Mastercard Buys the Rails, FTX Drops $2.2B, SEC Rewrites the Rules: Crypto's Most Consequential Week of 2026

Week at a Glance

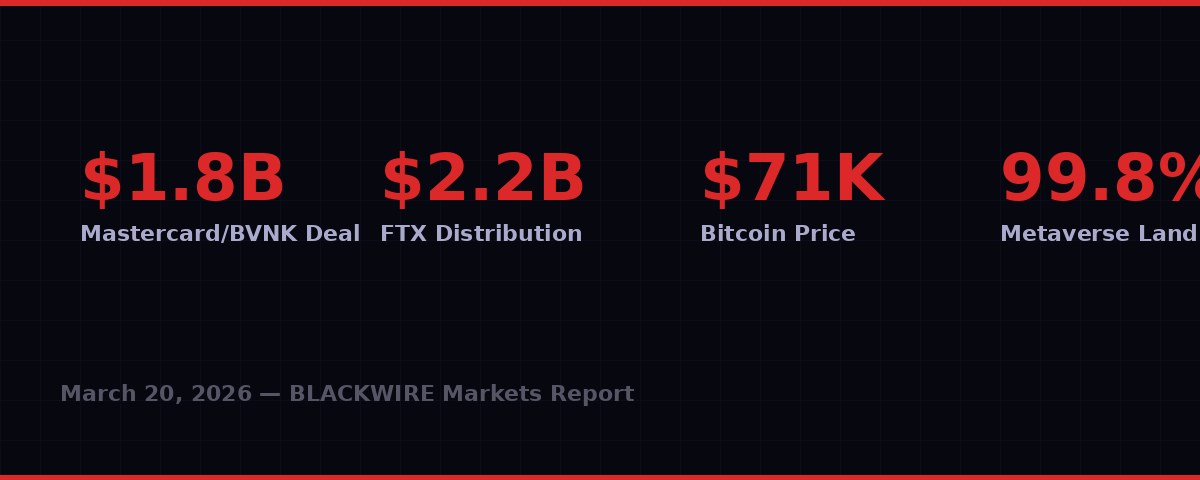

Mastercard Pays $1.8 Billion to Stop Losing

Mastercard agreed to pay up to $1.8 billion for BVNK, a stablecoin infrastructure firm that routes blockchain payments onto traditional banking rails. The deal, announced this week, includes $300 million in contingent payments and gives Mastercard capabilities the company told investors would have taken years to build internally. (Source: Mastercard press release, March 2026)

What Mastercard actually bought is the stablecoin middleware layer - the orchestration, compliance licensing, conversion tools, and payout rails that connect crypto networks with the SWIFT-age financial system. BVNK holds licenses across multiple geographies, has MiCA-compliant infrastructure, and was already running a Visa Direct stablecoin pilot. It processes remittances, payouts, P2P transfers, and B2B payments. That last part is the tell: this is not a crypto bet, it is a payments infrastructure bet.

The acquisition reveals something uncomfortable for anyone who believed crypto would replace Visa and Mastercard. BVNK had been in takeover talks with both Mastercard and Coinbase. Coinbase was reportedly further along - then walked away. That dual courtship signals something about where the real value sits in the stablecoin economy. Both a crypto-native giant and a 60-year-old card network concluded that the stablecoin middleware layer is too strategically important to leave in someone else's hands. (Source: CryptoSlate analysis, March 2026)

The market numbers back that urgency. Mastercard's own press release said digital currency payment volume reached at least $350 billion in 2025. McKinsey, working with Artemis, estimates actual stablecoin payments at approximately $390 billion annualized. Small relative to the $13.5 trillion total global payment flows McKinsey tracks, but growing fast enough that card networks now treat it as strategic, not experimental.

Visa is running the same playbook. In January, Visa's stablecoin settlement volumes had reached an annualized run rate of $4.5 billion, per Solana ecosystem disclosures. By March, Visa and Stripe-owned Bridge said their stablecoin-linked cards were live in 18 countries and targeting more than 100 by year-end. BVNK was already powering Visa Direct stablecoin pilot programs. Mastercard just decided it was cheaper to buy what Visa was also using than to watch from the outside.

Mastercard also launched a Crypto Partner Program this week alongside the BVNK announcement, listing more than 85 crypto-native firms, payment providers, and financial institutions. The framing: the next phase of on-chain payments runs through collaboration with existing rails, not around them. The message to the broader DeFi ecosystem is blunt. The disruption thesis has been absorbed. The disrupted parties now own the pipes.

"The highest-value layer in the stablecoin economy may be the connective tissue between on-chain and off-chain - not the token itself." - CryptoSlate analysis, March 2026

Mastercard / BVNK Deal Breakdown

FTX's $2.2 Billion Hits March 31 - Bitcoin Watches Carefully

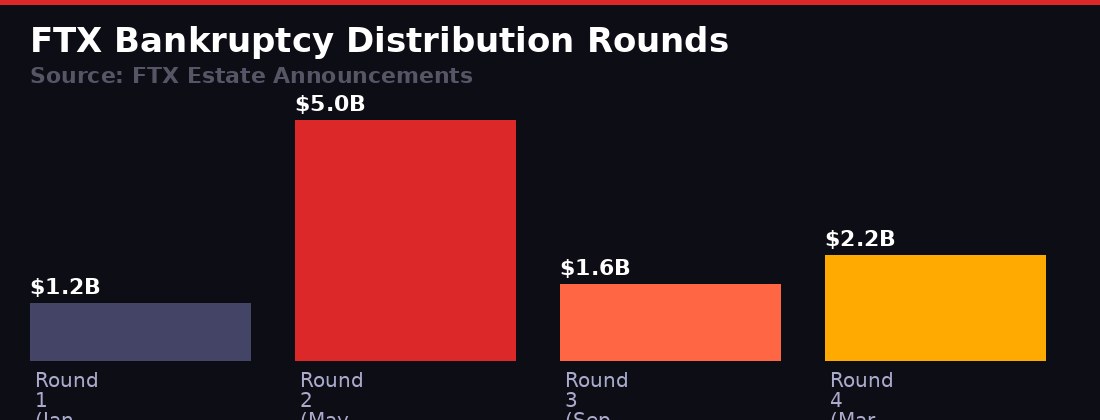

The FTX bankruptcy estate announced on March 18 that its fourth distribution round will begin March 31 and run through April 3. Eligible creditors will receive funds via BitGo, Kraken, or Payoneer within 1 to 3 business days. The total payout: $2.2 billion - the largest FTX distribution since the $5 billion round in May 2025, and 37.5% bigger than September 2025's $1.6 billion third round. (Source: FTX estate announcement, March 18, 2026)

The payout structure breaks down across claim categories. Dotcom customers get an incremental 18%, reaching 96% cumulative recovery. US customers get 5%, reaching 100% cumulative. General unsecured and digital asset loan creditors each get 15%, reaching 100%. Convenience claims stay at 120% cumulative. The people who held crypto on FTX and watched it collapse in November 2022 are now getting made whole in cash - at 2022 dollar values, not at current crypto prices.

That last point matters. FTX creditors are getting their original dollar balances back, not equivalent cryptocurrency at today's prices. If you held 1 BTC on FTX in November 2022 when it was worth $17,000, you are getting $17,000 back - not the current $71,000 equivalent. The crypto community has been vocal about this for years. But that dynamic cuts both ways: creditors receiving cash have no forced obligation to stay in crypto. A portion will recycle into Bitcoin. Another portion will not.

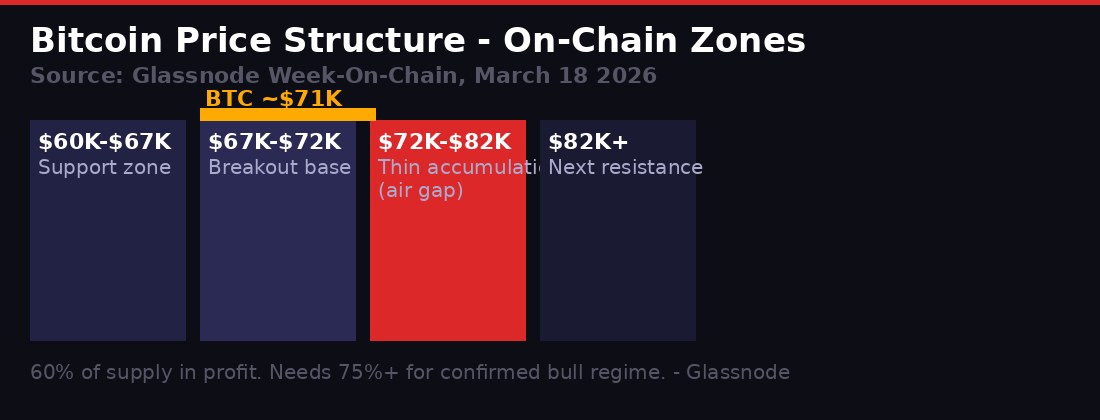

The market structure at the moment of this payout is delicate. Bitcoin is trading at approximately $71,000, having recently broken above the $70,000 threshold and entered what Glassnode's March 18 report calls a "thinly accumulated" zone between $72,000 and $82,000. Limited on-chain resistance in that range means price can move faster - in either direction. (Source: Glassnode Week-On-Chain, Week 11 2026, March 18)

Glassnode says only about 60% of Bitcoin supply is currently in profit. A sustained move above 75% would be needed to confirm a genuine early bull transition. Short-term holders are already realizing profits at $18.4 million per hour as price approached $74,000 this week. ETF flows have rebounded - CoinShares reports $1.06 billion in digital asset inflows last week, with Bitcoin taking $793 million, extending a three-week Bitcoin inflow run to $2.2 billion.

The $2.2 billion figure is not a coincidence. FTX distribution: $2.2 billion. Bitcoin ETF inflows over three weeks: $2.2 billion. The flows are identical in size. The question is whether recycling happens. Researchers model it in percentages:

FTX $2.2B Recycling Model - Bitcoin Impact

Glassnode flags one structural warning: the FTX cash lands after March options expiry. About $4.5 billion in negative dealer gamma sits around $75,000, with $3.9 billion expiring this month. Once quarter-end expiry passes, dealer hedge unwinding creates potential headwinds regardless of creditor recycling behavior. The payout may hit just as a key market support mechanism fades. Timing is not friendly.

SEC Ends Eight Years of War: ETH, SOL, XRP Are Commodities Now

On March 17, the SEC published its biggest crypto classification move in the agency's history. The interpretation places major tokens - Ethereum, Solana, Cardano, Dogecoin, Avalanche, XRP, and Chainlink - into a "digital commodities" bucket. It confirms that some token sales stop being treated as securities-law cases once the issuer's essential promises are fulfilled. Paired with a joint SEC-CFTC memorandum of understanding signed March 11, the release replaces nearly a decade of enforcement-by-litigation with an explicit regulatory taxonomy. (Source: SEC Press Release 2026-30, March 17, 2026)

The SEC's own fact sheet acknowledges what the crypto industry has been screaming for years: the agency spent more than a decade engaging with crypto "mostly through Howey-based analysis" and, before 2025, failed to build a tailored framework, instead "regulating by enforcement." Gary Gensler is gone. This is the formal burial of that era.

The classification taxonomy creates five distinct buckets. Digital commodities - ETH, SOL, and the named tokens - are not themselves securities. Digital collectibles and digital tools also fall outside securities classification. GENIUS Act payment stablecoins fall outside securities status. Tokenized securities - xStocks, tokenized bonds - remain fully inside securities law. Covered staking, mining, and wrapping of non-security assets fall outside the offer-and-sale requirement. Certain airdrops fail Howey's investment-of-money prong entirely and are now explicitly outside securities treatment.

The most structurally important shift is conceptual. The SEC is now saying a token can exit securities status. When the issuer's essential promises are fulfilled - or clearly fail - the investment contract ends, and the token separates. Secondary market trading in that token no longer constitutes a securities transaction. That directly kills the long-running fear that tokens are permanently contaminated by how they were first sold. The legal overhang on exchanges listing "possibly securities" is materially reduced.

"The release explains that when buyers cease to reasonably expect the issuer's essential managerial efforts to remain connected to the asset, the token can separate and exit that contractual relationship." - CryptoSlate analysis of SEC Mar 17 2026 interpretive release

The CFTC joined the release, saying it will administer the Commodity Exchange Act consistently with the SEC's view. The joint SEC-CFTC MOU from March 11 established a "Joint Harmonization Initiative" to align product definitions, reduce friction for dually registered venues, and coordinate policy, exams, and enforcement. They commit to consult on overlapping enforcement matters before issuing a Wells notice. This is the first time the two agencies have formally coordinated on crypto jurisdiction since crypto became a political flashpoint.

The practical implications roll through every major exchange, every institutional crypto fund, and every company that chose to domicile outside the US because of regulatory uncertainty. Legal costs drop. Competitive dynamics shift toward the US. Builders who relocated to Singapore, Dubai, and the Cayman Islands now have a reason to reconsider. None of this happens instantly - existing cases proceed, fraud liability is preserved - but the structural shift is real and permanent.

FDIC Draws the Line: Not All Digital Dollars Are Equal

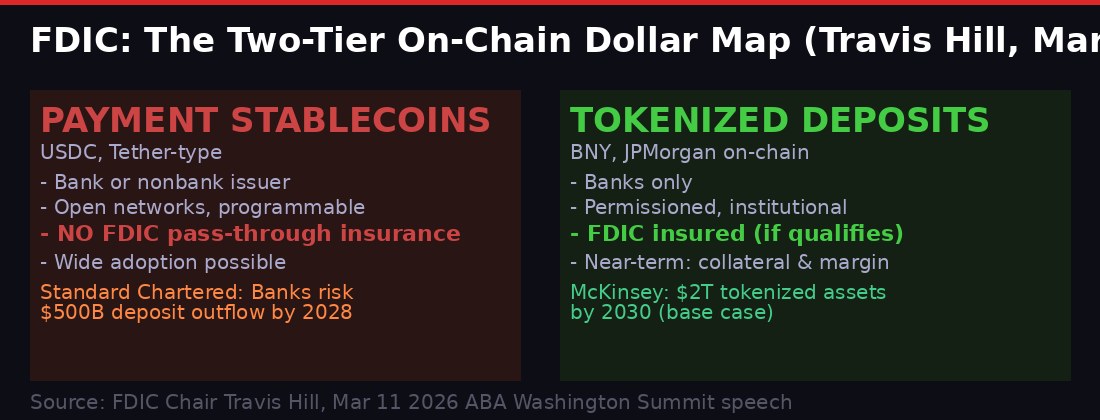

FDIC Chair Travis Hill delivered a speech at the ABA Washington Summit on March 11 that crystallized the regulatory battle underneath the stablecoin legislative fight. The core distinction: payment stablecoins under the GENIUS Act should not qualify for FDIC pass-through deposit insurance. Tokenized deposits that satisfy the statutory definition of a bank deposit would retain the same insurance treatment as traditional accounts. (Source: FDIC Chair Hill speech, March 11, 2026)

That single distinction, if it survives the legislative process, could determine the competitive hierarchy of on-chain money for the next decade. Banks can issue tokenized deposits that carry the FDIC insurance wrapper - the most powerful trust signal in retail finance. Stablecoin issuers like Circle and Tether cannot. Users who want insured digital dollars have to go through banks. The disruption thesis runs directly into a regulatory wall that incumbents built and funded.

The banking industry's anxiety about stablecoins is quantified. A February 2026 New York Fed staff report argued stablecoins can erode bank deposit franchises and transmit liquidity stress into the banking system, forcing partner banks to hold more reserves and reducing lending capacity. Standard Chartered estimated US banks could lose approximately $500 billion in deposits by end of 2028 if stablecoin adoption accelerates. Hill's distinction gives banks a weapon: on-chain money that preserves the deposit insurance advantage that has anchored the financial system since 1933. (Source: Standard Chartered via Reuters, January 2026; NY Fed Staff Report SR1185, February 2026)

The FDIC's positioning feeds into the broader Clarity Act fight in Congress. Banks and crypto firms are currently clashing over whether stablecoins should be allowed to offer yield. If Hill's insurance proposal holds, the fight shifts ground again: it is no longer just about yield, but about fundamental trust infrastructure. The stablecoin battle becomes a question of whether users prefer open, programmable dollars without insurance, or bank-issued tokens that carry the full weight of the existing safety net.

Payment Stablecoins vs Tokenized Deposits - Key Differences

The regulatory thaw for banks is real and coordinated. In March 2025, the FDIC said FDIC-supervised institutions may engage in crypto without prior approval. They withdrew from interagency crypto statements that had called public distributed-ledger activity inconsistent with safe banking. In December 2025, the FDIC proposed an application framework for banks wanting to issue stablecoins through subsidiaries under GENIUS. Then in March 2026, the FDIC, the Fed, and the OCC jointly clarified that tokenized securities receive the same capital treatment as non-tokenized equivalents. Banks got a clear, systematic path back onto blockchain rails. Stablecoin issuers got a hard wall around federal insurance.

Coinbase's Security Own-Goal: Seed Phrases as Official Procedure

In the middle of the most consequential regulatory week in crypto's history, Coinbase managed to generate a security controversy that contradicts years of its own safety guidance. The exchange is directing some Commerce wallet users to a seed-phrase recovery flow ahead of a March 31 migration deadline - the exact behavior that Coinbase's own wallet documentation tells users to reject as a scam.

The mechanics: Coinbase Commerce is shutting down its legacy wallet system. Users with funds in Commerce wallets must withdraw before March 31, when the Commerce portal becomes inaccessible. For users who backed up wallets to Google Drive, Coinbase's transition guide instructs them to open Settings and Security, reveal their 12-word seed phrase, and use the withdrawal tool at withdraw.commerce.coinbase.com. Coinbase says Commerce wallets are self-custodial, so the company cannot access the phrase - users must recover themselves.

The problem is structural, not technical. Coinbase's own wallet help documentation says: never share a recovery phrase, the company will never ask for it, and explicitly warns "never paste it into any website." The Commerce transition guide asks users to do exactly that on an official Coinbase-branded subdomain. Security researchers spotted the contradiction instantly.

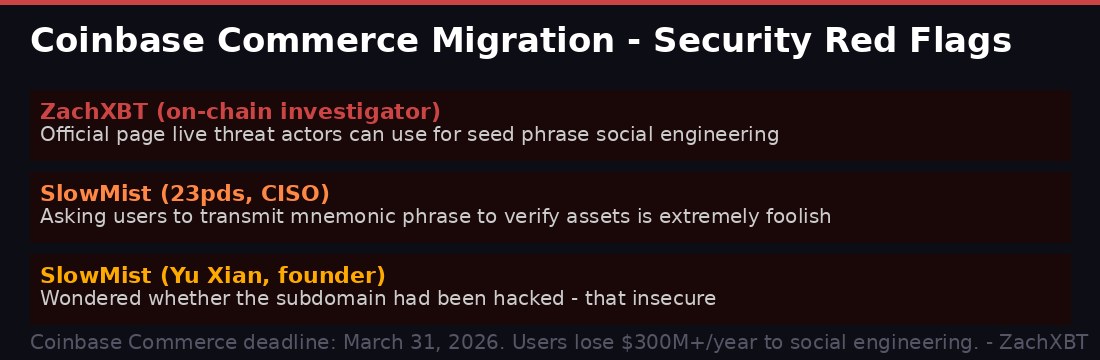

"So basically Coinbase has an official page live threat actors can use to target Coinbase users via seed phrase social engineering if they wanted?" - ZachXBT, blockchain investigator, posted on X, March 2026

SlowMist founder Yu Xian said he was initially puzzled whether the subdomain had been hacked - the practice was that insecure. SlowMist's chief information security officer 23pds identified a second problem: a flawed site sitemap that could allow attackers to clone the front end and deploy a near-identical page on a lookalike domain, creating a highly convincing phishing template using Coinbase's own user flow as the lure. (Source: Yu Xian and 23pds via X, March 2026)

The timing is brutal. ZachXBT revealed in 2025 that Coinbase users lose more than $300 million annually to social engineering scams. In May 2025, Coinbase reported that cybercriminals bribed overseas support agents to steal customer data for social-engineering attacks. The combination of a pending deadline, an official Coinbase domain, and a seed-phrase entry workflow is an attacker's dream template. The March 31 deadline creates urgency. The official Coinbase branding creates trust. The seed-phrase step harvests everything.

Coinbase has not publicly amended the flow at time of writing. Users with Commerce wallets should access the withdrawal tool only by navigating directly to the official URL, enabling maximum URL verification, and treating any inbound communication requesting seed phrase entry - even apparently from Coinbase - as a red flag until proven otherwise.

Metaverse Land: A Post-Mortem in Numbers

New research crystallizes what happened to the $24 million metaverse land boom. A CoinGecko study found that average metaverse land prices were down 72% from their highs by June 2024, with The Sandbox down 95%, Decentraland down 89%, and Otherdeed for Otherside down 85% from peak-cycle average floor levels. The flagship deals of the 2021-2022 era now show losses approaching 100% when marked to current floor-equivalent prices. (Source: CoinGecko Research, Metaverse Land Prices)

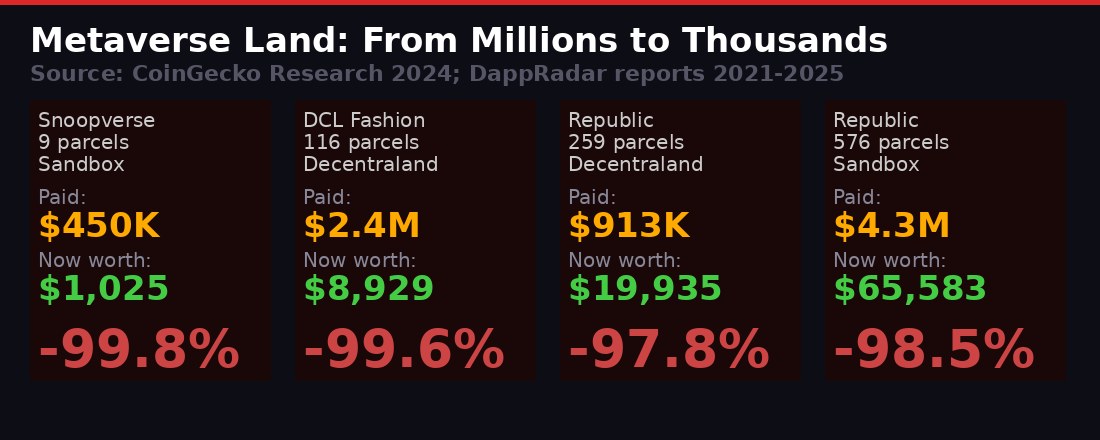

The data is stark. The Snoopverse estate in The Sandbox - nine parcels sold next to Snoop Dogg's virtual property for approximately $450,000 in December 2021 - now screens at approximately $1,025 on a floor-equivalent basis. That is a 99.8% drawdown. Metaverse Group's 116-parcel Decentraland Fashion District estate, purchased for $2.4 million in November 2021, screens at approximately $8,929. Republic Realm's 259-parcel Decentraland purchase for $913,228 screens at approximately $19,935. Republic Realm's 576-parcel Sandbox estate, bought for $4.3 million, screens at approximately $65,583.

Otherdeed #24 - a Bored Ape Yacht Club adjacent plot that sold for 333 ETH (close to $1 million) in May 2022 - has a floor equivalent approaching zero relative to the original purchase price. The Otherdeed floor itself has collapsed so far that even the category's most prestigious assets represent near-total loss scenarios when measured against original premiums paid for celebrity adjacency and scarcity.

The metaverse land unwind is most accurately described as a category repricing, not a temporary correction. Buyers in 2021 and 2022 priced digital land as if virtual neighborhoods would attract real traffic, real commerce, and real scarcity premiums - the same economic logic that governs prime real estate. The market now prices most of it as illiquid optionality: a token representing a claim on a virtual space that may eventually be worth something, but probably much less than originally paid.

NFT trading did not die entirely. DappRadar's Q2 2025 report said NFT volume fell 45% quarter over quarter to $867 million while sales actually rose 78% to 14.9 million transactions. Q3 2025 saw $1.6 billion in volume across 18.1 million sales. The market kept turning, but the pricing model broke. Higher unit activity at much lower dollar values is the signature of a market that has repriced away from scarcity premiums toward commodity consumption. The same number of people trading, for far less money each.

The lesson for the current cycle is applicable beyond virtual land. Any asset class where the bull case requires a critical mass of users to sustain a premium is vulnerable to this repricing dynamic. The Sandbox and Decentraland never got the user traffic their 2021 price tags implied. The same question applies to any token dependent on network effect adoption for its valuation thesis.

Where the Week Leaves Crypto - The Forward View

Five storylines converged this week in a way that does not happen often. The payment giants capitulated, the biggest exchange bankruptcy in history approached its final settlement, the chief US securities regulator reversed course on eight years of enforcement doctrine, the federal deposit insurer drew a hard line between stablecoin and bank money, and the metaverse's price collapse was finally documented in full.

The through-line is institutionalization - but not on crypto's original terms. Mastercard buying BVNK is not crypto winning. It is the legacy financial system absorbing the valuable parts of crypto while retaining structural advantages. The FDIC's insurance distinction is not crypto regulation maturing. It is a deliberate policy choice to ensure banks retain the trust infrastructure advantage over non-bank stablecoin issuers. The SEC's commodity classification is genuinely positive - but it comes with preserved fraud liability, registration requirements for initial sales, and the explicit survival of securities treatment for tokenized stocks.

Bitcoin at $71,000 in a thin on-chain zone with $2.2 billion in FTX cash arriving at the same moment dealer gamma unwinds is a precise setup for volatility in either direction. The market absorbed the first three rounds of FTX payouts without catastrophic price impact. But each round landed in different macro conditions. March 31 arrives into a post-FOMC environment where the Fed held rates and signaled fewer cuts than the market wanted - conditions already producing sell-into-strength behavior at $74,000.

The SEC classification removes a ceiling. Institutions that avoided crypto because of securities law uncertainty have one less reason to stay away. That is a multi-quarter tailwind, not a March catalyst. The Mastercard deal is a data point, not a turning point - stablecoin payment volume at $390 billion annualized is still 0.02% of global payment flows. The FDIC distinction is regulatory positioning that will take years to play out through legislation and court challenges.

What happened this week is the architecture of the next phase being drawn. Banks on-chain with insurance protection. Card networks owning the stablecoin middleware. ETH and SOL formally outside securities law. FTX's victims finally made whole in cash. Metaverse land officially dead as an asset class. The rules just changed - in more ways, and with more permanence, than most market participants have processed yet.

Key Dates Ahead

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSources: Mastercard press release March 2026; FTX estate announcement March 18 2026; SEC Press Release 2026-30 March 17 2026; SEC-CFTC MOU March 11 2026; FDIC Chair Travis Hill speech ABA Washington Summit March 11 2026; Glassnode Week-On-Chain Week 11 2026; CoinShares Digital Asset Fund Flows; NY Fed Staff Report SR1185 February 2026; Standard Chartered via Reuters January 2026; McKinsey tokenized assets report; CoinGecko metaverse land prices research; DappRadar Q2-Q3 2025 industry reports; SlowMist via X March 2026; ZachXBT via X March 2026; CryptoSlate reporting March 2026.