America Surrenders the Crypto War: SEC & CFTC Declare Most Digital Assets Are Not Securities

Forget gradual reform. In a single joint statement issued this morning, the U.S. SEC and CFTC officially confirmed what the crypto industry has been demanding for a decade: most digital assets are not securities. Today is the day the regulatory war ended - and the industry won.

The joint SEC-CFTC statement issued March 18, 2026 represents the most significant regulatory reversal in crypto history.

MARKET SNAPSHOT - MARCH 18, 2026

The Statement That Changed Everything

The new five-category token taxonomy introduced by the SEC/CFTC joint staff statement on March 18, 2026.

The U.S. Securities and Exchange Commission and Commodity Futures Trading Commission issued a joint staff statement on March 18, 2026 declaring that the vast majority of crypto assets do not qualify as securities under U.S. law. The document introduces a formal five-category taxonomy for digital assets - the first time U.S. regulators have published a codified classification framework for the industry.

SEC Chair Paul Atkins set the tone explicitly. The SEC is, in his words, no longer the "securities and everything commission." That one sentence is worth parsing carefully. For years, the SEC under Gary Gensler pursued a strategy of enforcement-by-ambiguity: if something was digital and moved in price, someone at the agency thought they could reach it. That strategy is now officially dead.

"Surreal." - Jake Chervinsky, crypto legal expert, reacting to the scope of the SEC/CFTC joint statement on X, March 18, 2026

The five categories established are: Digital Securities (narrowly defined investment contracts requiring full registration), Digital Commodities (Bitcoin, Ethereum, and similar assets not tied to managerial effort - CFTC jurisdiction), Stablecoins (payment rail assets, neither securities nor CFTC-regulated commodities), Digital Tools (utility and access tokens built for functional use within protocols), and Restricted Digital Assets (a transitional class covering pre-launch and vesting tokens with time-limited rules).

The critical shift: "investment contract" now requires proof that profits are tied to the ongoing managerial efforts of a specific identifiable third party. That test - effectively a modernized Howey test - excludes most decentralized networks by design. Bitcoin, Ethereum, and the bulk of established DeFi protocol tokens comfortably fall outside it.

Source: SEC/CFTC Joint Staff Statement, March 18, 2026; Unchained Crypto reporting, March 18, 2026

The Howey Test Gets Modernized

The original Howey test dates to a 1946 Supreme Court ruling involving Florida orange groves. The SEC applied it to crypto by arguing that token buyers were investing money in a common enterprise with an expectation of profit from others' efforts. That argument worked in cases like XRP (Ripple), where a company was actively promoting and developing the asset.

It never worked cleanly for Bitcoin or Ethereum. Federal courts repeatedly rejected the SEC's attempts to classify Ether as a security. The agency's own lawyers disagreed internally for years about whether BTC's proof-of-work mining structure counted as the kind of "managerial effort" the Howey test requires. The joint statement ends that ambiguity.

Going forward, regulators will focus on three questions when evaluating any digital asset: Does the issuer retain ongoing control over the network? Were tokens sold with explicit profit promises tied to that control? Is there a formal investment relationship between token holders and the issuing entity? If the answer to all three is no, the asset is not a security.

This framework legitimizes the vast majority of the top 100 tokens by market cap. It also creates a clear path for new projects: decentralize early, hard-code governance, and publish clear utility documentation - and you avoid the securities framework entirely.

The statement also directly addressed staking, mining, and airdrops - three areas where the prior SEC stance was either unclear or openly hostile. Staking rewards are not securities. Mining income is not a securities transaction. Airdrops to wallets meeting specific criteria do not constitute securities distributions. All three of these positions represent clean reversals from Gensler-era enforcement posture.

Source: SEC/CFTC Joint Staff Statement; Unchained Crypto; Jake Chervinsky commentary via X, March 18, 2026

Phantom Wins a Precedent-Setting CFTC Ruling

The same morning the joint taxonomy landed, the CFTC issued a no-action letter to Phantom - the most widely used self-custodial Solana wallet - confirming the regulator will not pursue enforcement action for Phantom connecting its users directly to regulated derivatives markets.

The mechanics of the ruling matter. Phantom is categorized as a "passive interface" rather than an intermediary. Users interact directly with fully registered exchanges and brokers. Phantom provides the front end to view and submit trades. It does not hold funds. It does not settle transactions. It does not custody assets. Under this logic, it is software - not a financial intermediary.

"Regulators are beginning to draw clearer lines around non-custodial software, especially tools that do not touch user funds." - Unchained Crypto, March 18, 2026

The no-action relief comes with guardrails. Phantom must maintain visible risk disclosures inside the interface. The company must build and maintain a compliance program tied specifically to derivatives activity. Record-keeping requirements apply to any derivatives-related data generated by users. And critically - the relief explicitly does not cover DeFi derivatives or prediction markets. That frontier remains unresolved.

Still, the signal is loud. Non-custodial wallets that function as interfaces rather than intermediaries can connect to traditional financial rails without becoming licensed brokers. This is the blueprint the entire wallet industry has been waiting for. Expect MetaMask, Rainbow, and Backpack to file similar no-action requests within months.

The broader implication reaches beyond wallets. If a piece of software that routes orders but never touches funds can avoid broker-dealer registration, the same logic applies to smart contracts, DEX front-ends, and protocol aggregators. The CFTC just told the industry: build non-custodial, build transparent, and you can plug into regulated markets without the full compliance overhead of a broker.

Source: CFTC No-Action Letter to Phantom, March 18, 2026; Unchained Crypto reporting

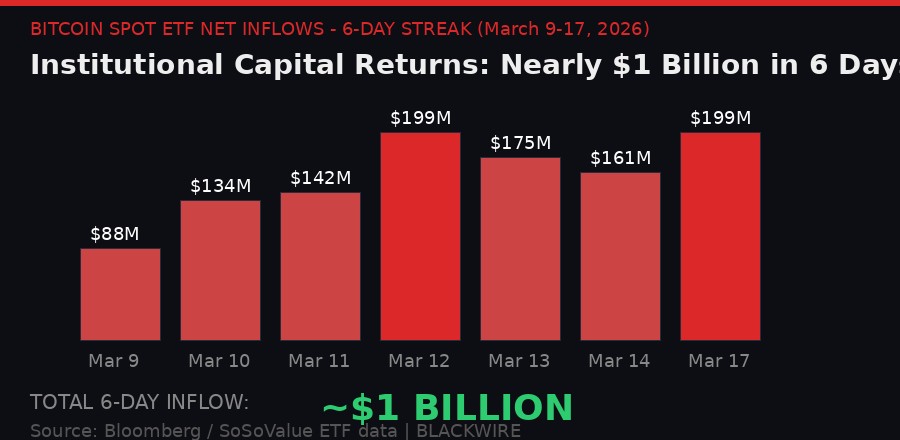

Bitcoin ETF Inflows Hit $1 Billion in Six Days - The Institutions Are Back

Bitcoin spot ETF net inflows from March 9-17, 2026. Six consecutive days of positive flow totaling nearly $1 billion, with BlackRock's IBIT and Fidelity FBTC leading.

The regulatory news lands on top of a market that was already finding its footing. Bitcoin has been on a quiet tear since March 9, climbing from the mid-$60,000s toward $75,000 as spot ETF inflows returned with force. Six consecutive days of positive flow, totaling nearly $1 billion in net inflows, tell you everything about where institutional sentiment sits right now.

March 12 was the standout session: $199 million in single-day inflows, the highest since the post-election surge in late 2024. BlackRock's IBIT and Fidelity's FBTC led the charge, collectively accounting for over 60% of the flows. These are not retail buyers. These are institutional allocators who pulled back during February's correction and are now rebuilding positions systematically.

The market structure around the move amplified it. Over $600 million in liquidations hit in the 24-hour period around March 17, the majority of it from short positions. When you have sustained ETF inflows driving spot demand while leveraged shorts are getting unwound simultaneously, price action gets violent and one-directional. The $75,000 print was a direct result.

BTC ETF INFLOW STREAK - MARCH 9-17, 2026

Analysts quoted by Unchained are cautioning the rally is "flow-driven" - meaning it depends on continued institutional demand rather than organic retail enthusiasm. That caution is mathematically correct but likely overstated in its near-term implication. The Fear and Greed Index has climbed out of "Extreme Fear" territory, where it sat for most of February, into neutral. Macro conditions have eased. And the regulatory news this morning provides the clearest fundamental catalyst Bitcoin has had since ETF approval in January 2024.

The question now is whether the SEC/CFTC statement acts as a sustained inflow catalyst or a short-term spike. Historical data from January 2024 suggests that institutional allocators who were waiting on regulatory clarity tend to add over multiple quarters rather than days. If this morning's guidance holds and faces no legal challenge, the slow-drip institutional allocation could continue through Q2 and Q3 2026.

Source: Bloomberg ETF data; SoSoValue; Unchained Crypto, March 17, 2026

S&P 500 Trades On-Chain 24/7: Hyperliquid Lands the Biggest TradFi Name in History

Hyperliquid's rise to legitimate institutional venue: from $0 to $100 billion in total Trade[XYZ] volume in five months, capped by the S&P 500 perpetual launch.

While regulators were rewriting the rules in Washington, Hyperliquid was quietly doing something historic on-chain. S&P Dow Jones Indices - the organization that owns one of the most valuable financial benchmarks on earth - has officially licensed the S&P 500 index to Trade[XYZ] for use in a perpetual derivatives contract on Hyperliquid. This is the first officially sanctioned on-chain perpetual derivative based on a major equity index, anywhere, ever.

The word "official" matters enormously here. Previous attempts to bring S&P 500 exposure on-chain relied on synthetic pricing feeds that S&P Dow Jones Indices had no hand in. Those products were gray-area at best. This contract runs on institutional-grade index data sourced directly from S&P DJI, with a licensing agreement that gives the product legal and reputational legitimacy that no previous on-chain equity product has had.

"The deal signals something beyond product innovation: one of finance's most respected institutions has decided decentralized infrastructure is ready for flagship benchmarks." - Unchained Crypto, March 18, 2026

The contract trades 24 hours a day, 7 days a week. That alone is a structural first. The NYSE and Nasdaq close. CME S&P futures have overnight sessions but close on weekends. This perpetual never closes. For global investors outside U.S. time zones - Asia, Europe, the Middle East - this creates a real-time equity exposure product that traditional markets cannot match.

Access is currently restricted to eligible non-U.S. investors, consistent with U.S. securities regulations, but the international market is large. S&P DJI Chief Product Officer Cameron Drinkwater cited the need for "deep liquidity and institutional confidence at scale" - and Trade[XYZ] has the track record to support that confidence. The platform has crossed $100 billion in total trading volume since launching on Hyperliquid in October 2025, running at an annualized rate above $600 billion.

Earlier this month, an oil perpetual on Hyperliquid briefly generated more daily trading volume than the entire Ethereum network. That was the data point that convinced traditional finance that decentralized venues were real competitors, not curiosities. The S&P 500 license is the direct consequence of that proof-of-concept.

Source: Unchained Crypto, March 18, 2026; Trade[XYZ] volume data; S&P Dow Jones Indices press materials

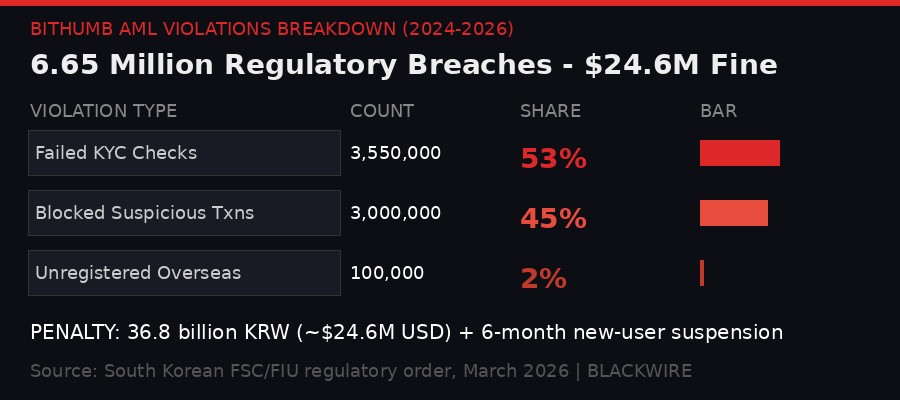

Bithumb's $24M Fine: South Korea Puts an End to AML Theater

Breakdown of Bithumb's 6.65 million regulatory violations identified by South Korean regulators. The exchange received a $24.6M fine and a six-month new-user suspension.

The regulatory clarity arriving in the U.S. stands in sharp contrast to the enforcement hammer South Korea just dropped on its domestic crypto sector. Bithumb - South Korea's second-largest cryptocurrency exchange by volume - has been hit with a 36.8 billion won fine, approximately $24.6 million at current exchange rates, and a six-month ban on accepting new users after regulators identified 6.65 million anti-money laundering violations.

The scale of the violations is extraordinary. Regulators identified 3.55 million instances where Bithumb failed to complete mandatory customer identity verification - KYC checks that every regulated financial platform is legally required to perform. A further 3 million transactions were processed despite clear signals of suspicious activity that should have triggered automatic blocks. The exchange also processed tens of thousands of transfers involving unregistered overseas cryptocurrency firms, which Bithumb had been warned about repeatedly before regulators formally intervened.

The penalty structure extends beyond the institution itself. Bithumb's CEO received a formal reprimand from the Financial Intelligence Unit. The compliance officer was suspended. Both are unusual steps in South Korean regulatory practice and signal that authorities are moving toward personal accountability frameworks - a shift that mirrors post-2008 financial regulation trends in the U.S. and Europe.

BITHUMB REGULATORY PENALTY SUMMARY

Bithumb is not alone. South Korean regulators have handed out similar AML enforcement actions against Upbit and Korbit over the past 12 months, making clear this is a systemic campaign rather than targeted prosecution. The pattern mirrors what happened to European banks from 2014-2018, when regulators moved from institution-level fines to industry-wide enforcement sweeps.

For retail users, the six-month suspension targets new account registrations only. Existing Bithumb users can continue trading and withdrawing funds normally. This distinction is important - a full suspension would have triggered a bank-run dynamic. The partial suspension is calibrated to punish without precipitating a liquidity crisis, which suggests regulators are threading a needle between enforcement and market stability.

The broader implication for global crypto exchanges is unambiguous: AML compliance is no longer optional theater. South Korea's Financial Services Commission and Financial Intelligence Unit now have a documented track record of actually counting violations and pricing them accordingly. At $24.6 million, the fine is large enough to hurt but not existential. The next exchange to accumulate 6 million violations after this public example should expect the calculus to shift.

Source: South Korean FSC/FIU regulatory order; Unchained Crypto, March 17, 2026

Reg Crypto Safe Harbor: What Comes Next for Token Issuers

The SEC and CFTC joint statement hints at a significant forthcoming mechanism: a "Reg Crypto" safe harbor for new token issuers. Details are preliminary, but the concept mirrors the existing Regulation A+ and Regulation D exemptions that allow smaller companies to raise capital without full SEC registration. A Reg Crypto safe harbor would give projects a defined compliance pathway - register the basic terms of your token, disclose material facts, meet minimum decentralization milestones, and avoid criminal liability during a grace period while you build.

Legal expert Jake Chervinsky flagged this element specifically on X following the announcement, calling it one of the most consequential elements of the guidance. The current environment forces projects to choose between two bad options: register as a full security (expensive, slow, restrictive), or launch without clarity and hope you don't get a Wells Notice two years later. A Reg Crypto framework eliminates both of those failure modes.

The timing of the safe harbor proposal matters as much as the substance. U.S.-based token launches have been declining for three years as founders chose to incorporate offshore - in the Cayman Islands, Switzerland, or the UAE - specifically to avoid the SEC enforcement risk. A defined safe harbor brings those projects back onshore, back into U.S. legal infrastructure, and back into U.S. tax jurisdiction. That is a strong fiscal argument that the Treasury Department will be sympathetic to, regardless of ideology.

The CFTC also issued a separate no-action letter confirming that non-custodial wallets do not qualify as intermediaries under the Commodity Exchange Act. That ruling, paired with the Phantom precedent, creates a complete picture: if your software does not hold user assets and does not act as a counterparty, you are likely outside the registration regime entirely. Build self-custodial, deploy non-custodially, and the regulatory apparatus largely leaves you alone.

For Ethereum's DeFi ecosystem specifically, this is transformative. Uniswap's front-end has been under SEC investigation since 2023. Aave, Compound, and other protocol interfaces have operated in legal uncertainty for years. The combination of the joint taxonomy plus the CFTC wallet ruling creates a strong defense for each of them - one that their legal teams are almost certainly already drafting memos around.

Source: Jake Chervinsky via X, March 18, 2026; SEC/CFTC Joint Staff Statement; Unchained Crypto

Timeline: How the U.S. Crypto Regulation War Was Won

SEC Chairman Jay Clayton declares most ICO tokens are securities. Enforcement actions proliferate. Industry operates under a "regulation by lawsuit" framework with no published rules.

SEC Chair Gary Gensler asserts nearly all crypto assets except Bitcoin are securities. Files suits against Coinbase, Kraken, Binance, Ripple, and dozens of others. Calls crypto the "Wild West." Industry relocates offshore en masse.

SEC approves 11 Bitcoin spot ETFs simultaneously. BlackRock's IBIT launches. $10 billion flows in within 30 days. Institutional legitimacy arrives at scale.

Trump wins the presidency on a crypto-friendly platform. Gensler resigns effective January 20, 2025. Paul Atkins nominated as SEC Chair with explicit mandate to end regulation-by-enforcement.

SEC drops active suits against Coinbase, Kraken, Consensys, and others. CFTC signals cooperative approach. Industry cautiously optimistic but awaits formal guidance.

SEC and CFTC issue joint staff statement. Five-category token taxonomy published. Staking, mining, airdrops all explicitly excluded from securities treatment. Reg Crypto safe harbor previewed. Phantom wins non-custodial wallet precedent same day.

What Traders Need to Watch Right Now

The immediate trading implication is that the risk-discount priced into U.S.-adjacent crypto assets for the past three years starts unwinding. Projects that built offshore specifically to avoid SEC reach - and priced in that regulatory risk - now have room to redomicile, expand U.S. operations, and access U.S. capital markets more directly.

The ripple effect reaches into ETFs. A Bitcoin ETF exists. An Ethereum ETF got approved in 2024 but still trades at a discount to NAV attributable partly to regulatory risk. With ETH now unambiguously in the "digital commodity" category under CFTC jurisdiction, that risk discount should compress. Watch ETHA and ETHW for flow acceleration.

The Hyperliquid S&P 500 perpetual creates a new vector for on-chain derivatives exposure that was not previously available at institutional scale. Global investors who cannot easily access U.S. equity markets now have a licensed, 24/7 perpetual backed by S&P Dow Jones data. The premium over other on-chain synthetic products will compress as liquidity builds, but in the near-term, this product will attract volume from TradFi institutions testing on-chain infrastructure.

Three numbers to track into Q2 2026: (1) Spot BTC ETF weekly net flows - watch for sustained $200M+ days as the indicator of post-guidance institutional demand; (2) Uniswap front-end trading volume - a proxy for how quickly the DeFi ecosystem reprices its regulatory risk; (3) U.S.-domiciled token project announcements - the safe harbor preview should trigger a wave of projects repatriating from the Cayman/Swiss structure.

Bithumb's $24M fine and South Korea's broader AML crackdown serve as a useful counterweight to U.S. optimism. Regulatory clarity in the U.S. does not mean regulatory permissiveness globally. Exchanges operating in multiple jurisdictions face an increasingly fragmented compliance landscape: crypto-friendly rules in the U.S., aggressive AML enforcement in South Korea, MiCA's structured framework in Europe, and total bans in a handful of emerging markets.

The projects and platforms that win the next cycle will be those that treat compliance as infrastructure rather than overhead - built in from the architecture layer, not bolted on after the fact. The SEC and CFTC just made it clear they reward that approach. The Bithumb enforcement action made it equally clear they punish the opposite.

Today's news is not a destination. It is a starting line. Five years of regulatory war has ended. The next five years will determine whether the industry uses this opening to build something legitimate at scale - or whether new actors find new ways to invite the next crackdown. The regulatory environment is more favorable than it has ever been. What happens with that advantage is the story.

Sources: SEC/CFTC Joint Staff Statement March 18, 2026; Unchained Crypto (multiple reports March 17-18, 2026); Bloomberg ETF data; S&P Dow Jones Indices / Trade[XYZ] announcement; South Korean FSC/FIU enforcement order

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram