Senate Breaks Stablecoin Yield Deadlock - But the Clarity Act Still Has Miles to Go

Senators Tillis and Alsobrooks reached an "agreement in principle" Friday on the most contentious clause in the Digital Asset Market Clarity Act. Meanwhile, bond markets are crumbling, rate hike bets hit 12%, and a DeFi exploit just handed attackers $5.8 million.

Photo: Pexels - Capitol Hill financial legislation

Friday evening in Washington, two senators shook hands on a deal months in the making. Senator Thom Tillis (R-NC) and Senator Angela Alsobrooks (D-MD) reached what their offices are calling an "agreement in principle" on the stablecoin yield provision inside the Digital Asset Market Clarity Act - the crypto industry's single most important piece of pending legislation. [CoinDesk, March 20, 2026]

The compromise unclogs one of the biggest bottlenecks on a bill that has been in legislative purgatory since 2023. Whether it actually gets the Clarity Act to a Senate floor vote before the summer is a different question entirely.

The deal came on the same day that oil was trading at $96 per barrel after a 50% surge since the Iran conflict began, bond markets were pricing the first U.S. rate hike odds at 12% for April - up from literally zero one week ago - and a Venus Protocol exploit from March 16 was still bleeding out $2.15 million in bad debt onto BNB Chain. It was a Friday that had everything.

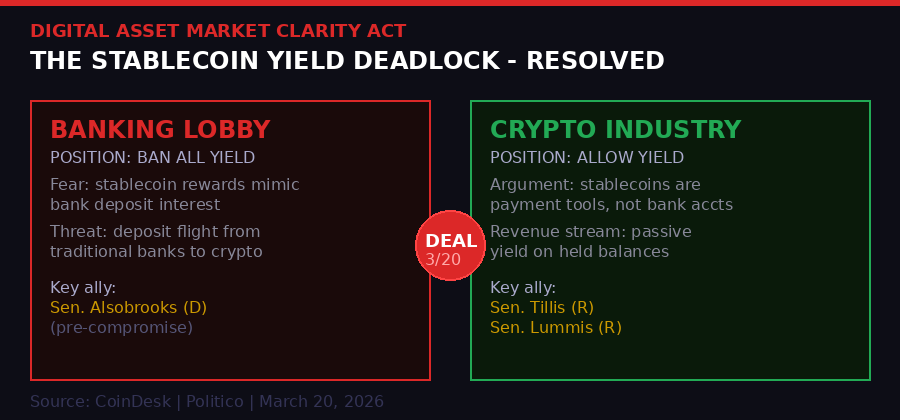

The two-sided battle over stablecoin yield: banking lobby vs. crypto industry, with Tillis-Alsobrooks brokering a middle path.

1. The Stablecoin Yield Battle, Explained

Photo: Pexels

The stablecoin yield debate sounds technical. The money at stake is anything but. Stablecoins are dollar-pegged tokens - USDT, USDC, the incoming wave of bank-issued stablecoins. The question that nearly killed the Clarity Act: should stablecoin issuers be allowed to pay holders a yield on their passive balances?

The banking lobby said no. Hard no. Their argument: if you can hold USDC and earn 4%, 5%, maybe 6% passively, why would anyone keep money in a checking account earning 0.01%? Deposit flight. That is the fear. Deposits underpin the entire fractional reserve lending system. Remove the deposits, you remove the lending capacity, and you potentially destabilize the financial system that underpins everything else. [CoinDesk, March 20, 2026]

Senator Alsobrooks came in representing those concerns. She sits on the Senate Banking Committee alongside Senator Tillis - the crypto-friendly Republican who has been one of the Clarity Act's most vocal champions. Their disagreement over the yield clause was the single most publicized sticking point in months of negotiations.

"Sen. Tillis and I do have an agreement in principle. We've come a long way. And I think what it will do is to allow us to protect innovation, but also gives us the opportunity to prevent widespread deposit flight." - Senator Angela Alsobrooks, March 20, 2026 [via Politico]

The details of the compromise remain under wraps. Connor Lounsbury, Alsobrooks' communications director, told CoinDesk the legislators planned to "consult industry stakeholders to solicit feedback" before circulating text. Translation: the crypto and banking industries won't see the actual language before Monday at the earliest. [CoinDesk, March 20, 2026]

What is known: the compromise will bar rewards on passive stablecoin balances. Active use cases - paying for things, on-chain DeFi activity - appear to remain in play. The exact demarcation between "passive" and "active" is where the lawyers will earn their fees.

- Legislation in question: Digital Asset Market Clarity Act (formerly DAMS/FIT21 successor)

- Committee path: Senate Banking Committee hearing expected late April 2026

- Parallel track: Senate Agriculture Committee passed its own version - bills must be merged

- Outstanding issues beyond yield: DeFi treatment, illicit finance provisions, ethics clauses

- Target floor vote: May 2026 (under threat from Iran war vote competition for floor time)

- White House involvement: Officials reviewed updated legislative text Thursday, March 19

2. The Clarity Act's Long Road From FIT21 to Now

Three years from concept to near-passage: the Clarity Act's legislative journey through multiple Congresses.

The bill's origins trace back to 2023, when the House passed the FIT21 - Financial Innovation and Technology for the 21st Century Act - with surprising bipartisan support. The Senate did nothing with it. Crypto's moment in the spotlight at that stage was colored by FTX's implosion and a succession of fraud convictions. The timing was bad. [Congressional Record, 2023-2024]

The political environment flipped in 2025. Trump's return to the White House brought a crypto-friendly executive branch for the first time. The SEC retreated from its enforcement-first posture. The CFTC and SEC began joint rulemaking instead of legal warfare. And Congress, emboldened, tried again with a more comprehensive bill: the Digital Asset Market Clarity Act.

The new bill went further than FIT21. It attempted to draw clear jurisdictional lines between SEC-regulated securities tokens and CFTC-regulated commodity tokens, a distinction that had been litigated expensively for years. It addressed DeFi protocols with a treatment that made some Democrats nervous about money laundering. And it tackled stablecoins - which had been previously addressed in separate legislation like the GENIUS Act, but which the Clarity Act sought to integrate into a unified framework. [CoinDesk, multiple 2026 reports]

The yield provision snagged everything. Through 2025 and into early 2026, the Banking Committee deadlocked repeatedly. Tillis and Alsobrooks were assigned to find a way through. That process took months. Friday's announcement suggests they found one - though "agreement in principle" is Washington-speak for "we agree on the concept, but don't ask us about the specifics yet."

"This is an important step forward for market structure legislation, a step that both have worked for months to resolve. Of course, there are still outstanding issues in the wider legislation - including ethics and illicit finance - that still need resolution to secure a broad, bipartisan vote in the Banking Committee." - Connor Lounsbury, Sen. Alsobrooks' communications director [CoinDesk, March 20, 2026]

Senator Cynthia Lummis, who chairs the Banking Committee's crypto subcommittee and has been the Senate's most relentless crypto advocate, predicted a hearing in the latter half of April. She posted on X on Friday - a photo of a "yield" sign. Her sense of humor about the situation suggests genuine confidence. [CoinDesk, March 20, 2026]

The compressed timeline creates political risk. Senate floor time is scarce. Republicans are pushing a voter-ID bill. The Iran war authorization debate is consuming oxygen. May is achievable if nothing goes sideways. But in 2026, nothing staying sideways is not a safe assumption.

3. Morgan Stanley's MSBT Filing: Wall Street's Next Move on Bitcoin

Photo: Pexels

While senators negotiated in Washington, Morgan Stanley was quietly updating its SEC filings. The bank confirmed its planned spot bitcoin ETF will trade under the ticker MSBT - and seeded it with an initial $1 million, plus two shares purchased earlier this month for audit purposes. [SEC EDGAR Filing, March 20, 2026]

The structural details matter. BNY Mellon handles cash and administrative functions. Coinbase serves as prime broker and custodian for the actual bitcoin holdings. The 10,000-share creation unit requirement is standard for institutional ETF products. It is a professionally structured product, not a startup experiment.

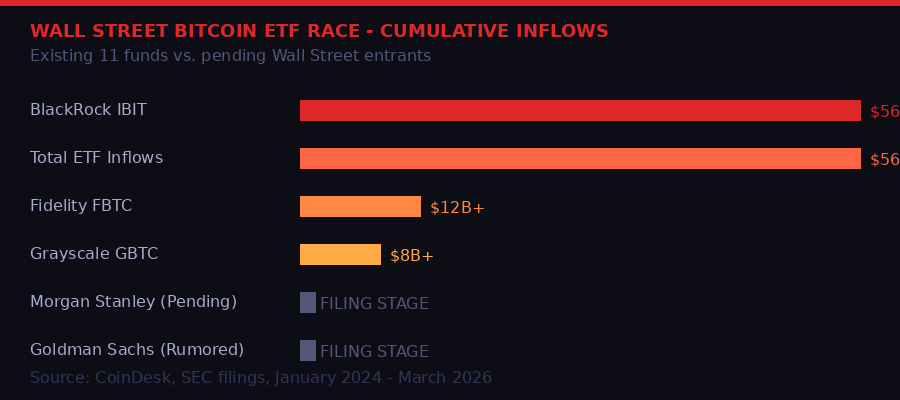

Morgan Stanley is not entering an empty market. Eleven spot bitcoin ETFs have been active since January 2024. BlackRock's IBIT alone has accumulated over $56 billion in combined inflows across all spot BTC ETFs. The MSBT would be the twelfth fund chasing the same institutional capital pool - differentiated mainly by the Morgan Stanley brand and the bank's massive wealth management distribution network. [CoinDesk, March 20, 2026]

Wall Street's bitcoin ETF land grab: $56B+ in combined inflows since January 2024, with Morgan Stanley joining the queue.

That distribution advantage is the entire thesis for MSBT. Morgan Stanley manages over $5 trillion in client assets through its wealth management division. Financial advisors at the bank can now offer clients direct BTC exposure through a familiar brokerage wrapper. The ETF does not need to attract crypto-native investors - it needs to offer a frictionless on-ramp for the 60-year-old retirement account holder who has been hearing about bitcoin for five years and finally wants in.

The bank also filed for a Solana ETF earlier this year. That application has seen no material updates - suggesting the focus is on getting MSBT approved and operational before expanding to alt-coins. One battle at a time.

4. Rate Hike Fear Returns: Bonds Break, Inflation Bites

Photo: Pexels

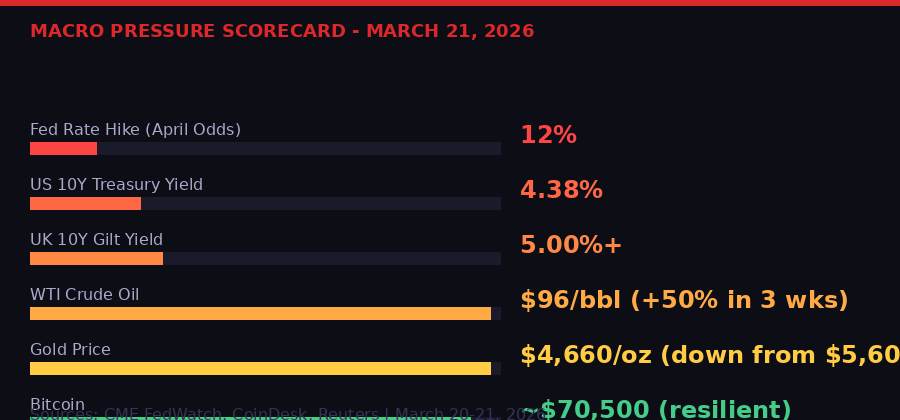

The most alarming macro development this week was not a crypto story. It was the 12% probability of a Federal Reserve rate hike priced into April futures by Friday - up from zero percent one week ago. [CME FedWatch, March 20, 2026]

Rewind three months. The dominant market narrative in January 2026 was about rate cuts. How many? When? Two cuts? Three? The Fed's "higher for longer" posture seemed to be softening. The economy was showing early signs of slowing. Inflation was still above target at 2.4% headline and 2.5% core in February data - but the direction felt manageable.

Then Iran. Oil was at $64 per barrel before the conflict erupted. By mid-March it was approaching $108. By Friday, after brief relief on news of possible sanctioned Iranian oil releases, it had pulled back to $96. That is still a 50% surge in three weeks. [Reuters, CNBC, March 2026]

A 50% oil shock does not stay contained. It seeps into every input cost, every transportation price, every inflation metric that the Fed watches. The February PCE data - already at 2.4% before the war began - is now stale. March data will be ugly. The Fed, which had been patient, now faces a stagflation scenario: slowing economic growth colliding with supply-side inflation it has no real tools to address.

March 21, 2026 macro snapshot: rate hike bets rising, bonds selling globally, gold retreating from record highs - BTC the lone performer.

The bond market is pricing this in brutally. The 10-year U.S. Treasury yield jumped another 10 basis points on Friday to 4.38% - up from under 4% at the start of March. That is a 38 basis point move in three weeks, which for the treasury market is dramatic. [CoinDesk, March 20, 2026]

The bond selloff is not isolated to the United States. In the U.K., 10-year gilt yields have pushed above 5% for the first time since 2008. UK gilts at 5% reference a specific kind of financial memory - the last time that happened, the global financial crisis was underway and central banks were about to undertake emergency interventions. The current spike is different in mechanism but the number carries psychological weight. [CoinDesk, March 20, 2026]

For crypto, the implications are complex. Higher rates are traditionally bearish for risk assets - they increase the opportunity cost of holding non-yielding assets like bitcoin, reduce risk appetite, and tighten liquidity conditions. But BTC at $70,500 has demonstrated unusual resilience since the war began. The S&P 500 is down more than 5% from late February. Gold, after a spectacular run to $5,500 per ounce at the start of March, has cratered to $4,569 - a 17% collapse in three weeks. Silver has fallen from $95 to $69.50. [CoinDesk, March 20, 2026]

"Bitcoin has once again acted as the canary in the macro coal mine. At current levels, bitcoin is already pricing a recession, while many traditional assets are not." - Andre Dragosch, European Head of Research at Bitwise [CoinDesk, March 20, 2026]

If Dragosch is right, the implication is that BTC bottomed before equities - and that the S&P 500, Nasdaq, and credit markets have more pain ahead before they catch down to where bitcoin is already trading. That is a bold call in either direction.

5. The Venus Protocol Exploit: Nine Months of Patience, One Day of Theft

Photo: Pexels

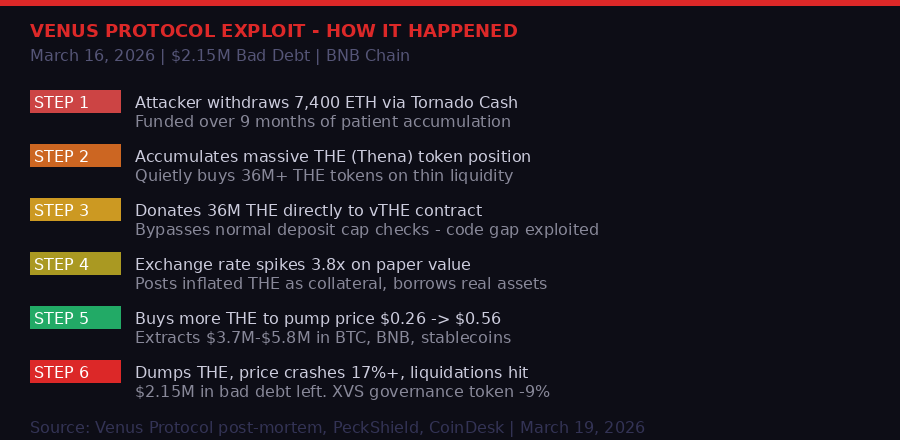

DeFi exploits have a rhythm to them. A vulnerability sits undetected. A sophisticated attacker identifies it. They spend weeks or months positioning. Then in a single session they execute, extract value, and vanish. The Venus Protocol attack on March 16 followed that pattern with unusual precision. [Venus Protocol post-mortem, March 19, 2026]

Venus is one of BNB Chain's largest lending protocols - a money market with over $1.4 billion in total value locked. The exploit targeted its Thena market, which allows borrowing and lending against the THE token issued by the Thena DEX. The attacker's trail, reconstructed by blockchain security firm PeckShield, began nine months before the attack itself. [PeckShield, March 19, 2026]

How the Venus exploit worked: nine months of preparation, one day of execution. $2.15M in bad debt, up to $5.8M extracted.

The attacker withdrew 7,400 ETH from Tornado Cash - the cryptocurrency mixer that the U.S. Treasury previously sanctioned before partially reversing course in early 2026. They used that capital to accumulate a massive position in THE tokens over nine months, moving carefully enough to avoid triggering community alarm. [PeckShield, CoinDesk, March 19, 2026]

Then on March 16, they executed the critical step: donating 36 million THE tokens directly to the vTHE contract - Venus's vault wrapper for the token. This is where the code gap lived. Normal deposits run through cap checks that prevent any single position from distorting the market. The direct donation bypassed those checks entirely. The exchange rate on the vTHE contract jumped 3.8 times on paper.

With artificially inflated collateral, the attacker borrowed real assets - tokenized bitcoin, BNB, stablecoins. They used some of that borrowed capital to buy more THE on the open market, pushing the token price from $0.26 to $0.56. Then they dumped. THE fell 17% in under 24 hours. Liquidations cascaded. The protocol was left with $2.15 million in bad debt - loans the system can no longer recover. [Venus Protocol, March 19, 2026]

The XVS governance token dropped 9% on the news - delayed by days because the price impact wasn't clear until analysis showed Justin Sun-linked wallets and other large holders moving XVS to exchanges in anticipation. [CoinDesk, March 19, 2026]

Venus's public response included an admission that stings: the attacking address had been flagged by community members before the incident occurred. The protocol did not act. Their reasoning:

"Venus is a decentralized protocol. As a permissionless protocol, we cannot and should not freeze or blacklist addresses based on suspicion alone. This is a tension inherent to DeFi, and one we take seriously." - Venus Protocol official statement [March 19, 2026]

That statement captures the unsolvable tension in DeFi risk management. If protocols can freeze addresses on suspicion, they are not really decentralized - they are managed systems with admin keys. If they cannot, they leave the door open for patient attackers who do nothing technically illegal in the accumulation phase. The $2.15 million in bad debt will be covered by Venus's risk fund, pending a governance vote. The code gap is being patched. The philosophical gap remains open.

6. Coinbase Becomes the Everything Exchange: Stock Perps Go Live

Photo: Pexels

One company spent Friday expanding its market while everything else was burning. Coinbase launched stock perpetual futures contracts for non-U.S. traders - a product category that puts the exchange in direct competition with traditional brokerages for 24/7 equity exposure. [Coinbase blog, March 20, 2026]

The contracts cover what the industry calls the "Magnificent 7" - Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla. Traders can also access perpetual futures on SPY and QQQ, the dominant S&P 500 and Nasdaq 100 ETFs. Leverage goes up to 10x on individual stocks, 20x on ETF products. All contracts are cash-settled in USDC. They never expire. [Coinbase, March 20, 2026]

The competitive framing here is significant. Traditional stock perpetuals have been available on decentralized platforms - Hyperliquid in particular has become a hotbed for round-the-clock equity futures, including S&P 500 contracts it introduced this week. Coinbase's move is the centralized exchange answer to that DeFi trend. [CoinDesk, March 20, 2026]

The "Everything Exchange" strategy has a clear logic. Coinbase's core US spot and derivatives business faces constant regulatory pressure and competitive erosion from DeFi alternatives. If the exchange can expand into equities, forex, and commodities for non-US users - wrapping it all in USDC settlement and cross-margining with crypto positions - it becomes structurally different from both traditional brokerages and pure crypto exchanges. Something neither industry can simply copy.

- Coinbase stock perps: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, Tesla + SPY/QQQ ETFs

- Leverage: Up to 10x single stocks, 20x ETF products

- Settlement: Cash-settled in USDC (Circle's dollar stablecoin)

- Cross-margining: Integrated with existing Coinbase crypto derivatives risk engine

- Availability: Non-U.S. retail and institutional traders

- Competitor: Hyperliquid launched S&P 500 perps same week (decentralized)

This launch also matters for the stablecoin debate playing out in Washington. USDC - issued by Circle Internet, ticker CRCL - is the settlement currency for these contracts. If the Clarity Act passes with favorable treatment for dollar-pegged stablecoins, Circle and Coinbase (which jointly created USDC through the Centre consortium) stand to benefit enormously from the product's growth. The legislative and commercial threads are tangled in ways that lobbyists on both sides understand very well.

The timing - Friday of the same week the stablecoin yield deal was announced - underscores how aggressively Coinbase is moving. Brian Armstrong's "Everything Exchange" framing is not marketing language. It is the actual strategic roadmap, executed in real time, with quarterly product launches to back it up.

7. Gauntlet's $380 Million Vanishing Act - And Why It Does Not Mean What You Think

Photo: Pexels

The headline reads badly: DeFi risk management giant Gauntlet lost $380 million in TVL in a week. Seven-day drop of 22.84%, from $1.72 billion to $1.325 billion. Single-day slide of 7.57% on Thursday. [DeFiLlama, CoinDesk, March 19, 2026]

The reality is more mundane. OKX ran a pre-deposit campaign on Katana, a DeFi-focused blockchain. Pre-deposit campaigns work exactly like what the name suggests: protocols incentivize users to park capital ahead of a launch, often with promises of airdrops or token allocations. Capital floods in. Campaign ends. Capital floods out. TVL charts look like a spike followed by a cliff.

Gauntlet's TVL surged around March 2 when the OKX campaign went live. The campaign ended March 18-19. The $380 million exit was not panic - it was the scheduled unwinding of incentive-driven deposits. The underlying assets going out were predominantly stablecoins, not risk capital burning through a protocol collapse. [Gauntlet statement to CoinDesk, March 19, 2026]

"Institutional risk managers manage through these events. Working to maintain rates, preserve capital supplied to vaults, and adjusting to market conditions." - Gauntlet official statement [CoinDesk, March 19, 2026]

For context, Gauntlet handled a $775 million single-transaction deposit in October 2025 - a 40x TVL spike - and recovered to pre-deposit levels within ten days. They have seen this movie before. What makes Gauntlet's model resilient is that the firm does not hold user funds itself - it sets the risk parameters for lending markets and vaults. When TVL moves, Gauntlet adjusts parameters. The governance logic, not the capital stock, is the product. [Gauntlet blog, CoinDesk, March 2025]

The more interesting signal in the Gauntlet story is the yield competition. The firm's USDC vault currently offers 4.86% APY. Solana-based protocol Jito offers 5.69% on SOL staking. In a DeFi environment with working yields in the 4-8% range, capital will move constantly toward the highest risk-adjusted return. That rotation is healthy in a functioning market. It also means protocol TVL numbers are a less reliable signal than they used to be - capital is mercenary now, and it moves fast. [DeFiLlama, March 2026]

8. What Happens Next - The Paths Forward

Photo: Pexels

Six stories, one week, three distinct pressure fronts converging on crypto markets simultaneously. Here is where each thread goes next.

Clarity Act: April Hearing is the Test

The Tillis-Alsobrooks deal removes the yield provision as a blocker - in theory. The actual legislative text goes to industry stakeholders Monday. Banks will scrutinize every word for deposit flight risks. Crypto firms will scrutinize for over-restriction. Any ambiguity in the "passive vs. active" yield distinction will surface immediately in feedback.

If the Banking Committee schedules a hearing in late April, the bill is on track for a May Senate floor attempt. If the committee hearing slips to May, the floor vote pushes to June or later - at which point Iran war politics and budget negotiations could crowd it out entirely. Senator Lummis's confidence is real, but the legislative calendar is not sympathetic to optimism. [CoinDesk, Politico, March 2026]

Macro: The April Fed Meeting is Radioactive

At 12% probability, a rate hike in April is still unlikely. But it is no longer zero. If March CPI data lands above 3% - entirely plausible with oil at $96 and supply chain stress building - that 12% becomes 25%, then 35%. The Fed's credibility on inflation is deeply tied to its ability to respond when inflation re-accelerates. A second inflation wave during an oil shock is the nightmare scenario it has been trying to avoid since 2022. [CME FedWatch, CoinDesk, March 20, 2026]

Bitcoin's resilience near $70,000 is impressive but not guaranteed. If equities enter a real bear market - the S&P 500 down another 10-15% from here - institutional investors who added BTC exposure in 2025 may need to liquidate to cover margin calls and redemptions. Correlation to equities is lower than it used to be, but it is not zero.

DeFi Security: Venus Sets a Pattern

The Venus exploit post-mortem is required reading for every DeFi protocol still running oracle-dependent lending markets. The attack vector - patient accumulation, direct contract manipulation to bypass cap checks, inflated collateral extraction - was not novel. It was an old pattern executed with unusual patience and precision. Nine months of setup for a single execution day.

Protocols with flagged addresses that they chose not to act on face an uncomfortable governance question. The decentralization argument is philosophically coherent but operationally costly. At $2.15 million in bad debt, Venus absorbed the loss. At $50 million, governance would be in crisis. The Clarity Act's DeFi provisions - still unresolved - will have to grapple with exactly this kind of tension between permissionlessness and user protection. [Venus Protocol, CoinDesk, March 19, 2026]

Morgan Stanley and Coinbase: Institutional Moat-Building

MSBT and the Coinbase stock perps launch are two sides of the same institutional infrastructure trend. Morgan Stanley is building distribution for bitcoin through wealth management. Coinbase is building product for global retail through the "Everything Exchange" wrapper. Both are racing ahead of the regulatory clarity they technically do not yet have.

That bet - build the infrastructure now, get regulatory clarity later - has worked so far. The eleven existing bitcoin ETFs pulled in $56 billion before the Clarity Act passed. Coinbase's stock perps launched before any regulatory framework for crypto-settled equity derivatives existed. The speed advantage is real. The risk is that a Clarity Act that passes with restrictive DeFi or stablecoin provisions could retroactively constrain products already live. Both firms will have lobbyists at every stakeholder consultation between now and the April hearing. [CoinDesk, SEC EDGAR, March 2026]

The week ended with the legislative, macro, and technical risk layers all in motion simultaneously. The Clarity Act deal is a genuine development - one senators and industry have been working toward for years. The rate hike fear is a real threat that could derail risk assets if it accelerates. The Venus exploit is a reminder that DeFi's security model has known failure modes that the industry still has not resolved. Morgan Stanley filing MSBT and Coinbase launching stock perps are the forward edge of institutional crypto infrastructure that will define the next market cycle.

All of it is happening at the same time. That is not a coincidence. That is what a market inflection point looks like.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram