullish), or whether risk-off deleveraging forces institutions to sell their most liquid, most volatile holdings first (bearish). The current week has leaned toward the former. Sustained pressure could tip it toward the latter.

Q2 2026 Macro Risk Matrix for Crypto

The Venus Aftermath: When DeFi Protocols Knowingly Ignore Red Flags

The Venus XVS exploit from March 16 deserves more analytical attention than it has received in the daily noise. The governance token dropped 9% Thursday as the full picture emerged. Let's go through what actually happened, because this is not a typical DeFi hack.

The attacker spent nine months accumulating a large position in Thena's THE token. Nine months. That accumulation was funded with 7,400 ETH withdrawn from Tornado Cash - a mixing protocol that obscures transaction origin. The attacker then donated more than 36 million THE tokens directly to the vTHE contract, bypassing normal cap checks and lifting the market's exchange rate by approximately 3.8 times. Using that inflated paper value as collateral, the attacker borrowed other assets and bought more THE in a thin market, pushing THE from $0.26 to near $0.56.

When the attacker unwound the position, THE dropped more than 17% in less than a day. Liquidations followed. Analysis by PeckShield puts the value extracted before liquidations at $3.7 million to $5.8 million. The protocol was left with $2.15 million in bad debt - loans it can no longer recover from the collateral pool.

Here is the governance failure that makes this case particularly damning: Venus's own community had flagged the attacking address before the incident. Community members identified the suspicious accumulation pattern, the Tornado Cash funding, and the unusual position size. Venus reviewed the flag and took no action, stating - and this is direct from Venus's own post-incident communication:

"Venus is a decentralized protocol. As a permissionless protocol, we cannot and should not freeze or blacklist addresses based on suspicion alone. This is a tension inherent to DeFi, and one we take seriously." - Venus Protocol, post-incident statement

That statement is technically correct. It is also a description of a known attack vector that was allowed to proceed to completion. The philosophical commitment to permissionlessness, while genuine, has a direct dollar cost: $2.15 million in bad debt that Venus's risk fund will now have to cover through governance vote.

The Venus exploit joins a growing list of cases where DeFi protocols flagged potential exploits in advance and failed to act because acting would require "centralizing" the protocol. Euler Finance, Mango Markets, Aave's CRV concentration risk - all had on-chain warning signs. Some were acted on. Many were not. The pattern suggests that DeFi's governance model, as currently implemented, is systematically unable to respond to slow-moving, sophisticated attacks that do not obviously violate protocol rules until they are already profitable for the attacker.

Venus paused THE borrows and withdrawals after the event, cut THE's collateral value to zero, and tightened rules on markets identified as at-risk - including BCH, LTC, AAVE, and others. The stable closing of the barn door after the horse has left is the most common post-exploit response in DeFi, and it remains deeply unsatisfying as a risk management framework.

Where Bitcoin Goes From Here: The $70k Floor Test

Every analyst with a Bitcoin take this week is watching the same level: $69,000-$70,000 as a support zone. CoinDesk reported that BTC slipped below $70,000 on Wednesday when the Fed delivered its hawkish hold and oil spiked. It recovered. It is back at $70,500 this morning.

The price action is mimicking the November-January pattern that preceded a slide to $60,000, per CoinDesk technical analysis. That pattern showed weak conviction among "buy the dip" buyers - capital showing up to defend levels but without the velocity needed to sustain a breakout. The current setup looks similar: BTC is holding but not accelerating. The bid exists. The aggressive buyer is not.

What changes the trajectory in the near term:

Bullish catalysts: Morgan Stanley MSBT goes live and draws early institutional inflows. Oil drops below $100 on ceasefire news, removing the Fed's inflation cover for hawkishness. The Crypto Clarity Act clears committee and signals regulatory certainty, unlocking pension fund allocations. Quadruple witching expires without the volatility spike many feared, giving the market a clean technical reset.

Bearish catalysts: Oil pushes toward $120, forcing the Fed to explicitly signal no cuts in 2026. Equity markets enter a correction, triggering deleveraging that hits crypto as the most liquid risk asset. A major DeFi exploit (post-Venus) spooks institutional capital. Legislative setback on Crypto Clarity Act - the stablecoin yield provision fails, creating uncertainty about Coinbase and Circle's business models.

The derivatives market is pricing near-term caution. The long-term structural case - Morgan Stanley filing, Nasdaq tokenization, growing corporate treasury adoption, shrinking BTC supply from mining halving effects - remains intact. These two realities can coexist for weeks or months. Bitcoin at $70,500 on Quadruple Witching Day 2026 is not a crisis. It is a stress test. The question is whether the bids below $69,000 are deep enough to absorb whatever selling the macro environment produces before the next wave of institutional capital finds its entry.

The answer to that question will be clearer by Sunday. Watch the weekly close.

Timeline: March 2026 Crypto-Finance Convergence

The structural story of March 2026 is not one event. It is the convergence of multiple institutional legitimization signals arriving simultaneously while macroeconomic pressure tests the market's resolve. Morgan Stanley's MSBT filing. The SEC/Nasdaq tokenization approval. The Crypto Clarity Act approaching a Senate floor vote. Bitcoin outperforming gold on Quadruple Witching Day. Each of these would be notable in isolation. Together, they describe an industry in the middle of a transformation from speculative asset class to institutional infrastructure.

The DeFi sector has a separate set of problems - mercenary TVL, permissionless governance exploits, the Gauntlet exit illustrating how quickly incentive-driven liquidity evaporates. Those problems are real and not resolved by the institutional story playing out in Washington and on Wall Street. Both can be true at the same time: TradFi is running toward crypto, and DeFi's internal governance is still failing in predictable ways.

Where do we land at end of day? Quadruple Witching will clear, the puts will expire worthless, the market makers will unwind their hedges, and Bitcoin will either hold $69,000 or it won't. The weekly close will set the technical tone for Q2. Everything else - Morgan Stanley, Nasdaq tokenization, the Crypto Clarity Act - is the backdrop for a market that is genuinely more institutionalized than it was twelve months ago, and genuinely more complex to navigate as a result.

Watch oil. Watch the weekly close. Watch what Morgan Stanley's wealth advisers tell their clients on Monday morning.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram