RAMmaggedon: Tariffs and Memory Price Spikes Are About to Kill the Budget PC Market

Three major analyst firms now agree: PC shipments will drop 10-12% in 2026 - the worst collapse in over a decade. Tariff-driven memory price surges just made every cheap laptop a lot more expensive. The era of the $300 computer may be over.

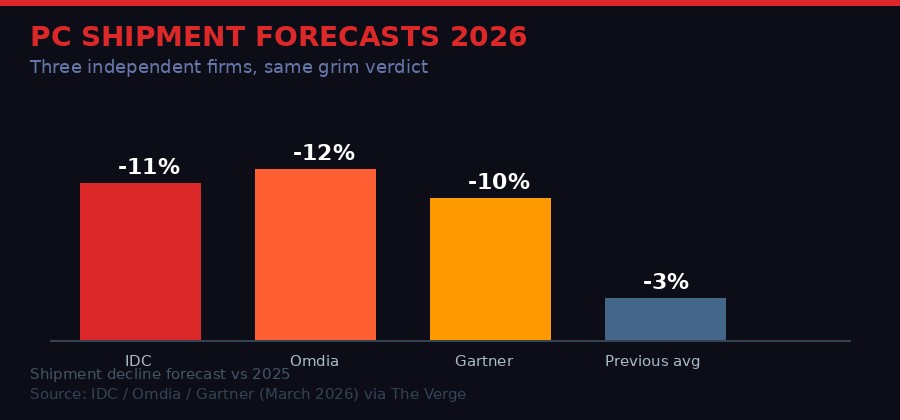

Three firms, one verdict: the 2026 PC market is heading for its worst year in over a decade. BLACKWIRE / nixus.pro

The numbers landed this week like a verdict nobody wanted to read. IDC, Gartner, and Omdia - three firms that rarely agree on anything beyond broad trends - published their 2026 PC market forecasts within days of each other. IDC: shipments down 11%. Omdia: down 12%. Gartner: down 10%.

That kind of consensus is unusual in analyst circles. When three independent research firms drawing on separate data sets converge on the same catastrophic number, the signal is hard to dismiss. The PC market is heading for its steepest decline since the post-pandemic crash of 2022, and the cause this time is not a hangover from pandemic buying. It is something more structural, more policy-driven, and harder to reverse.

The term circulating in supply chain circles is "RAMmaggedon" - a convergence of tariff pressure, memory supply constraints, and AI infrastructure competition that has pushed DRAM prices to levels not seen since the shortage years of 2017-2018. The difference is that this time, the price spike is manufactured. It is not a demand surge. It is the deliberate outcome of trade policy colliding with a market that was already stretched thin.

IDC, Omdia, and Gartner forecasts for 2026 PC shipments vs 2025 baseline. All three project the sharpest single-year decline in over a decade. BLACKWIRE analysis.

How We Got Here: The Tariff-Memory Chain Reaction

To understand RAMmaggedon, you have to trace the chain reaction backward. It starts not with a chip factory or a memory fab, but with a policy decision made in Washington - and the second and third-order effects that nobody in the executive branch appears to have modeled carefully before pulling the trigger.

The Trump administration's tariff regime, escalated through 2025 and now running at effective rates of 25-145% on various categories of Chinese electronics and components, created an immediate cost shock for PC manufacturers. But the effect on DRAM - the memory chips inside virtually every consumer PC sold globally - was not direct. It was indirect, and for that reason, much harder to see coming.

Most consumer DRAM does not come from China. It comes from South Korea (SK Hynix and Samsung) and the United States (Micron). But the fabrication of DRAM relies on a global supply chain of chemicals, substrates, and specialized equipment where Chinese suppliers play critical roles. Tariffs on upstream materials added cost throughout the chain. Combined with an ongoing reallocation of manufacturing capacity toward high-bandwidth memory (HBM) - the premium, AI-focused DRAM variant used in Nvidia's H100 and H200 chips - consumer DRAM supply tightened precisely when it needed to stay loose.

The result: DDR5 module prices climbed roughly 35-55% through late 2025 and into early 2026, according to spot market tracking from DRAMeXchange. Budget laptop makers, who operate on notoriously thin margins, absorbed some of that. Then passed the rest on.

"The era of bargain-priced PCs and tablets is behind us." - Sean Hollister, The Verge, March 12, 2026, summarizing IDC, Omdia, and Gartner analyst findings

The HBM Factor: AI's Appetite Is Eating Your Laptop's Memory

There is a second story buried inside RAMmaggedon, and it is one the chip industry has been reluctant to discuss openly: the AI infrastructure buildout is directly cannibalizing the consumer PC memory market.

High-bandwidth memory - HBM2e, HBM3, and now HBM3e - is manufactured on the same underlying DRAM substrate as conventional DDR5 and LPDDR5. The raw silicon and process steps are similar. The key difference is in packaging: HBM stacks multiple DRAM dies vertically and connects them with through-silicon vias (TSVs), creating the extremely high-bandwidth, low-latency memory that AI accelerators need.

Building HBM is dramatically more complex and expensive than building standard DRAM. But for memory fabs like SK Hynix, it is also dramatically more profitable. Hynix's HBM3e sells to Nvidia for prices that dwarf what it earns on DDR5 modules destined for Lenovo or HP laptop assembly lines.

The economic logic is inescapable: when AI infrastructure demand surges, memory fabs shift capacity to HBM. Consumer DRAM supply tightens. Prices go up. Laptop makers either absorb the cost - cutting margins to near zero - or pass it through. Most are now passing it through.

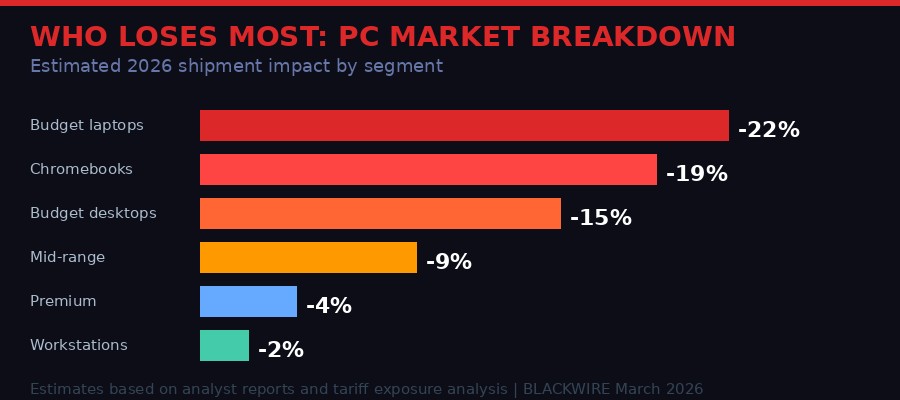

Who Gets Hurt Most: A Segment-by-Segment Breakdown

Not all PC segments are equally exposed. The damage lands hardest at the bottom of the market - precisely where most buyers live.

Budget and education-focused PC segments face the steepest volume declines as price-sensitive buyers hit affordability walls. BLACKWIRE analysis.

Budget laptops (sub-$500): The hardest-hit segment. These machines rely on the thinnest margins, the cheapest DRAM configurations, and the most price-sensitive buyers. A $40 memory cost increase on a device that sold for $329 a year ago either kills the price point or kills the product. Many SKUs are being discontinued rather than repriced. Estimated 2026 volume decline: 20-25% in this segment alone.

Chromebooks: Arguably the most vulnerable platform. Chromebooks exist precisely because of their price point. The entire product category was engineered to compete at the $200-350 level. Google's ChromeOS is built around the assumption of cheap, low-RAM hardware. Memory price spikes attack that assumption at the root. IDC's forecast specifically flagged Chromebook volumes as a primary source of the overall PC market decline. Education buyers - school districts, public institutions - are unlikely to absorb price increases. They will simply buy fewer devices.

Tablets (counted in some analyst forecasts): The Verge's headline mentioned "PCs and tablets," and the memory price spike hits iPad and Android tablet alternatives similarly. Budget Android tablets from Lenovo, TCL, and Amazon's Fire line all rely on LPDDR4X and LPDDR5 configurations where cost increases directly threaten price accessibility.

Mid-range ($700-1200): Shielded somewhat by higher margins. A $50 memory increase on a $999 laptop is painful for manufacturers but does not necessarily kill consumer demand. Expect volume declines of 8-12% in this band - significant, but not catastrophic.

Premium and workstations ($1500+): Largely insulated. Buyers at this level are less price-sensitive, and the memory component as a percentage of total BOM (bill of materials) is smaller. Professional workstation segments may actually see modest growth as organizations that cannot afford to cut computing needs shift spending upmarket rather than buying multiple cheap units.

| Segment | Typical Price Point | DRAM Cost Exposure | Estimated 2026 Volume Impact |

|---|---|---|---|

| Chromebooks | $200-350 | Very High | -18 to -22% |

| Budget Laptops | $350-500 | Very High | -20 to -25% |

| Budget Desktops | $400-650 | High | -14 to -18% |

| Mid-Range Laptops | $700-1200 | Medium | -8 to -12% |

| Premium / Gaming | $1200-2500 | Low | -3 to -5% |

| Workstations | $2500+ | Very Low | -1 to +2% |

Estimates based on analyst data from IDC/Omdia/Gartner and DRAM spot market analysis. March 2026.

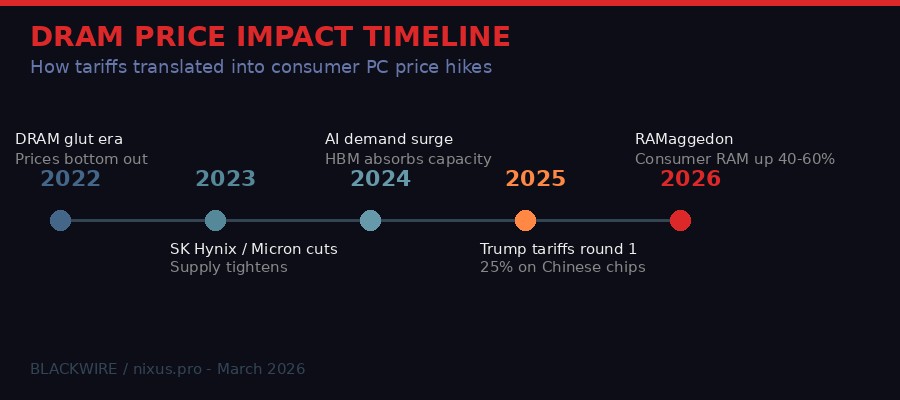

The DRAM Price Timeline: How We Got to RAMmaggedon

The path to RAMmaggedon: five years of DRAM market dynamics converging on a single shock event. BLACKWIRE analysis.

The memory industry runs in well-documented cycles. Oversupply leads to price crashes. Fabs cut production. Supply tightens. Prices recover. Rinse and repeat, roughly every three to five years. The cycle has been running this way since the 1990s.

What is different now is the introduction of a structural distortion that does not follow cycle logic: AI infrastructure demand.

2022-2023: The Great DRAM Glut

Post-pandemic demand collapse leaves memory fabs with massive overstock. DDR5 prices fall to near cost-of-production levels. PC makers enjoy one of the best memory pricing environments in years. Budget devices proliferate.

Late 2023: AI Flips the Script

ChatGPT's explosion in enterprise adoption drives unprecedented HBM demand. SK Hynix wins Nvidia's HBM3e qualification. The race to supply AI accelerators begins reallocating fab capacity away from commodity DRAM.

2024: Supply Tightens Quietly

Consumer DRAM spot prices begin climbing as HBM production absorbs an increasing share of total wafer output. The shift is gradual enough that PC OEMs continue forward-pricing based on legacy contracts. The problem is building beneath the surface.

2025: Tariffs Arrive, Contracts Expire

Trump's tariff escalation on Chinese electronics components - including upstream memory supply chain materials - adds 10-20% cost pressure across the board. Legacy OEM supply contracts begin expiring. New contracts are negotiated at sharply higher memory prices. The squeeze begins in earnest.

Q1 2026: RAMmaggedon

Budget PC prices hit a wall. Entry-level configurations that sold for $299-349 in 2024 now require $380-430 to maintain margins. Consumer demand collapses at the margin. IDC, Gartner, and Omdia all publish their revised forecasts: down 10-12% for the full year. The era of cheap computing, as Verge's Sean Hollister put it, is behind us.

The Geopolitical Dimension: Tariffs as Tech Policy

RAMmaggedon did not happen by accident. It is the predictable downstream consequence of using tariffs as a blunt instrument in a trade conflict that involves some of the most interconnected supply chains in human history.

The stated goal of the Trump tariff regime is to reshore manufacturing - to bring chip and electronics production back to American soil. In some narrow respects, this goal has made progress: Intel's CHIPS Act-funded fabs in Ohio and Arizona represent genuine domestic capacity expansion. Micron's new fabrication facility in Idaho, backed by $6.1 billion in federal grants announced under the CHIPS Act, will eventually add meaningful DRAM capacity to the US supply chain.

But "eventually" is doing enormous work in that sentence. These facilities take three to five years to build, qualify, and ramp to volume production. The tariff pain is happening now. The domestic supply benefit is happening in 2027 at the earliest, and more realistically 2028-2029 for meaningful volume. In the meantime, American consumers are absorbing the cost of a trade war that is supposed to benefit them.

The political economy of this is worth examining carefully. Budget PC buyers skew heavily toward lower-income households, students, and small businesses. These are not the demographics that can easily absorb $100-200 price increases on entry-level devices. The Chromebook market, in particular, has been a lifeline for schools and districts that could not otherwise afford computing infrastructure for students. If Chromebook volumes collapse 20% in 2026, the educational technology gap - already significant before the pandemic - widens further.

"Tariffs are supposed to protect American industry from foreign competition. But when the product being taxed is a critical input for education, small business, and digital participation in the economy - you have to ask who, exactly, is being protected." - BLACKWIRE analysis, March 2026

Microsoft's Pivot and the Windows on ARM Gamble

Against this backdrop, Microsoft's decision to reorganize its Windows and Surface leadership - moving both divisions to report directly to CEO Satya Nadella - takes on a sharper meaning. The Verge reported this week that the leaders of Windows and Office are now getting promoted and report directly to Nadella, a structural signal that Microsoft is treating the PC platform as a top-tier strategic priority again after years of treating it as a cash-sustaining legacy business.

The timing is not coincidental. Microsoft is betting that Windows on ARM - powered by Qualcomm's Snapdragon X processors and, potentially, its own silicon efforts - offers an escape route from the RAMmaggedon trap.

Qualcomm's Snapdragon X series uses LPDDR5x memory in configurations optimized for power efficiency rather than raw bandwidth. The memory subsystems in these chips are designed differently from x86 PC architectures, and Qualcomm's deep integration with Asian manufacturing partners - particularly Taiwan's TSMC - gives it more supply chain flexibility than Intel or AMD's platform dependencies allow.

ARM-based Windows PCs, if they can achieve broader software compatibility (the ongoing challenge), represent a structural alternative to the Intel-AMD-DRAM supply chain that is currently bleeding budget PC buyers. Apple demonstrated with the M-series that ARM can deliver competitive performance at dramatically better power efficiency. The question is whether Qualcomm can replicate that for Windows at the low end of the market where RAMmaggedon is doing the most damage.

The answer, at current Snapdragon X pricing, is: not yet. The cheapest Snapdragon X-based Windows devices still retail for $700 or more. Getting ARM-on-Windows to sub-$500 is a product development challenge that Microsoft and Qualcomm have been working on but have not yet solved. The DRAM crisis adds urgency to that challenge.

What Happens Next: Three Scenarios for the PC Market

The analyst forecasts paint a grim 2026. But forecasts are not fate. Three scenarios are plausible for how this plays out over the next 12-24 months.

Scenario 1: Extended pain, slow recovery (most likely) - Tariffs remain in place, Micron and SK Hynix slowly expand consumer DRAM capacity as HBM demand eventually plateaus, and prices gradually normalize through 2027. The PC market bottoms in Q3 2026 and begins a modest recovery in 2027. Budget devices return, but at permanently higher price floors. The $300 laptop becomes the $380 laptop for the foreseeable future. Digital access inequality widens in the interim.

Scenario 2: Policy reversal accelerates recovery - A tariff carve-out for electronics components - possible but not currently signaled by the administration - provides immediate relief. Memory prices stabilize in H2 2026. PC makers reprice aggressively to rebuild market share. Recovery happens faster than analysts currently expect. This scenario requires political will that is not currently evident.

Scenario 3: Structural market transformation - The RAMmaggedon shock accelerates the transition to cloud-first, thin-client computing. Instead of buying a $400 laptop, consumers and schools increasingly rely on browser-based applications, Chromebook-like devices with minimal local processing, and subscription computing models. This scenario actually benefits some players - Google's cloud services, Microsoft's 365 ecosystem, and streaming compute providers - while permanently shrinking the traditional PC hardware market. The hardware recovers in volume, but at lower ASPs and with fundamentally different margin structures.

The Overlooked Victims: Education Technology and Digital Equity

Every conversation about the PC market eventually has to confront the education question, and the analysts' forecasts are no exception. IDC specifically called out budget devices and Chromebooks as the primary source of the 2026 decline. These products do not primarily sell to tech enthusiasts or enterprise IT departments. They sell to schools.

The post-pandemic era saw an enormous expansion in school technology access, driven by emergency federal funding (ESSER funds) and the recognition that students without devices were effectively locked out of education during remote learning periods. Chromebooks went from a niche product to the dominant computing platform in K-12 education in the United States, with over 50 million devices deployed in schools according to Google's most recent available data.

Those devices are now three to five years old. The normal replacement cycle would see schools buying new Chromebooks in 2025-2026. But ESSER funds have expired. Budget constraints have tightened at the district level. And now the devices themselves cost 20-30% more than they did at the last purchasing cycle.

The arithmetic is brutal. A school district that budgeted $280 per device for a 5,000-unit Chromebook refresh - a $1.4 million line item - now faces a $350-380 per unit reality. That is $1.75 to $1.9 million for the same purchase. Not every district can find that extra $400,000 in a budget cycle that has already been squeezed by inflation, staffing costs, and the end of federal emergency relief.

The result: technology refresh cycles get extended. Devices that should have been retired run for another two to three years. Students use machines that are too slow for modern web applications. The performance gap between well-funded suburban schools and under-resourced urban or rural districts - already significant - grows larger. This is not a footnote. It is one of the central consequences of trade policy that optimizes for domestic semiconductor production while ignoring the downstream effects on how Americans actually access computing.

Industry Response: Who Is Adapting and How

The major PC OEMs are not standing still while their market collapses. Lenovo, HP, and Dell have all moved to diversify their component sourcing, accelerating deals with non-Chinese memory suppliers and exploring longer-term fixed-price contracts with both Micron and SK Hynix to reduce exposure to spot market volatility.

Lenovo, the world's largest PC maker, has been the most aggressive. The company has expanded its use of Micron's US-manufactured DDR5 and LPDDR5, partly for supply security and partly as a marketing differentiator in markets where "made with US components" carries value in procurement decisions. Lenovo's ThinkPad line has always commanded premium positioning, and the company is leaning into that: if budget PC margins are getting compressed to zero, Lenovo's strategy is to move upmarket rather than defend the bottom.

HP is taking a different approach, doubling down on its managed print and enterprise services business to compensate for PC hardware margin pressure. The company's 2025 annual report explicitly identified memory price volatility and tariff uncertainty as material risks - unusual specificity for a company that has historically been vague about supply chain dynamics in public disclosures.

Dell's commercial focus gives it more insulation than consumer-heavy rivals. Enterprise IT buyers are less price-sensitive than retail consumers, and they work on longer procurement cycles that allow Dell to hedge supply costs more effectively. Dell is also betting heavily on AI PCs - devices with dedicated neural processing units (NPUs) designed to run AI workloads locally - where the higher average selling prices help offset component cost increases.

The wild card is ASUS, Acer, and the Taiwan-based OEM ecosystem. These companies compete primarily on price and volume, especially in emerging markets where budget PCs are not a lifestyle choice but a necessity. They have the least room to maneuver. Several Acer models slated for Q2 2026 have quietly been delayed as the company works out whether the pricing works at all.

The Signal in the Noise: What RAMmaggedon Tells Us About Technology's Future

RAMmaggedon is not just a market story. It is a diagnostic. It reveals what happens when the assumptions embedded in decades of globalized supply chain optimization get suddenly stress-tested by policy shifts that move faster than manufacturing can adapt.

The PC market - broadly understood as a mature, boring, commodity business - turns out to be more fragile than it looked. Thin margins, complex supply chains, and reliance on a handful of dominant memory producers in a handful of countries create systemic brittleness. Add tariffs, stir in AI-driven capacity reallocation, and the whole stack wobbles.

The second-order effects spread outward from that wobble in ways that are harder to see than the headline numbers. Education technology gaps. Digital equity disparities. Chromebook market restructuring. Microsoft's forced strategic pivot toward ARM and cloud-first computing. The death of the $300 laptop as a product category.

None of these are permanent. Markets adapt. Manufacturers find workarounds. Policy can change. But adaptation takes time, and in the meantime, the people who feel the squeeze most are not the ones best positioned to wait it out.

The firms calling this RAMmaggedon are not being dramatic. They are being accurate. A market that was supposed to recover from its pandemic hangover and ride an "AI PC" upgrade supercycle is instead facing its worst contraction in a decade, caused not by a product problem or a demand collapse, but by the quiet friction of geopolitics moving through a semiconductor supply chain that was never designed to absorb it.

Budget computing was one of the genuinely democratizing forces in technology over the past two decades. The $200 laptop connected more people to the internet, to education, and to economic opportunity than any government program managed. Watching that access point get squeezed by the intersection of trade war and AI investment boom is not just a market forecast story. It is a story about who gets to participate in the digital economy, and who gets left behind while the rest of us argue about chip sovereignty.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSources & References:

IDC, Omdia, and Gartner 2026 PC market forecasts (March 2026) via The Verge / Sean Hollister. DRAMeXchange DRAM spot pricing data Q4 2025-Q1 2026. Micron Technology CHIPS Act grant announcement ($6.1 billion, Idaho fab). SK Hynix HBM3e supply agreements (public filings 2024-2025). Google Chromebook deployment data (50M+ K-12 units, per company disclosures). Lenovo, HP, Dell annual reports 2025 (supply chain risk disclosures). The Verge (March 12, 2026): "'The era of bargain-priced PCs and tablets is behind us': PC shipments expected to drop 11 percent." Microsoft organizational restructuring: Windows and Office leaders to report directly to Satya Nadella, The Verge March 12, 2026.