Kraken IPO Frozen, FTX Pays $2.2 Billion, SEC Approves Nasdaq Tokenization: Crypto's Infrastructure Week Explained

Three seismic moves landed in the same 24-hour window: Kraken quietly killed its IPO plans, FTX's recovery trust announced a $2.2 billion creditor payout for March 31, and the SEC formally approved Nasdaq's bid to let securities trade in tokenized form. Read them separately and they look like isolated news items. Read them together and they draw a map of where crypto infrastructure is heading - and how much damage the Iran war has already done to the path there.

BLACKWIRE Markets graphic: Three moves that redefined crypto infrastructure in 24 hours - March 18, 2026.

Kraken Blinks: How a $20 Billion IPO Became "Wait and See"

BLACKWIRE infographic: Kraken's IPO journey from November 2025 filing to March 2026 freeze.

Four months ago, Kraken looked unstoppable. On November 18, 2025, Payward - Kraken's parent company - announced it had raised $800 million in fresh capital, including a $200 million check from Citadel Securities, at a $20 billion valuation. The next day, November 19, it quietly filed a draft S-1 registration statement with the SEC, confirming what the industry had long suspected: Kraken was going public.

The timing felt perfect. Bitcoin had just touched its all-time high of $126,000 in October. Eleven crypto IPOs had collectively raised $14.6 billion in 2025, according to PitchBook data. The SEC under the new administration was friendlier to crypto than at any point in history. The pipeline was wide open.

Then everything broke at once.

Bitcoin gave back roughly 44% from its October peak. The Iran war, which began in late February 2026, sent oil prices screaming from under $60 to nearly $100 per barrel. The Federal Reserve, which was supposed to be cutting rates in 2026, instead held steady at 3.50%-3.75% on March 18 and raised its inflation forecast from 2.4% to 2.7%. Markets got the message: cheap money is not coming.

The most visible sign of the rot came in February, when Kraken dismissed its chief financial officer, Stephanie Lemmerman. Two people with knowledge of the matter confirmed the firing to CoinDesk. A CFO departure four months into a pre-IPO filing process is not a good look. Wall Street equity analysts price that kind of turbulence harshly.

"As we announced in November, we filed confidentially with the SEC, and that is all we can really share." - Kraken spokesperson, March 18, 2026 (via CoinDesk)

That non-answer from Kraken's PR team confirmed what the sources were already saying: the IPO is on ice, probably until Q3 or Q4 2026 at the earliest, and only if conditions meaningfully improve. Two anonymous sources with knowledge of the matter told CoinDesk the company "is still considering an IPO but probably not until market conditions improve."

The tell is in the comparison. Rival exchange Gemini went public in 2025 and has seen its stock price slump to near its 52-week lows. Crypto custodian BitGo, the only pure-play digital asset company to list in 2026, has cratered 44% from its IPO price. These are not exactly the performance charts that attract institutional book runners.

Why Kraken's IPO Matters Beyond Kraken

Kraken filing for IPO was supposed to validate the entire "crypto infrastructure" investment thesis - the idea that picks-and-shovels companies (exchanges, custodians, compliance tech) could command traditional equity market valuations. If the picks-and-shovels trade is dead, so is the argument for a wave of crypto IPOs in 2026. The sector needs Kraken to succeed to prove the model works. An indefinite delay does damage to the entire class.

The contrast with tokenization firm Securitize is instructive. Securitize - which works closely with BlackRock on its tokenized treasury products - told CoinDesk it still plans to go public via SPAC, possibly as early as Q2 2026. CEO Carlos Domingo's reasoning is revealing: "Interest in tokenization continues to be strong in spite of market conditions." Tokenization has a tailwind from institutional money even in a down market. A pure crypto exchange does not enjoy that luxury.

BLACKWIRE infographic: The crypto IPO pipeline - listings, delays, and what comes next.

FTX Pays $2.2 Billion: The Final Chapter No One Expected

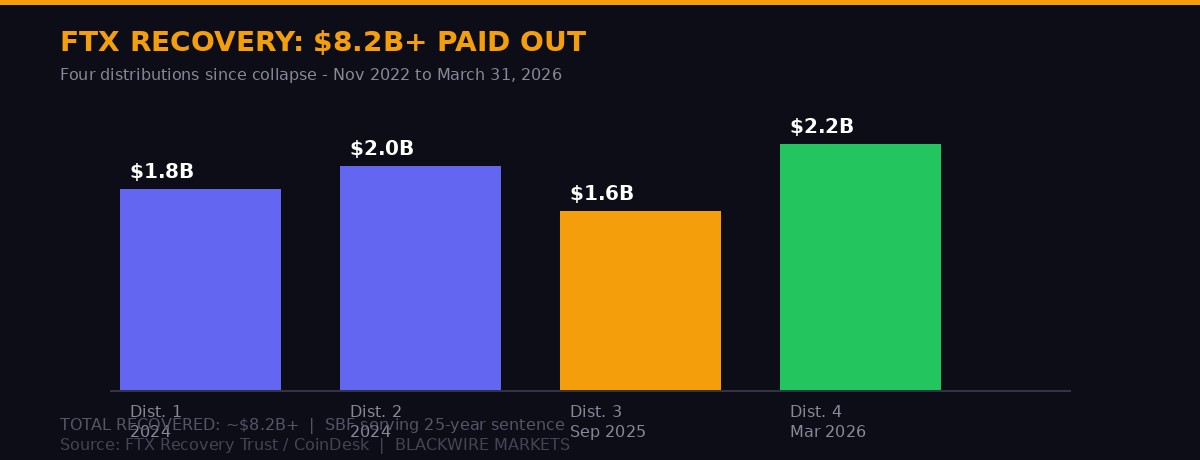

While Kraken is freezing its future, FTX is finishing its past. The FTX Recovery Trust announced on March 18 it will distribute approximately $2.2 billion to creditors on March 31 - the fourth major payout since the exchange collapsed in November 2022.

The announcement comes via a press release filed through PR Newswire by the FTX Recovery Trust. Funds will flow through three distribution partners - BitGo, Kraken, and Payoneer - and recipients can expect to see money within 1 to 3 business days of March 31.

Let that irony land for a second: Kraken, whose IPO is frozen partly because the crypto market is depressed, is one of the three pipes being used to return billions to FTX's burned creditors. The sector is nothing if not circular.

The fourth distribution is significant because of what it means for recovery rates. Here is what creditors in each class are getting:

- Class 5A Dotcom customers: Additional 18% payout, bringing total recovery to 96%

- Class 5B U.S. customers: Reaches 100% total recovery in this round

- Classes 6A and 6B: Full 100% recovery, each receiving a 15% increment

- Class 7: Cumulative 120% distribution - creditors actually get back more than they lost at dollar value

That last point deserves unpacking. Class 7 creditors will receive 120 cents on the dollar. This is because the estate recovered assets at crypto prices that were significantly lower than FTX's collapse-era values, and then the broader market rallied dramatically in 2023-2025. The trust essentially liquidated into a bull market. The beneficiaries are getting more back than they put in, measured in dollars - even though they lost access to their assets for over three years.

"The fourth distribution pushes recovery rates higher across several claim classes." - FTX Recovery Trust statement, March 18, 2026

FTX Recovery: The Numbers

Earlier distributions total more than $6 billion. The September 2025 third distribution alone moved $1.6 billion. Combined with the March 31 payout of $2.2 billion, the trust will have distributed over $8.2 billion since it began returning funds. Sam Bankman-Fried is currently serving a 25-year sentence at a federal penitentiary after being found guilty of seven counts of fraud and conspiracy. The estate he destroyed has outlasted the initial expectations for recovery - and exceeded them by almost every metric.

The trust also set April 30 as the record date for its first-ever payments to preferred equity holders, with actual payments scheduled for May 29. To qualify, equity holders must complete KYC verification, ownership certification, and tax documentation. This is a new class of payment - equity holders, not just creditors - marking the bankruptcy approaching a final resolution.

The FTX collapse in November 2022 wiped out billions in market value and triggered the deepest crypto bear market since 2018. It took down Celsius, BlockFi, and Three Arrows Capital in its wake. It poisoned institutional confidence in crypto custody for over a year. The fact that the estate is now paying back 100% - and in some cases 120% - to creditors is either a remarkable feat of bankruptcy administration, or evidence of just how distorted crypto valuations were in 2022, or both.

BLACKWIRE data chart: FTX Recovery Trust distributions - from first payout in 2024 through the March 31, 2026 $2.2B round.

A critical detail buried in the announcement: FTX customers who elected to receive funds through a designated distribution provider - BitGo, Kraken, or Payoneer - have waived their right to direct cash payments. They must work through those platforms to access their funds. If you are a creditor who has not completed onboarding, your payout is at risk of being delayed. The trust made clear that only creditors who have completed all required steps will receive the March 31 distribution.

The preferred equity payment timeline - April 30 record date, May 29 payment - means FTX's legal saga will stretch into at least mid-2026. Further distribution timelines are expected to be announced after the preferred equity round closes. For all practical purposes, however, the core creditor recovery story is done. The saga that began in a Bahamas apartment in November 2022 is approaching its financial close.

The SEC and Nasdaq Make History: Tokenized Stocks Get Cleared for Launch

BLACKWIRE infographic: The structure of SEC-approved tokenized securities trading on Nasdaq - how it works.

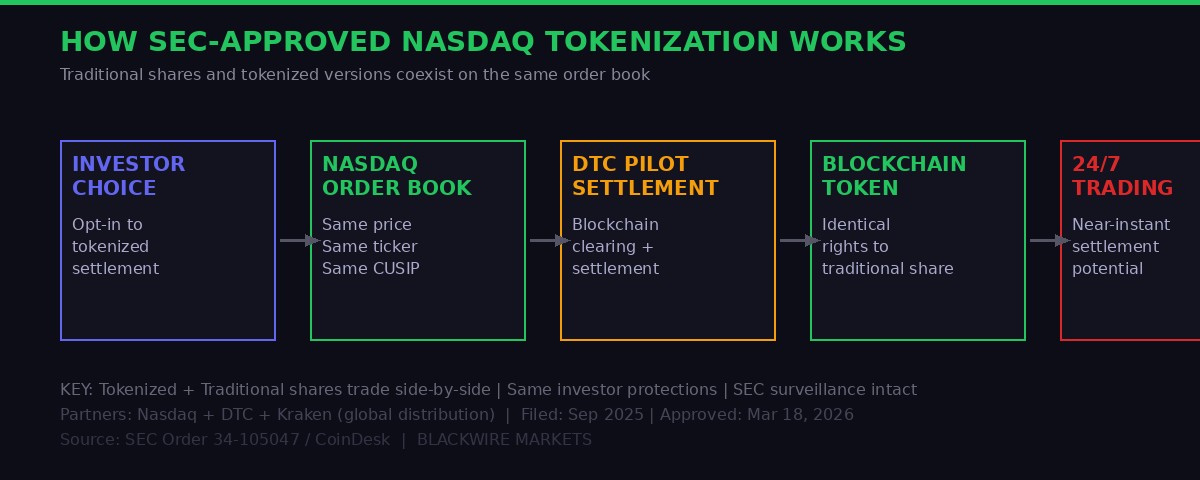

While creditors celebrate and Kraken idles, the SEC quietly signed off on one of the most significant market structure decisions in years. On March 18, the U.S. Securities and Exchange Commission approved Nasdaq's proposal to allow certain securities to trade in tokenized form. The order - SEC release 34-105047 - is live on the SEC's website.

Here is what the approval actually enables. Nasdaq participants can now elect to have their trades settled as blockchain-based tokens rather than through the standard book-entry system currently managed by the Depository Trust Company (DTC). Tokenized shares trade alongside traditional shares on the same order book, at the same price, under the same ticker symbol and CUSIP identification number. Investor protections remain identical: surveillance, data reporting, and settlement timelines all meet existing standards.

This is not crypto. This is traditional equity markets getting a blockchain layer grafted onto existing infrastructure. The distinction matters enormously for institutional adoption. A hedge fund manager who is skeptical of crypto does not care that settlement now runs through a distributed ledger - they care that their trade settles at the same price, under the same rules, with the same compliance protections. Nasdaq's structure delivers that.

"The SEC said the structure meets investor protection standards, noting that surveillance, data reporting and settlement timelines remain intact." - CoinDesk, March 18, 2026, citing SEC Order 34-105047

Nasdaq filed for this regulatory permission back in September 2025. The six-month approval timeline reflects the SEC's methodical approach to reviewing structural market changes, but also signals that the current commission under its pro-innovation leadership is willing to act when the legal framework is sound. This is not a rubber stamp - it required serious due diligence. It is also not a revolution. It is a careful, calibrated experiment.

The market size at stake is staggering. The global equity market has a total capitalization of approximately $126 trillion. Even capturing a fraction of that in tokenized form would represent a multi-trillion dollar shift in how securities infrastructure operates. Settlement that currently takes two business days (T+2) could eventually move toward near-instant finality. Corporate actions, dividend distribution, and shareholder voting could be automated via smart contracts. The back-office cost savings for large institutions run into billions of dollars annually.

Kraken's Dual Role: IPO Frozen, But Nasdaq Partner

There is a notable irony in Kraken's current position. The exchange whose public listing is frozen due to market conditions is simultaneously one of Nasdaq's chosen partners for distributing tokenized stocks globally. Nasdaq said last week it is developing a framework for companies to issue blockchain-based shares and has teamed up specifically with Kraken for global distribution. ICE - the NYSE parent - made a parallel move by investing in crypto exchange OKX with plans for tokenized stocks and crypto futures. Kraken may be too burned out to IPO right now, but it is deeply embedded in what Wall Street is building next.

The DTC pilot that underpins the Nasdaq approval is a critical piece of infrastructure. The DTC currently clears virtually all U.S. equity and corporate bond trades. Getting DTC to run a blockchain settlement pilot is the equivalent of getting the Federal Reserve to test digital dollar rails - it means the core financial plumbing is taking the technology seriously. This is not a startup experiment. This is legacy infrastructure trying to modernize itself.

Intercontinental Exchange (ICE), owner of the New York Stock Exchange, is moving in parallel. ICE invested in crypto exchange OKX with explicit plans to launch tokenized stocks and crypto futures products. Two of the three largest equity exchanges in the United States are now publicly committed to blockchain-based securities infrastructure. The market structure shift is no longer theoretical.

Bitcoin Under $71K: The Context Behind the Three Stories

None of these three developments exist in a vacuum. They are all downstream of the same macro event: Bitcoin sitting below $71,000 on March 18 after the Fed held rates and Jerome Powell flagged the Iran war as a new inflation risk.

Bitcoin's route from its October 2025 peak of $126,000 to sub-$71,000 represents a roughly 44% drawdown. That is not catastrophic by historical crypto standards - the 2022 bear market took BTC from $69,000 to $15,500, a 78% decline. But it is large enough to materially alter corporate decision-making, IPO valuations, and institutional risk appetite.

The Federal Reserve's March 18 decision to hold the fed funds rate at 3.50%-3.75% was universally expected. What was not universally priced in was the language in the accompanying statement. The Fed acknowledged that "the implications of developments in the Middle East for the U.S. economy are uncertain" - central bank speak for "the Iran war is a real risk and we don't know how bad it gets." The vote was 11-1, with Federal Reserve Governor Stephen Miran dissenting in favor of a 25-basis-point cut.

Powell's post-meeting press conference added fuel to the fire. He acknowledged that rising oil prices "for sure show up" in policymakers' higher inflation projections - the 2026 inflation forecast moved from 2.4% to 2.7%. He pushed back on stagflation comparisons, saying "I would reserve the term stagflation for a much more serious set of circumstances," but the fact that reporters are asking the question says something about how the market is pricing risk right now.

BLACKWIRE SIGNAL: The dot plot still shows one 25-basis-point cut in 2026 and one more in 2027. But "one cut in 2026" in March looks very different from "one cut in 2026" in October 2025, when the market was pricing in three to four cuts. Rate cut hopes have not evaporated - they have collapsed from bull-market fantasy to single-event reality. For risk assets including Bitcoin, that is a meaningful shift in the liquidity environment.

The hash rate data makes the crypto-specific pain more concrete. Bitcoin's network hash rate dropped roughly 8% in the week ending March 18, falling to 920 EH/s, according to mempool.space data. An estimated 8% to 10% of global Bitcoin mining operates in energy markets sensitive to the oil price surge caused by the Iran conflict. With hash rate falling, the network is heading for an approximately 8% downward difficulty adjustment - one of the second-largest negative shifts in five years.

Miners under margin pressure sell BTC to cover operating costs. That selling pressure is a headwind on Bitcoin prices regardless of any macro narrative. The hash rate drop, the energy price surge, and the Fed's hawkish hold form a triangle of pain squeezing Bitcoin from three directions simultaneously.

The Fairshake $10 Million Misfire: Crypto's Political Bet Goes Wrong

One more story from the same 24-hour window deserves attention: the Fairshake PAC's $10 million loss in the Illinois Senate primary.

Fairshake is the crypto industry's primary political action committee. It raised more than $170 million in the 2024 election cycle and established itself as one of the largest independent expenditure groups in U.S. political history. Its strategy has been to back pro-crypto candidates and punish anti-crypto incumbents.

In the Illinois Senate Democratic primary, Fairshake spent more than $10 million - over 5% of its estimated total war chest - trying to defeat a candidate who ultimately won the primary. The candidate the PAC backed lost. The candidate the PAC opposed won.

This is the first major electoral misfire for crypto's political machine. One loss does not break the strategy - Fairshake backed more than 50 candidates in 2024 and won the vast majority. But it reveals that the PAC's ability to move primary results is not unlimited. There are constraints: local politics, brand, candidate quality, issue salience. In Illinois, the crypto issue did not move enough voters to overcome other factors.

CoinDesk called the result "the first big hitch in crypto's political surge." That is an accurate read. For an industry that has spent $170 million+ buying political influence, one $10 million loss is a rounding error. For the specific argument that crypto PAC money is politically decisive, Illinois is a warning shot.

"Fairshake's $10 million Illinois misfire marks the first big hitch in crypto's political surge." - CoinDesk, March 18, 2026

The Bigger Picture: Crypto Infrastructure at an Inflection Point

BLACKWIRE: Three moves, one inflection. How March 18, 2026 rewrote the map for crypto's next phase.

Stack all five stories from March 18 into a single frame and a pattern emerges. Crypto is not dying - it is bifurcating. The speculative, price-driven, retail-facing end of the market is getting crushed by macro headwinds: the Iran war, sticky inflation, a Fed that cannot cut, and a Bitcoin hash rate in free fall. The infrastructure-facing, institutional-grade end is advancing regardless.

Kraken freezing its IPO is a price story. The company is worth less right now than it was when it filed the S-1. Waiting for better market conditions is not weakness - it is the only rational move when comparable names are trading down 44%. No competent banker would advise launching into this window.

FTX paying back $2.2 billion is a cleanup story - and a remarkable one. The fact that creditors are recovering 100% to 120% of their claims is a function of extraordinary legal work by the recovery trust under CEO John Ray, plus the structural irony that the bear market of 2022-2023 allowed the estate to buy back assets cheaply before Bitcoin surged to $126,000. The system worked, but only because the system got very lucky on timing.

The Nasdaq tokenization approval is a structural story. The SEC's sign-off on blockchain-based equity settlement is not going to move Bitcoin's price today or tomorrow. What it does is establish a legal and technical framework for the next decade of market infrastructure. Once the DTC pilot proves the settlement mechanics work at scale, the pressure on every major exchange to offer tokenized versions of their securities will be immense. This is the beginning of a multi-year migration.

The $126 trillion global equity market is not moving to blockchain next week. But it started moving to blockchain on March 18, 2026. The SEC's signature on Order 34-105047 is the timestamp.

Put it all together: crypto's speculative layer is bleeding out in a wartime macro environment. Crypto's infrastructure layer is getting embedded into the deepest plumbing of global financial markets. Those two things can be simultaneously true. They are both true right now.

For traders watching Bitcoin oscillate below $71,000 and wondering if the bull market is over, the answer is: it depends which part of the market you are talking about. The price chart says one thing. The regulatory filings say another. Both matter. The next 12 months will determine which narrative wins.

What Happens Next: Three Timelines to Watch

FTX $2.2B Distribution: Creditors in Convenience and Non-Convenience classes receive payout via BitGo, Kraken, and Payoneer. 1-3 business day settlement. Class 5B U.S. customers hit 100% recovery. Class 7 hits 120%.

FTX Equity Payout: Record date set for April 30; preferred equity holders who complete KYC and tax documentation receive first-ever equity payments on May 29. First-ever payment to equity class marks near-final chapter of the bankruptcy.

Securitize SPAC IPO: Tokenization firm backed by BlackRock plans to go public as soon as SEC grants green light, likely Q2. Has already raised $225M via PIPE. CEO Carlos Domingo: "Interest in tokenization continues to be strong."

Kraken IPO (Possible): Company is still considering a public listing but only when market conditions improve. Needs Bitcoin to recover, equities to stabilize, and a new CFO narrative after Lemmerman's departure. Timeline is entirely market-dependent.

Nasdaq Tokenization Pilot: The DTC pilot is now live following SEC approval. Early participants electing tokenized settlement will provide the first real-world data on whether blockchain-based equity settlement performs at scale. Results will shape every major exchange's roadmap for the next decade.

Sources

- CoinDesk: Kraken freezes IPO plans (March 17-18, 2026) [Primary reporting]

- CoinDesk: FTX Recovery Trust $2.2 billion distribution (March 18, 2026)

- PR Newswire: FTX Recovery Trust official press release

- CoinDesk: SEC approves Nasdaq tokenized securities (March 18, 2026)

- SEC Order 34-105047: Nasdaq tokenized securities rule filing

- CoinDesk: Bitcoin sinks below $71,000 post-Fed (March 18, 2026)

- CoinDesk: Fed holds rates, March 18, 2026

- Federal Reserve: FOMC statement, March 18, 2026

- Federal Reserve: Updated economic projections (dot plot), March 18, 2026

- CoinDesk: Bitcoin hash rate falls 8%, March 18, 2026

- CoinDesk: The era of cheap money is over, March 18, 2026

- CoinDesk: Fairshake $10M Illinois misfire, March 18, 2026

- mempool.space: Bitcoin network hash rate and difficulty adjustment data

- PitchBook: Crypto IPO data 2024-2026

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram