Strategy Crosses 761,000 BTC as Miners Bleed Out and the Fed Prepares to Speak

Michael Saylor dropped another $1.57 billion into Bitcoin last week. Metaplanet raised $255 million in Tokyo to race toward 210,000 BTC. Corporate bitcoin holdings just hit an all-time record. Meanwhile, the people who actually mine the coins are getting crushed to death - and on Wednesday, the Federal Reserve decides whether to make it worse.

Bitcoin trades near $74,000 on Monday, March 16, 2026. Strategy holds 761,068 BTC. Metaplanet holds 35,102 BTC. Short liquidations: $344M in 24 hours. Source: BitcoinMagazine Pro, Strategy SEC filing.

The $1.57 Billion Buy: Saylor Keeps Pulling the Trigger

Between March 9 and March 13, Strategy purchased 22,337 more bitcoin for approximately $1.57 billion at an average price of $70,194 per coin. The disclosure landed in an SEC filing Sunday evening. The purchase raised the firm's total holdings to 761,068 BTC - that is more than three percent of Bitcoin's entire fixed supply of 21 million coins concentrated in one company's treasury.

The math is staggering. Strategy has now spent $57.61 billion accumulating bitcoin. At the current market price near $74,000, those holdings are worth roughly $50 billion. The firm is sitting on a paper loss of about $7.6 billion on its average cost basis of $75,696 per coin. Saylor does not appear to care.

Before the official SEC filing, Saylor posted a cryptic message on X referencing Strategy's internal bitcoin tracker, writing "Stretch the Orange Dots." It was his way of telegraphing the buy before the paperwork hit. This is now a ritual. Markets know the pattern. The orange dots stretch, the filing follows, MSTR pops pre-market.

MSTR traded up 4.4% in pre-market trading Monday, according to Bitcoin Magazine. The stock has become a leveraged proxy for bitcoin exposure - its capital structure includes at-the-market programs across four preferred stock classes (STRK, STRC, STRF, STRD) totaling more than $31 billion in combined authorized raise capacity. The "42/42" initiative targets $84 billion in total capital raised through equity and convertible notes by 2027 - all earmarked for more bitcoin.

The previous week, the company had already bought 17,994 BTC for $1.28 billion. That means Strategy put $2.85 billion into bitcoin in ten trading days. At that pace the firm is running a sustained $12+ billion annual accumulation rate.

"IBIT ranked among the largest ETF inflows globally during the recent price decline. ETF investors showed a long-term accumulation pattern even during large price declines in Bitcoin." - Robert Mitchnick, Head of Digital Assets, BlackRock, speaking on CNBC, March 12, 2026

Metaplanet's $255 Million Raise: Japan Enters the Treasury Arms Race

While Saylor was filing his SEC disclosure, Tokyo-listed Metaplanet was closing a $255 million capital raise from global institutional investors - with another $276 million on the table via fixed-strike warrants if exercised before March 2028. Total potential raise: $531 million. All of it pointed at Bitcoin.

The company placed new shares at 380 yen ($2.39) each, a small premium to market. The fixed-strike warrants are exercisable at 410 yen ($2.57) per share, carrying a 10% premium to the placement price, according to CEO Simon Gerovich's post on X.

Metaplanet currently holds 35,102 BTC, valued at roughly $2.6 billion at current prices. That makes it a distant third behind Strategy and MARA Holdings among corporate holders - but the ambition is not distant at all. The company has publicly stated a target of 100,000 BTC by end of 2026 and 210,000 BTC by end of 2027. If Saylor is buying the mountain, Metaplanet is trying to buy the mountain range.

The capital structure is clever and worth dissecting. About $132 million of the raise will be used to repay the company's existing credit facility - a $500 million Bitcoin-backed loan with $280 million drawn as of March 11. Another $39.5 million goes toward margin collateral for options underwriting within the firm's bitcoin income generation business. The remainder funds fresh BTC purchases.

Metaplanet also announced two new subsidiaries this week: Metaplanet Ventures (deploying $25 million over the coming years into bitcoin financial infrastructure startups in Japan - lending, payments, custody, derivatives, compliance) and Metaplanet Asset Management. The company also disclosed a planned investment in Japanese stablecoin issuer JPYC Inc.

Shares of Metaplanet rose nearly 5% Monday as bitcoin climbed above $73,000, per Bitcoin Magazine reporting. The Japanese market is watching. This is not just one company's bet - it is a test case for whether a publicly listed Asian corporation can successfully replicate and accelerate the Saylor playbook in non-US jurisdictions.

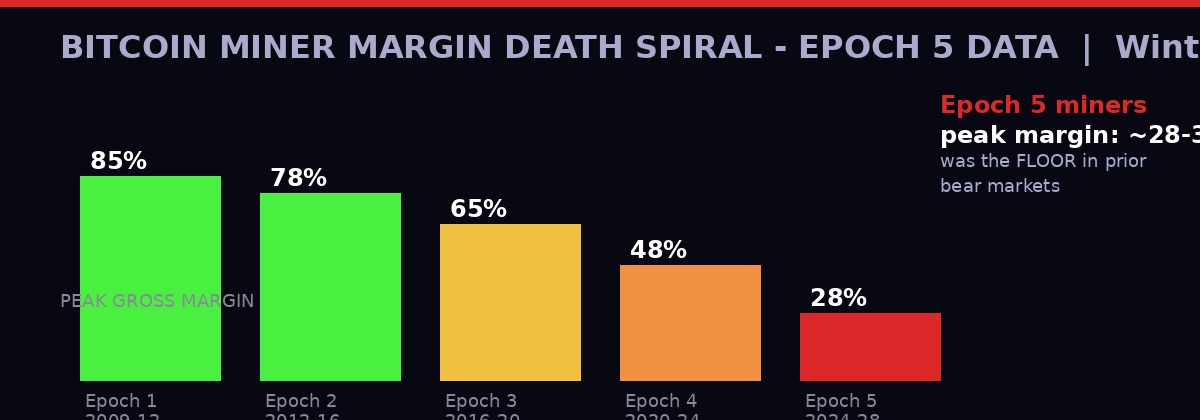

Peak gross margins by mining epoch, Epoch 1-5. Epoch 5 (2024-present) peak margin of ~28-30% was the floor in prior bear markets, not the ceiling. Data: Wintermute Research, "Epoch 5: A Structurally Different BTC Mining Cycle."

Miners Are Dying: Wintermute Delivers the Autopsy

There is a painful irony buried in the corporate treasury gold rush. Every bitcoin that Strategy and Metaplanet buy was produced by a miner. And those miners are, according to Wintermute's blunt new research report, in the worst structural position in the network's history.

Wintermute analyst Jasper De Maere's report, titled "Epoch 5: A Structurally Different BTC Mining Cycle," does not mince words. The thesis: miners who expect a bull market to bail them out the way it did in 2018 and 2022 are making a fatal miscalculation. This cycle is different, and the difference is permanent.

The core problem is the halving arithmetic. Bitcoin's block reward cuts in half every four years. In Epoch 5 (which began with the April 2024 halving), revenue per unit of compute dropped in half. In past cycles, explosive price appreciation - 10x to 20x over four years - covered up that revenue decline with room to spare. Peak gross margins in Epoch 2 and 3 sat at 78-85%. Epoch 4 peaked around 48%. Epoch 5 peak gross margins: roughly 28-30%.

The brutal twist is that those 28-30% margins were the floor during prior bear markets, not the ceiling during good times. Miners are now operating at stress-level economics during what should be a normal market environment.

Why? Because bitcoin now trades like a mainstream macro asset. With spot ETFs, institutional allocators, and corporate treasuries absorbing supply, the days of explosive retail-driven 20x runs are structurally less likely. The ETF machine that drives prices up is the same machine that compressed the ceiling for miners. The institutions took the volatility alpha that miners depended on for survival.

The transaction fee problem: Miners hoped fees would compensate for declining block rewards. They have not. Wintermute's analysis shows fee spikes tied to hype cycles and mempool congestion appear on charts but fade fast and rarely contribute more than a few percent of total miner revenue over time. Even accounting for fees, the margin lines between epochs barely diverge. The "second revenue stream" built into Bitcoin's protocol is not acting as a reliable backstop for Epoch 5 operations.

The report identifies two survival paths for miners who cannot simply wait for the next bull run. First: the AI pivot. High-performance computing and AI workloads need power and data center capacity fast. Big tech firms are racing to lock in sites. Miners who already control cheap power and built-out facilities are natural shortcut candidates. Sites once valued at $1-7 per watt as pure mining operations have traded hands at close to $18 per watt after AI repositioning, per Wintermute's data. HUT Mining's deal involving Google and Anthropic is the marquee example.

The catch, as Wintermute spells out clearly, is that not every miner has the location quality, balance sheet, or operational capacity to pivot. The AI pivot is an opportunity for a few large, well-capitalized operators. For the rest - the ones running older hardware in second-tier locations on thin credit - it is not a realistic lifeline.

Second survival path: active treasury management. Miners collectively hold close to 1% of all Bitcoin. Many have historically followed the "HODL" playbook, sitting on coins as a long-term bet. But Wintermute argues miners should be treating their BTC holdings like institutional investors - using derivatives, lending, and yield strategies to generate returns on the treasury rather than letting it sit. The irony is that this strategy essentially means miners competing with Strategy and Metaplanet in the treasury yield game - using the same financial products that are reshaping how bitcoin is owned.

The Corporate Treasury Record: 2.8x Mining Supply Absorbed

The macro picture behind the treasury arms race is striking. According to the latest corporate adoption report from BitcoinTreasuries.net, institutional demand has become a central structural pillar of the bitcoin market. Public companies, private firms, ETFs, and government-linked entities collectively hold a growing share of the circulating supply, with a small number of large buyers responsible for most of the recent accumulation.

The headline number: corporate bitcoin holdings reached a record in early 2026, with institutions buying at 2.8 times the new mining supply. Let that land. Buyers are absorbing 2.8 coins for every 1 coin the miners produce. At that absorption rate, exchange inventory drains regardless of price.

Strategy alone accounted for roughly 65% of all bitcoin added by corporate treasuries in February, per the BitcoinTreasuries.net report. Despite that buying dominance, February produced an unusual milestone - corporate treasuries collectively added about 7,800 BTC but disposed of approximately 8,600 BTC, producing a net decline of roughly 800 BTC for the first time since standardized tracking began. Likely explanation: smaller public miners selling coins to cover mounting operational losses and debt service - exactly the stress scenario Wintermute's analysis flagged.

The Q1 2026 picture looks different. Corporate treasuries have added roughly 62,000 BTC since January, with the pace accelerating sharply in early March as geopolitical tensions drove risk-asset volatility and Bitcoin outperformed traditional safe-havens. U.S. spot Bitcoin ETFs recorded approximately $586 million in inflows during the week of March 9-13 alone - one of the largest inflow weeks of the year - with BlackRock's IBIT continuing to attract capital despite price declines from peak levels.

The structural shift in bitcoin ownership is now multi-layered. ETFs provide exposure through regulated, exchange-listed products for institutional allocators who cannot hold crypto directly. Corporate treasuries like Strategy hold coins directly and use them as collateral for increasingly complex capital structures. Miners hold coins as a byproduct of production but are being forced to either sell or financialize them. And the fixed 21 million supply cap sits underneath all of it, making every absorbed coin a permanent structural tightening.

The Fed Wildcard: FOMC Starts Tuesday, Rate Decision Wednesday

All of the above is happening 24 hours before the Federal Reserve's most-watched policy meeting since the Iran-Israel war began. The Federal Open Market Committee convenes Tuesday with the rate decision and Chair Jerome Powell's press conference scheduled for Wednesday afternoon.

Markets are pricing rates unchanged. The CME FedWatch tool shows near-consensus expectations for a hold at current levels. But what matters is not the decision itself - it is the language, the dot plots, and Powell's answers to questions about oil, inflation, and when cuts might actually arrive.

Here is the tension. Bitcoin just broke back above $74,000 in part because geopolitical de-escalation signals eased energy markets - crude oil retreated from above $100 per barrel after US-Iran diplomatic contacts and two commercial tankers transited the Strait of Hormuz for the first time since fighting began. That retreat in oil prices reduced near-term inflation concerns. Equity futures turned positive. Risk sentiment improved.

But oil at $85-90 is still structurally inflationary compared to early 2025 levels. The Fed's dual mandate - maximum employment and price stability - is under pressure from both directions. Cutting too early risks reigniting inflation as energy costs stay elevated. Keeping rates high risks choking a slowing economy that is already feeling the weight of tariff uncertainty and Middle East supply disruption.

For crypto markets specifically, the Fed calculus has a direct transmission mechanism. Higher-for-longer rates increase the opportunity cost of holding zero-yield assets like bitcoin. Tighter financial conditions reduce the pool of speculative capital available for risk assets. Conversely, any dovish signal from Powell - even a softening of language around future cut timing - historically sparks immediate rallies in both crypto and equities.

"Despite being down from its October peak, Bitcoin has outperformed some traditional assets during the conflict - though volatility could increase depending on short-term selling and Fed signals." - Bitcoin Magazine, March 16, 2026

The short liquidation data reinforces how sensitive positioning has become. In the 24 hours ending Monday, roughly $344 million in derivative positions were wiped out, with bearish traders accounting for more than 80% of the total, per Bitcoin Magazine Pro data. That is a massive short squeeze clearing the deck heading into a macro catalyst. The market is leaning long going into FOMC. If Powell turns hawkish, the unwind could be violent.

The Bitcoin Tax Exemption War: Congress Fractures on De Minimis Relief

While the price action and treasury moves dominate headlines, a quieter but consequential fight is playing out on Capitol Hill that could reshape everyday Bitcoin utility in America - and the lobbying lines are drawn in unexpected places.

The issue: de minimis tax relief. Under current U.S. law, bitcoin is treated as property. Every single transaction with bitcoin - buying a coffee, sending a small remittance, paying a contractor - triggers a capital gains calculation. The IRS requires you to track cost basis and report gains or losses no matter how trivial the amount. This is a compliance nightmare that effectively makes bitcoin unusable as a payment medium for ordinary commerce.

Two competing approaches are circulating in the 119th Congress. Senator Cynthia Lummis introduced a standalone bill with a $300-per-transaction threshold and a $5,000 annual cap. House members Max Miller and Steven Horsford floated a discussion draft through the PARITY Act that would apply a narrower exemption only to regulated payment stablecoins, with a $200 threshold mirroring foreign currency rules.

The Bitcoin Policy Institute (BPI) is alarmed by the stablecoin-only framing. In a March 12 letter to key tax writers, BPI argued that limiting relief to stablecoins would leave bitcoin payments subject to full reporting obligations while creating a structural regulatory preference for stablecoin-mediated commerce. The group also notes that stablecoin transactions themselves rely on separate network tokens for gas fees - which remain taxable events under the stablecoin-only model, creating a compliance trap within the relief mechanism.

BPI's coalition has met with 19 congressional offices across both chambers over the past three months. The group is pressing for a value-based exemption covering both GENIUS-compliant stablecoins and large-cap network tokens, targeting up to $600 per transaction with an annual cap near $20,000.

The political window is narrow. Senator Lummis leaves the Senate in January 2027. The 2026 midterms will reshape committee compositions. And Coinbase has its own complications in this fight - CEO Brian Armstrong and Chief Policy Officer Faryar Shirzad both denied allegations that the exchange had lobbied against Bitcoin de minimis relief, with Shirzad calling the accusation "a total lie" after Bitcoin podcaster Marty Bent's March 11 report surfaced the claim. The denial was emphatic. The damage to Coinbase's Bitcoin-friendly credibility was still real enough to require a public response from the CEO.

The Structural Picture: What a 3.4% Concentration Means Long-Term

Step back from the week's data points and what emerges is a structural transformation in how Bitcoin functions as a financial asset. One company now controls 3.4% of the entire Bitcoin supply that will ever exist. A Japanese public company is racing to add another 1% by 2027. ETFs have collectively absorbed hundreds of thousands more coins into long-duration institutional custody. The coins being produced every day are being absorbed at 2.8 times the rate of production.

This creates a supply architecture that is fundamentally different from any prior Bitcoin market. In the 2017 bull run, retail buyers drove the price. In 2021, the initial institutional wave arrived but the supply dynamics were still fluid. In 2026, there is a class of buyers who are structurally committed to accumulating regardless of short-term price levels - and they have access to equity markets, debt markets, and derivatives structures to fund those purchases through any price environment.

Strategy's capital structure is the most sophisticated example. The 42/42 initiative - $84 billion in planned raises over three years through equity sales and convertible notes - means Saylor can buy bitcoin on dips, through wars, through Fed tightening cycles, through whatever the macro environment throws at the market. The preferred stock classes (STRK at 8% non-cumulative, STRF at 10% cumulative, STRC variable monthly, STRD at 10% non-cumulative) give different investor profiles exposure to bitcoin's upside while receiving fixed income returns. It is a machine designed to continuously convert traditional capital into bitcoin, regardless of conditions.

For miners, the implications are existential in a different direction. They produce coins at enormous cost - energy, hardware, capital expenditure - and face a structural squeeze on margins that Wintermute's analysis suggests will not recover to historical norms without a sustained 10x-20x price appreciation. The AI pivot offers a lifeline for the well-capitalized few. For the rest, consolidation, bankruptcy, or transformation into treasury management vehicles are the realistic outcomes.

Bitcoin at $74,000 on Monday was not just a price print. It was the result of a $344 million short squeeze, two massive institutional buy disclosures, a geopolitical de-escalation that pulled oil down from triple-digit territory, and a market positioning itself for a Federal Reserve that could either accelerate the rally with dovish language or kill it with hawkish restraint. Every one of those variables converges Wednesday at 2 PM Eastern when Powell takes the podium.

Strategy purchases 22,337 BTC for $1.57 billion at average $70,194/coin. SEC filing March 16.

BlackRock's Robert Mitchnick says on CNBC that ETF investors showed accumulation behavior through price weakness. IBIT among largest ETF inflows globally during conflict period.

Wintermute publishes "Epoch 5: A Structurally Different BTC Mining Cycle." Key finding: miner peak gross margins 28-30% - the floor in prior bear markets, not the ceiling.

Bitcoin Policy Institute leads coalition letter to Congress. Demands de minimis tax relief cover bitcoin, not just stablecoins. Has met with 19 congressional offices.

Strait of Hormuz: two commercial tankers transit for first time since Iran-Israel conflict. Iran signals restrictions apply only to adversary-linked vessels. Bitcoin recovers to $74,000.

Metaplanet closes $255M capital raise. Warrants could add $276M more. Target: 210,000 BTC by 2027. Strategy SEC filing published. Bitcoin at $74,000. $344M shorts liquidated in 24h.

Federal Open Market Committee convenes. Two-day meeting begins.

FOMC rate decision 2 PM ET. Jerome Powell press conference. Markets watching for language on cut timing, inflation trajectory, energy impact.

What Happens Next: Three Scenarios for Wednesday

Scenario 1 - Hold with dovish language (base case, ~60% probability): Powell confirms hold, acknowledges progress on inflation, signals that two or three cuts remain likely in 2026. Risk assets rally. Bitcoin tests $78,000-$80,000 within the week. Short interest that rebuilt after Monday's squeeze gets punished again. Metaplanet shares pop another 5-8%. MSTR follows. Corporate treasury model gets another validation print.

Scenario 2 - Hold with hawkish pivot (~30% probability): Powell emphasizes oil-driven inflation risks, removes language about rate cuts in 2026, or raises the prospect of a hike if energy prices sustain. Risk assets sell off. Bitcoin gives back $3,000-$5,000 of recent gains. The $344 million short squeeze gets partially rebuilt. Miner stocks - already near multi-year lows - take another leg down. This is the scenario that most resembles 2022 regime dynamics.

Scenario 3 - Surprise cut (~10% probability): The market has not priced this and it would be extraordinary given oil at $85-90. A cut would likely trigger the fastest bitcoin rally of 2026, potentially a run at all-time highs above $100,000 before month-end. This is not the base case but the positioning going into Wednesday is lopsided enough that any dovish surprise compounds dramatically.

The institutional buyers are not waiting for the Fed. Strategy has been deploying capital through every macro scenario that 2026 has produced - war, tariffs, oil shocks, and yield volatility. Metaplanet closed its raise regardless of FOMC timing. The corporate treasury machine is running on its own fuel: equity issuance, preferred stock sales, and convertible debt converting traditional capital into bitcoin at whatever the spot price happens to be.

The miners are not so fortunate. They depend on the spot price to cover operating costs that are paid in dollars. Every week of sub-$75,000 bitcoin is another week of compressed margins in a market where peak margins are already where floors used to be. Wintermute's prescription - AI pivot or active treasury management - assumes capital and optionality that most miners simply do not have.

Three groups. Three completely different relationships with the same asset. Strategy and Metaplanet treat bitcoin as the destination - the thing you accumulate regardless of cost. Miners treat it as the output of an industrial process - the thing you sell to cover costs or HODL as a bet on future price appreciation. The Fed treats it as a data point in a broader risk-asset landscape where crypto amplifies whatever direction the macro sends it.

Wednesday at 2 PM ET, all three groups find out which direction Powell sends it.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram