Quadruple Witching, Bitcoin at $69K, DeFi Burns: The March 20 Convergence

$600 million in deep-out-of-the-money Bitcoin puts expire today on the biggest options event of the quarter. Oil is up 4% on Iran war headlines. Gold is cracking. A DeFi hacker spent nine months engineering a $15 million heist and walked away down $4.7 million. Chris Larsen is using a billion-dollar nonprofit to pump an XRP stock onto Nasdaq. Bank of America's CEO says $6 trillion in deposits could migrate to stablecoins. It's quadruple witching Friday and the market is running on chaos.

Bitcoin's $69,000 hold through this week's geopolitical turmoil has surprised even bearish analysts. Photo: Pexels

Section 1: What Quadruple Witching Actually Means for Crypto

Options expiry events historically drive short-term volatility regardless of underlying fundamentals. Photo: Pexels

Quadruple witching happens four times a year - the third Friday of March, June, September, and December. It's when stock index futures, stock index options, single-stock futures, and single-stock options all expire simultaneously. For traditional equity markets, it's always a high-volume, high-volatility session. In 2026, it hits with crypto riding shotgun.

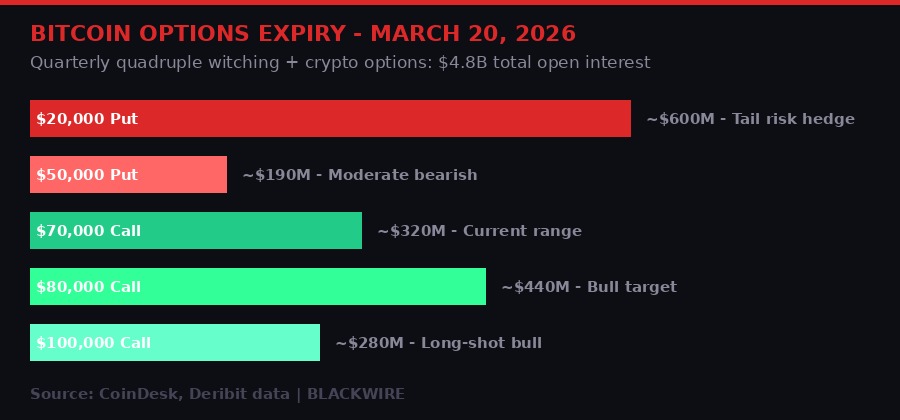

Crypto options have their own expiry calendars but they've become increasingly synchronized with tradfi cycles as institutional participation deepens. March 20 carries roughly $4.8 billion in Bitcoin and Ethereum open interest, with the single largest position being a cluster of $20,000 put options totaling approximately $600 million in notional value, according to CoinDesk reporting citing Deribit data.

That $20K put number is the one everyone's talking about. It's deep out of the money - Bitcoin would need to fall 71% from current levels to be in play. But the sheer volume of that strike tells a story about where professional risk managers are hedging their tail scenarios. These aren't retail punters buying lottery tickets. Institutional desks buying $20K puts are pricing in scenarios where the Iran war escalates to oil infrastructure collapse, where US credit conditions seize up, or where some as-yet-unknown macro shock surfaces. The options market is basically saying: we don't think it happens, but if it does, we want protection.

Wintermute's Bryan Tan put it plainly in comments to CoinDesk: "While bitcoin has shown relative strength against gold since the war in Iran broke out, investors are better off holding off dry powder while prices swing wildly on headlines." Translation - the smart money is watching, not loading up. Dry powder over FOMO right now.

Options positioning by strike price heading into March 20 quadruple witching. The $20K put cluster is the most-discussed tail risk bet. Source: CoinDesk/Deribit, BLACKWIRE graphic.

Historical data from 2025 is worth checking. Quadruple witching days last year showed muted Bitcoin performance on the session itself - but weakness in the days to weeks following. The market digests the expiry, positions reset, and then the underlying trend reasserts. What that means for March 20-27 depends entirely on how oil and the Iran situation play out, which brings us to the macro picture.

Section 2: The Iran Shock - Oil, Gold, and Why Bitcoin Held

Crude oil markets absorbed the Iran war shock faster than many traders expected, with WTI holding elevated but not spiraling. Photo: Pexels

Oil is up roughly 4% on the week, sitting at elevated levels following the US strikes on Iranian facilities that BLACKWIRE covered earlier this month. The expected spiral to $200/barrel hasn't materialized - Iranian production disruption has been real but not catastrophic, and Saudi Arabia moved quickly to signal it would increase output to offset supply gaps.

Gold was supposed to be the war trade. It's not working. Gold tumbled this week as traders rotated into - counterintuitively - Bitcoin and US Treasuries. The Bitcoin relative strength play versus gold is one of the more interesting data points of 2026. Since the war headlines broke, BTC is down less than gold on a percentage basis and has recovered faster.

There are two ways to read this. The optimistic read: Bitcoin is finally being treated like a macro hedge by institutional investors who see it as a store of value with a supply ceiling. The pessimistic read: this is a momentum carry trade that will reverse hard the moment liquidity conditions tighten. Jerome Powell and the Fed have kept rates steady, which has compressed dollar strength and given risk assets more room to breathe.

"Bitcoin has shown relative strength against gold since the Iran war broke out... but investors are better off holding off dry powder while prices swing wildly on headlines." - Bryan Tan, Wintermute (via CoinDesk, March 19, 2026)

The $69,000 level is notable because it's acting as a magnet - below the cycle high BLACKWIRE covered in the February Strategy report ($75K-ish territory) but well above the crash lows when tariff panic hit in January. Bitcoin has carved out a holding range between roughly $66K and $75K through the Iran conflict, which for a war that was supposed to crater risk assets is actually impressive.

The question going into next week is whether the options expiry catalyzes a flush or a breakout. If the puts expire worthless - which they will unless something nuclear happens in the next 24 hours - dealers who sold those puts will no longer need to maintain hedges. That could free up capital for risk-on positioning. Or the market could just drift sideways as everyone waits for the next headline.

Section 3: The Venus Protocol Heist That Blew Up in the Hacker's Face

The Venus exploit required nine months of preparation - and ended with the attacker losing more than they stole. Photo: Pexels

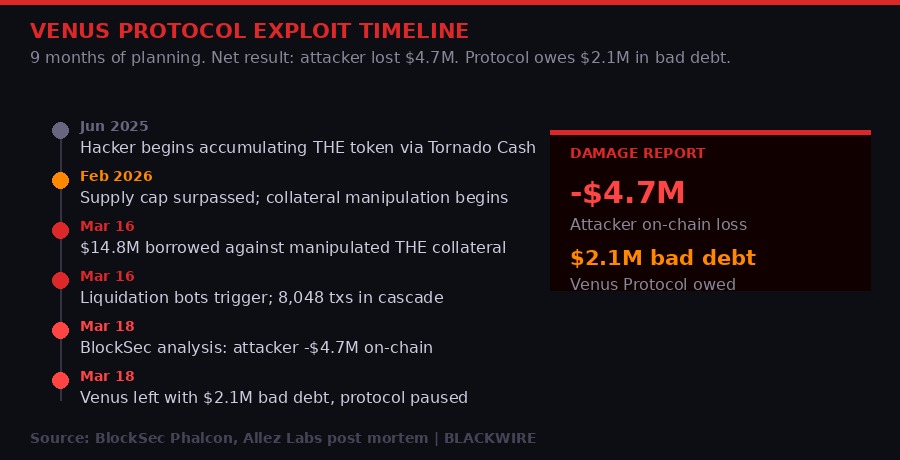

DeFi's week from hell delivered one of the stranger exploit stories in recent memory. A hacker spent nine months meticulously engineering an attack on Venus Protocol - the largest lending platform on BNB Chain with $1.45 billion in total value locked - and ended up losing $4.7 million of their own money in the process.

The technical breakdown from audit firm BlockSec is brutal: "254 bots, 8,048 liquidation txs, still $2.15M in bad debt. The attacker lost ~$4.7M on-chain. Both sides lost money."

Timeline of the Venus Protocol attack - from initial token accumulation in June 2025 to the March 2026 implosion. Source: BlockSec, Allez Labs, BLACKWIRE graphic.

Here's how it worked. The attacker began accumulating Thena's THE token starting around June 2025, funding purchases via Tornado Cash to obscure the trail. Over nine months they built up a massive THE position. The goal: exceed Venus Protocol's THE supply cap, which would let them manipulate the value of their collateral. Once the collateral was inflated, they borrowed approximately $15 million in assets against it.

Then the liquidation cascade happened. The attack triggered Venus' automated liquidation system. 254 bots piled in across 8,048 transactions, selling THE collateral into thin liquidity. The price of THE collapsed under the selling pressure. The attacker's $14.8 million borrow position was liquidated at a loss. By BlockSec's calculation, the attacker "invested $9.92 million and retained only approximately $5.2 million after all liquidations, an on-chain net loss of approximately $4.7 million."

"The on-chain picture is more complex than the widely-reported $3.7 million hack. Both the protocol and the attacker ended up losing money." - BlockSec Phalcon, post-mortem analysis (March 18, 2026)

There's a catch to the pure "hacker rekt himself" narrative: BlockSec notes the attacker may have had off-chain positions - short positions on THE via centralized exchanges - that profited from the price crash they engineered. One security researcher claimed to have made $15,000 just by watching the on-chain data and shorting THE in real time. If the hacker ran the same play at scale, their CEX profits could offset the on-chain losses. We don't know. Blockchain analysis can only see what's on-chain.

What makes this worse for Venus: Allez Labs' technical post-mortem confirmed the attack vector was identified in a 2023 Code4rena audit and explicitly dismissed as having "no negative side effects." Someone literally flagged this vulnerability three years ago. Venus didn't fix it. The $2.1 million in bad debt the protocol now carries is the invoice for that decision.

Venus has a documented history of bad luck and bad decisions. A $27 million phishing incident in September 2025. A $900,000 oracle manipulation attack in early 2025. Participation in the $14 million bad debt from the 2022 LUNA collapse. A looming $150 million BNB liquidation from the BNB Bridge hack. Venus keeps surviving, but each time it's messier. With $1.45 billion in TVL, this protocol is too big to ignore and apparently too stubborn to adequately fix its own vulnerabilities.

Section 4: Chris Larsen's Nonprofit Trick - Pumping XRP Stock Through a Tax-Exempt Shell

Ripple co-founder Chris Larsen's SEC disclosures reveal a layered structure connecting his nonprofit to a for-profit XRP treasury play heading to Nasdaq. Photo: Pexels

Ripple co-founder Chris Larsen has been quietly engineering a structure that connects his tax-exempt nonprofit - which holds $1.4 billion in assets and receives over $190 million in tax-deductible donations - directly to a for-profit XRP treasury company called Evernorth that's heading for a Nasdaq listing.

The vehicle is Armada Acquisition, a SPAC. The mechanics were buried in a 1,158-page SEC Form S-4 filed March 18 - but Protos got through it. The structure works like this: Larsen's nonprofit RippleWorks invested $500,000 cash plus 211 million XRP tokens into Arrington XRP Capital Fund LP, the SPAC's sponsor. RippleWorks holds a majority of the fund's limited partner interests. The fund's general partner is Michael Arrington's LLC - but by contract, Arrington is required to vote as RippleWorks directs.

Translated: Larsen's nonprofit effectively controls how the sponsor votes, and the sponsor controls Evernorth's Nasdaq listing. Larsen's Larsen Lam Children's Remainder Trust separately contributes 50 million XRP for 1.8 million Evernorth shares. Ripple itself is throwing in an additional 126 million XRP into the same vehicle.

"The economic interests of the Sponsor diverge from the economic interests of holders of the Public Shares." - Armada Acquisition Corp, SEC Form S-4 filing (March 18, 2026) - Larsen's own admission in the document

The S-4 is remarkably candid about the conflicts. Larsen's own risk disclosures state: "This structure may create potential conflicts of interest between Mr. Larsen's duties to Ripple, his influence over RippleWorks' investment in Arrington XRP Capital Fund, and the interests of Evernorth Holdings Inc. and its stockholders." He's essentially filing a document that says "here's the conflict, good luck."

For XRP holders who believe in the Ripple narrative, this news is complicated. On one hand, having a publicly listed XRP treasury company on Nasdaq is a bullish signal for XRP institutional adoption - more corporate entities holding XRP creates buy pressure. On the other hand, the structure reveals that Larsen is using a nonprofit that received hundreds of millions in tax-deductible donations to amplify his control over a for-profit enterprise that benefits him personally. RippleWorks CEO Doug Galen earned $845,945 in 2024 while the nonprofit derived 89% of its revenue from dumping donated XRP assets.

The SEC is reviewing the S-4. Whether they approve the listing as-is or require structural changes will be a signal about how aggressively the new administration's pro-crypto posture overrides traditional conflict-of-interest disclosure requirements. Watch this one closely.

Section 5: Bank of America's $6 Trillion Warning and the Coinbase GENIUS Act Standoff

Bank of America CEO Brian Moynihan's stablecoin warning is the clearest signal yet that traditional banking sees crypto as an existential threat to deposit funding. Photo: Pexels

Bank of America CEO Brian Moynihan made headlines this week with a warning that deserves more attention than it's gotten: $6 trillion in deposits could potentially migrate into stablecoins if the regulatory framework around them becomes too permissive. That's roughly 12% of total US commercial bank deposits. For context, the 2008 financial crisis was triggered by disruptions to about $600 billion in money market funds. A $6 trillion deposit migration would be a different kind of catastrophe.

Moynihan isn't arguing against stablecoins out of principle - Bank of America has its own stablecoin development underway. He's arguing against stablecoins that pay yield. The GENIUS Act, currently moving through Senate, contains provisions that some analysts say could ban yield-bearing stablecoins. That's where Coinbase enters the picture.

The scale of what's at stake: $6 trillion in US bank deposits versus a $230 billion stablecoin market. If even 10% migrates, it reshapes banking. Source: BLACKWIRE graphic.

Coinbase threatened this week to pull its support for the GENIUS Act stablecoin bill over the yield provision. USDC - Coinbase and Circle's stablecoin - generates substantial revenue for Coinbase by parking the dollar reserves in yield-bearing Treasuries and sharing that revenue with the exchange. If the GENIUS Act bans stablecoin issuers from passing yield to holders, Coinbase's entire USDC revenue model gets restructured.

There's a reported loophole being discussed - a "rewards" structure where Coinbase pays customers a return from its own balance sheet rather than from USDC yield directly. Analysts told CoinDesk this could protect the revenue stream even under the bill's current language. But it's legally untested and depends on how regulators interpret the distinction between "yield" and "rewards." That's a lot of regulatory risk to build a revenue model on.

The broader stablecoin legislative battle is getting complicated fast. The Crypto Clarity Act is simultaneously inching toward a Senate hearing, with White House involvement and lawmakers reportedly weighing bank-friendly provisions as a quid pro quo for bank support. Banks want one thing: if stablecoins are going to exist, they want them to be bank-issued, bank-regulated, and non-yielding to prevent deposit migration. Crypto companies want the opposite. This is the battle that will define the next decade of American financial infrastructure.

"The proposed rules could ban yield on stablecoins like USDC, though analysts say the exchange may adapt." - CoinDesk analysis, March 19, 2026

Barclays made a small but significant move into this space this week, taking a stake in UK-based stablecoin startup Ubyx. A major European bank making its first stablecoin investment is a signal that the traditional finance sector is choosing to participate rather than lobby for prohibition. When Barclays puts money in, it means their legal and regulatory teams believe stablecoins will exist and be regulated, not banned. That's a different posture than most US banks have taken publicly.

Section 6: Ben Delo's Westminster Play - Crypto Money Enters UK Politics

Ben Delo's Westminster hub sits in rooms overlooking Westminster Abbey, used for right-wing political events kept deliberately off public lobby plaques. Photo: Pexels

Ben Delo, co-founder of BitMEX, was pardoned by President Trump last year as part of the administration's crypto industry outreach. Delo had been convicted for failing to implement Bank Secrecy Act-compliant money laundering checks at BitMEX - a conviction that cost him significant legal fees and time, but ultimately less than two years in legal limbo before the pardon.

What Delo has been doing with his freedom is notable. An investigation by The Guardian and HOPE not hate reveals he's been funding a Westminster political hub called "The Sanctuary" - a suite of rooms overlooking Westminster Abbey where right-wing politicians, media figures, and controversial intellectuals are given free access for events, office space, and podcasting.

The Sanctuary has hosted Reform UK figures, race science publications, anti-abortion campaigners, and events connected to former Prime Minister Boris Johnson and Conservative leader Kemi Badenoch. Delo contributed £100,000 to The Battle of Ideas festival, which HOPE not hate characterizes as promoting "anti-science, anti-expert, and anti-public health positions."

The Sanctuary operates with deliberate opacity - its name doesn't appear on the building's lobby plaques, and users are reportedly instructed to keep quiet about it online. A photo of Delo's BitMEX pardon, signed by Trump, sits framed in the halls. One framed letter from Battle of Ideas founder Claire Fox calls Delo "our free speech hero."

The crypto-to-politics pipeline is not new. FTX money funded both sides of American politics before the collapse. Arthur Hayes of BitMEX donated to various libertarian causes before his own legal troubles. But the Delo story is different in texture - this isn't campaign contributions with disclosed donor lists. It's a private hub with an invite list and instructions to stay off social media about it.

For crypto's reputational standing in the UK - where regulators are already skeptical and a parliamentary committee recently called for a ban on crypto political donations - this story lands at a bad moment. The UK Financial Conduct Authority is watching. If Delo's activities get linked to specific policy outcomes or regulatory decisions, expect this to become a formal inquiry.

Section 7: The Quadruple Witching Playbook - What Happens Next

Options traders are watching the March 20 session closely - historical patterns suggest muted volatility on the day itself, followed by directional moves in the week after. Photo: Pexels

Pull back from the individual stories and the picture that emerges is of a market running at maximum complexity. Bitcoin at $69K is holding ground that looked impossible two months ago when tariff panic was sending everything into free-fall. But the holds are fragile and event-dependent in a way that should make any leveraged long nervous.

Options gamma reset after expiry can cut both ways. Dealers who were short gamma (sold puts) now have less hedging pressure - which could free capital for risk-on buying. Or they simply close books and flatten. Historically the week after quadruple witching has been rough for crypto.

Oil staying above $90/barrel would maintain inflationary pressure that keeps the Fed on hold. A Fed that doesn't cut isn't necessarily bad for Bitcoin, but it removes one of the near-term catalysts the market was pricing in for Q1 2026.

WATCH LIST: KEY EVENTS NEXT 7 DAYS

The through-line connecting all these stories is institutional pressure. Institutions are pricing tail risk through put options. Institutions are navigating whether to buy stablecoins or fight them. Institutions are watching DeFi's security failures with the practiced eye of people who already knew it wasn't ready for prime time. Institutions are funding political infrastructure to shape the regulatory environment they'll operate in.

Retail crypto holders are caught in the middle of all of it - their coins moved by forces they can barely track, on timelines set by options expiry calendars and Senate committee schedules. That's not a complaint. That's just what it means to be in an asset class that grew up from a cypherpunk experiment into a $2 trillion institutional battleground in fifteen years.

Bitcoin at $69K after everything that happened this week is actually a statement. Not of invincibility - the $600 million in $20K puts proves the market hasn't forgotten what catastrophe looks like. But of resilience. The Iran war, the tariff shock, the DeFi exploits, the legislative uncertainty - and we're still at $69K. That's the number people will remember if this level holds. If it doesn't, the $600M put buyers will have the last laugh.

Quadruple witching Friday. Hold onto something.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram