The clash between states and federal regulators over prediction markets has taken a criminal turn. (Pexels)

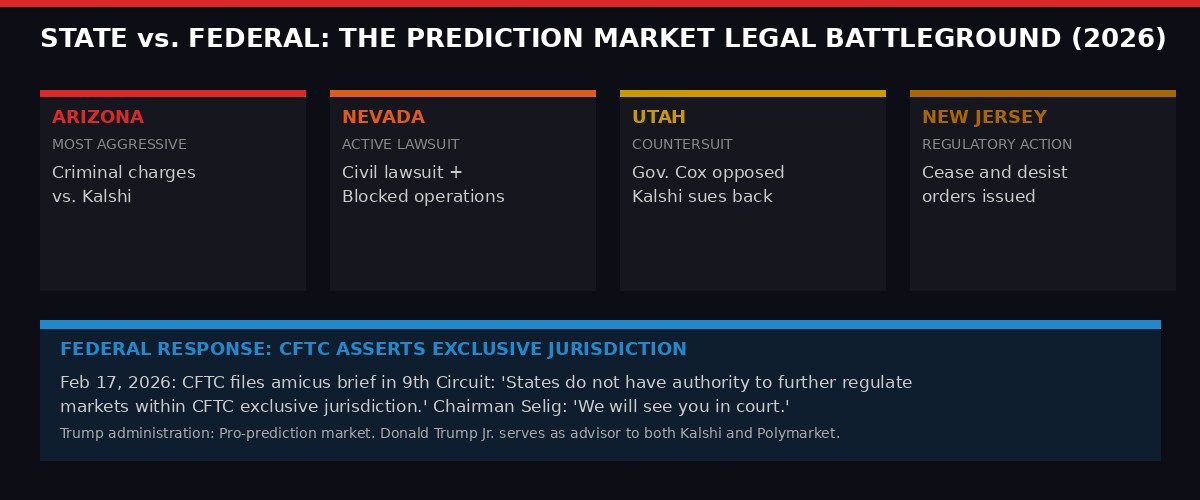

Arizona filed criminal charges against Kalshi on March 17, 2026 - the first-ever criminal case against a prediction market company in United States history. The Arizona attorney general's office accused Kalshi of illegally operating a gambling business in the state, a charge the company flatly denies and calls an unconstitutional overreach by a state trying to claim regulatory power it doesn't have.

Kalshi responded with its now-familiar posture: defiance. The company told Reuters that "states like Arizona want to individually regulate a nationwide financial exchange, and are trying every trick in the book to do it." They didn't back down from operating. They didn't promise compliance talks. They essentially dared Arizona to follow through.

This is what the prediction market war looks like in March 2026 - not a policy debate in committee rooms, but a full-contact legal battle being fought simultaneously on four fronts: Nevada's civil suit, Utah's regulatory standoff, the CFTC asserting federal supremacy in the 9th Circuit, and now Arizona reaching for criminal prosecution. The stakes are enormous. Prediction markets processed over $1 billion in volume on a single Super Bowl Sunday. March Madness could shatter that record. And the question of who controls this industry - and who taxes it - is worth billions of dollars a year in revenue.

The Legal Architecture That Made This Fight Inevitable

To understand why Arizona is bringing criminal charges, you need to understand the legal architecture prediction markets built their business on - and why states consider it a loophole rather than a legitimate distinction.

Prediction markets operate as Designated Contract Markets (DCMs) under the Commodity Futures Trading Commission. That designation means they are, legally speaking, financial exchanges - not gambling companies. When you place a bet on whether the Kansas City Chiefs will win the Super Bowl on Kalshi, you are technically trading a binary event contract, not wagering on a sports outcome. The difference is not semantic to regulators; it's structural. The CFTC, which was established to regulate futures and derivatives, has federal jurisdiction. Gambling laws belong to the states. Since the CFTC claims prediction markets, states theoretically cannot touch them.

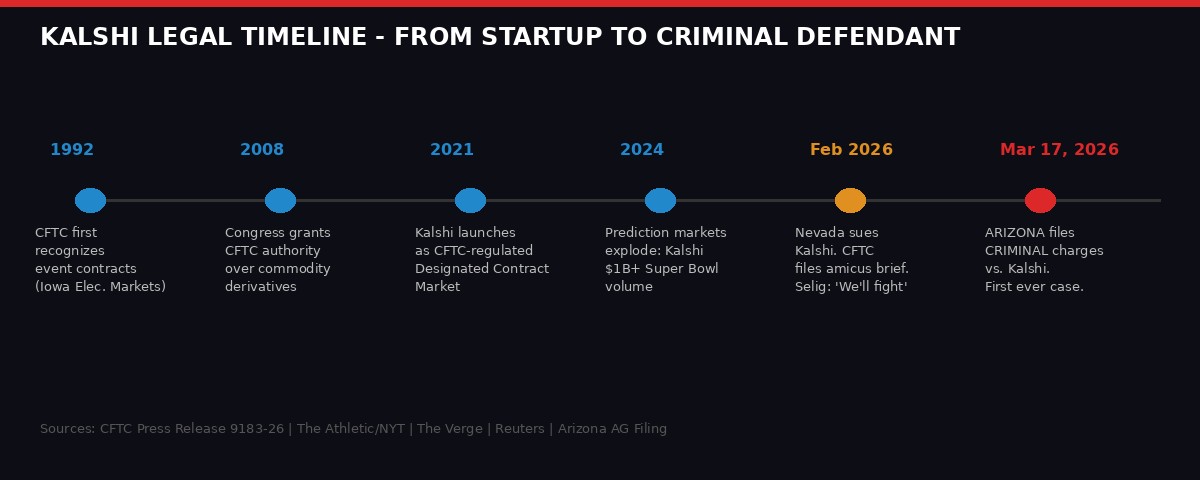

This framework was built over decades. The CFTC first officially recognized event contracts in 1992, when it allowed the Iowa Electronic Markets - a research project at the University of Iowa - to run futures markets on presidential election outcomes. Congress expanded the CFTC's authority over commodity derivatives in the wake of the 2008 financial crisis, writing laws broad enough to cover emerging financial instruments.

Prediction markets were almost a perfect fit. They structured themselves accordingly, registered with the CFTC, and built their legal moat. For years, it mostly worked. The Biden administration banned Polymarket from operating in the US, but that was an application of CFTC authority, not state law. When the Trump administration took over in early 2025, it reversed course - both Kalshi and Polymarket reopened to US users under CFTC oversight. The industry boomed.

Then the states got angry.

The legal battleground as of March 2026. Arizona's criminal move is the most aggressive state action yet against the industry. (BLACKWIRE graphic)

Why States Are Fighting - and What They Actually Want

Prediction markets have a structural problem when it comes to state regulators: the money flows in and the states see nothing. Traditional sportsbooks pay licensing fees, excise taxes, and channel a portion of gambling revenue to state funds. In New Jersey, for instance, legal sports betting generates hundreds of millions in annual tax revenue. Prediction markets, regulated federally as financial exchanges, pay no such state taxes.

Nevada's position is almost nakedly economic. The state built an entire economy around gambling. Las Vegas is the world's best-known gambling destination. The Nevada Gaming Control Board collects licensing fees, tax revenue, and compliance fines from regulated casinos and sportsbooks. When Kalshi processes $1 billion on the Super Bowl - money wagered mostly on sports outcomes - and remits nothing to Nevada's coffers, that's not just a regulatory disagreement. That's a direct attack on Nevada's business model.

Democratic congresswoman Dina Titus from Nevada made it plain: prediction markets "should not be able to circumvent state gaming laws," she said in early 2026. Nevada filed a civil suit to block Kalshi from operating in the state, which the company fought with a federal injunction. The CFTC filed an amicus brief in that case - formally titled North American Derivatives Exchange, Inc. et al v. The State of Nevada - on February 17, 2026, asserting its exclusive jurisdiction.

Utah's opposition is ideological rather than economic. Utah has no legal sports betting - the state considers gambling morally harmful. When CFTC Chairman Michael Selig publicly defended prediction markets, Utah Governor Spencer Cox responded viscerally. "These prediction markets are gambling - pure and simple," Cox said. "They are destroying the lives of families and countless Americans, especially young men." Kalshi responded by suing Cox directly, seeking an injunction blocking Utah from interfering with its business. A strategy it has deployed successfully in other states.

"CFTC-registered exchanges have faced an onslaught of lawsuits seeking to limit Americans' access to event contracts and undermine the CFTC's sole regulatory jurisdiction over prediction markets. This power grab ignores the law and decades of precedent." - CFTC Chairman Michael S. Selig, February 17, 2026 (CFTC Press Release 9183-26)

Arizona now takes a third path: criminal prosecution. The Arizona attorney general's criminal filing frames Kalshi as an illegal gambling operator - full stop. The charges don't ask for licensing. They don't seek a regulatory framework. They treat prediction market operation as a criminal act under Arizona law, with the potential for criminal penalties rather than civil fines or injunctions.

What the CFTC's Amicus Brief Actually Says

The federal government's position has been unusually clear for a regulatory agency. The CFTC's February 17 amicus brief in the 9th Circuit is worth reading directly, because it sets the stage for how the Arizona criminal case will likely be contested.

The brief argues that states "do not have the authority to further regulate markets within the CFTC's exclusive jurisdiction, and attempting to do so would have destabilizing economic effects." It traces the CFTC's regulatory history back to the Commodity Exchange Act and the 1974 legislation that created the commission, arguing that Congress intended federal preemption of state interference in derivatives markets.

The CFTC also makes an affirmative case for prediction markets as a social good - noting that "event contracts allow businesses and individuals to hedge event-driven risks, enable investors to manage portfolio exposure, and provide the public with information about the outcome of future events." This language is deliberate: it frames sports betting on the Eagles -2.5 as equivalent to a farmer hedging against bad weather futures. The legal argument is that both are commodity derivatives and both fall under federal jurisdiction.

Selig's public statement was even blunter: "To those who seek to challenge our authority in this space, let me be clear: We will see you in court."

But the CFTC's amicus brief is civil. Arizona's charges are criminal. That distinction matters enormously in practice. Federal preemption arguments typically operate in civil courts. Criminal prosecutions by state attorneys general against companies they claim violated state law create a different kind of pressure - one that cannot be easily resolved by federal injunction before the reputational damage is done, before executives face arrest warrants, before investors get nervous.

From the CFTC's 1992 recognition of event contracts to Arizona's 2026 criminal filing - thirty years of regulatory infrastructure potentially unraveling. (BLACKWIRE graphic)

The Trump Factor: How Politics Scrambled the Regulatory Map

The prediction market industry's current crisis is inseparable from the Trump administration's return to power - but not in the way you might expect. The Trump administration is broadly pro-prediction market. Donald Trump Jr. serves as an advisor on the boards of both Kalshi and Polymarket. The CFTC under Chairman Selig has been aggressively supportive. The administration's regulatory posture should, in theory, create a favorable federal shield for the industry.

Instead, it created a political paradox that made state action more likely. The sudden surge in prediction market activity after January 2025 - Kalshi's 27x year-over-year growth on the Super Bowl, Polymarket's return to US markets, the flood of new entrants from DraftKings, FanDuel, Robinhood, and Coinbase - caught state regulators flat-footed. The growth happened faster than their ability to respond through normal legislative channels.

And because the Trump administration's pro-market stance was so explicit, states that opposed prediction markets couldn't appeal to federal discretion. They couldn't lobby the CFTC to back off. They had to fight in court or, as Arizona is now doing, in criminal proceedings.

The political geography here is also unusual. Nevada's opposition is Democratic-led; it's about tax revenue and protecting an existing industry. Utah and Arizona's opposition has been more Republican-led, framed in moral terms about gambling addiction. This cross-partisan state resistance is actually a feature, not a bug - it means the industry faces opposition that doesn't break cleanly along the Trump-vs-Democrats fault line that normally protects its federal allies.

Nathan Goldman, an accounting professor at North Carolina State University whose research focuses on corporate taxation, told The Athletic that the core problem is regulatory vintage. "One of the problems that we have is that the gambling rules, especially for sports betting, are so outdated and archaic," Goldman said. "They were established before there was really legalized gambling anywhere except for, like, Vegas and Atlantic City. The rules were established before we had smartphones, before we had online sports gambling."

Asaf Meir, founder and CEO of financial surveillance company Solidus Labs, drew the obvious parallel: "We've been in this movie before, where there is an asset class that is moving faster than regulation. It's one-for-one crypto and digital assets."

The Gambling vs. Finance Distinction: Is It Actually Coherent?

The legal architecture that prediction markets rest on is technically valid. The CFTC's jurisdiction is real. The regulatory history is real. But there's a genuine philosophical problem buried in the middle of the argument that state attorneys general are now exploiting.

From the consumer's perspective, the functional experience of using Kalshi to bet on March Madness is almost indistinguishable from using DraftKings. You pick a team, you put money on the outcome, you either win or lose. The contractual mechanism underneath - binary event contracts vs. sports wagers - is invisible to users. The companies have structured things differently to get regulatory treatment, but the user-facing product is betting.

On Kalshi, sports contracts make up approximately 90% of total trading volume, according to reporting from The Athletic/New York Times. The other 10% covers politics, economics, and other events. The company's primary business, measured by activity, is sports betting - just structured as commodity futures.

The tax treatment reveals the strangeness of the current arrangement. Sports bets are taxed as gambling income. Prediction market contracts are taxed as futures - a hybrid of short-term and long-term capital gains that generally results in lower tax rates than gambling winnings. Goldman describes the absurdity directly: the favorable futures tax treatment "was written for like oil futures and weather predictions where they have to help have some checks and balances if the farmers have a bad winter or something. Now, we have people betting on the Eagles -2.5 with it."

This is the strongest argument Arizona and other states have - not that the CFTC lacks jurisdiction, but that the regulatory arbitrage prediction markets exploit was never intended to cover mass-market sports betting products. The legal framework was designed for sophisticated financial instruments. It's being used to run what looks, from most angles, like an online sportsbook.

Civil injunctions and regulatory disagreements can be managed. Criminal charges create immediate pressure on executives, board members, and investors. Even if Kalshi ultimately wins the legal argument - which it probably will, given the CFTC's strong position - the reputational and operational cost of fighting criminal charges in a state while simultaneously running a consumer-facing platform is substantial. It's not just about Arizona. It's about what other state AGs decide to do when they see that criminal prosecution is now on the table.

March Madness and the Billion-Dollar Pressure Test

The timing of Arizona's filing is not accidental. March Madness - the NCAA basketball tournament - is the prediction market industry's single biggest annual event. The tournament runs from mid-March through early April, with 67 games, tens of millions of casual participants, and historically the highest betting volume of any US sporting event outside the Super Bowl. For 2026, with prediction markets now mainstream and accessible through platforms like Coinbase and Robinhood, the potential volume is unprecedented.

Industry observers have predicted March 2026 could easily be the biggest month in prediction market history. Kalshi's leadership likely anticipated a record period. Instead, they're entering it as the defendant in a criminal case filed by one of the five most populous states in the country.

The operational implications are real but manageable in the short term. Kalshi can continue operating everywhere except potentially within Arizona itself while the legal process plays out. Federal court injunctions have been Kalshi's weapon of choice against state interference, and the company's legal team has already demonstrated competence at obtaining them quickly - its filing against Utah's governor moved within days of Cox's public opposition.

But the reputational pressure compounds with every new state that joins the fight. What started as Nevada's civil suit in February has become a multi-front legal war in just thirty days. Arizona's criminal charges are qualitatively different from what came before. Other state attorneys general are watching. The question isn't whether Arizona will succeed - the CFTC's position gives Kalshi strong federal preemption arguments. The question is whether the patchwork of state resistance becomes expensive enough to force a congressional solution.

The Endgame: Federal Legislation or Legal Exhaustion?

There are two plausible scenarios for how this ends. The first is legal exhaustion - Kalshi and its peers win case after case in federal courts, the states run out of money and political will to keep filing, and prediction markets establish their federal supremacy through accumulated precedent. The CFTC's 9th Circuit amicus brief looks like the foundation for exactly this strategy.

The second scenario is congressional intervention. The state opposition, despite being cross-partisan and politically diverse, is creating enough noise that legislators start feeling pressure to clarify the law. A framework that explicitly defines prediction markets as financial exchanges and establishes federal preemption in statute would put the issue to rest. So would the opposite: a law clarifying that event contracts with primarily recreational, sports-focused use cases are gambling, not commodity derivatives, and subject to state gaming laws.

Prediction market companies, naturally, prefer the status quo - or a clarifying statute that locks in federal authority. The gambling industry, led by DraftKings and FanDuel (which now have both sports betting licenses and prediction market products), occupies an awkward middle ground. These companies pay state taxes through their licensed sportsbooks while simultaneously using their prediction market products to avoid those same taxes. They have limited appetite to push for a resolution that might cost them their own arbitrage.

The Trump administration's political calculus is similarly complicated. The president's son is on Kalshi's board. The CFTC chairman is a public advocate for prediction markets. But Republican governors in Utah and Arizona are filing the most aggressive opposition. The White House cannot simply declare victory for prediction markets without losing allies in red states where social conservatives consider online gambling an existential moral threat.

The crypto angle deserves attention. Several major prediction market platforms - Polymarket, Manifold, and others - operate primarily through blockchain infrastructure rather than CFTC-regulated exchanges. Polymarket's return to the US market under the Trump administration was structured around its crypto-native architecture. If Arizona's criminal theory that prediction markets are gambling regardless of their regulatory classification succeeds, it creates a precedent that could be applied to decentralized prediction markets that lack even the CFTC's protective designation.

What Comes Next

Watch for three things in the coming weeks. First, whether other state attorneys general - particularly in states like Texas, Oklahoma, or Mississippi, where social conservatism meets the absence of legal sports betting - follow Arizona's lead with criminal filings of their own. The Arizona action creates political cover for copycat prosecutions.

Second, watch the 9th Circuit case. The CFTC's amicus brief in North American Derivatives Exchange v. Nevada is the legal linchpin. A ruling favorable to the CFTC's jurisdiction claim would significantly defang state civil suits - though it's less clear whether it would block criminal prosecutions, which operate on a different legal basis.

Third, watch Congress. Legislation is unlikely in the near term, but the prediction market industry has been building lobbying infrastructure in Washington. A congressional clarification - even a narrow one - would be worth hundreds of millions in regulatory certainty to companies that currently face a different legal landscape in every state where they operate.

Kalshi's statement after the Arizona filing was defiant, but the defiance has a specific target: it called out states trying to "individually regulate a nationwide financial exchange." That framing is legally accurate and strategically smart - it casts Arizona as a parochial actor trying to override federal law. But it doesn't resolve the fundamental tension the company faces: they are federally regulated as a financial exchange, but their primary business is sports betting, and no amount of legal architecture changes what users are actually doing when they log in on a Saturday.

The prediction market industry built its legal house on the argument that form matters more than substance. Arizona just said: prove it in criminal court.

Sources: The Verge (March 17, 2026); CFTC Press Release 9183-26 (February 17, 2026); The Athletic/New York Times, March 9, 2026; Salt Lake Tribune (February 25, 2026); Reuters (February 18, 2026). Arizona AG filing available via Reuters/Thomson Reuters legal document archive.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram