17% of World Natural Gas Supply Offline for Five Years: The Crisis No One Is Ready For

QatarEnergy's CEO has confirmed it in cold numbers: Iranian missile strikes on Ras Laffan have taken 17 percent of the company's LNG export capacity offline for three to five years. Combined with the closure of the Strait of Hormuz, the damage to South Pars, and the cascading strikes across the Gulf, the global natural gas market is now facing a structural supply hole of historic proportions - not a temporary disruption, but a multi-year deficit baked into the infrastructure calculus of every country on earth that burns gas to keep the lights on.

Energy infrastructure burning - the new reality across the Gulf. (Illustrative)

This is not a commodity shock. It is not a pricing event. It is a permanent, years-long removal of supply from a market that was already running at near-capacity. The damage done to Ras Laffan Industrial City in the early hours of March 19, 2026, will not be repaired by next winter. It will not be repaired by 2028. The engineers have not yet walked the site to assess the full damage - but QatarEnergy's CEO Saad al-Kaabi has already told Reuters the numbers, and they are as bad as anything this market has seen in living memory.

The 1970s oil crisis took months to develop and was resolved by political negotiation. This is different. Steel and concrete are destroyed. The world's largest LNG export facility has taken direct hits from Iranian ballistic missiles. And the war that caused this is still actively underway, with no ceasefire in sight, and the IRGC still threatening every other energy facility in the region.

What Was Hit, and How Bad

LNG processing infrastructure of the type now destroyed at Ras Laffan. (Illustrative)

Ras Laffan Industrial City is not just any industrial zone. It is the single most concentrated node of LNG production capacity on the planet. Located 80 kilometres north of Doha, it hosts Qatar's entire LNG operation - 14 liquefaction trains drawing from the North Field (Qatar's side of the South Pars/North Dome gas reservoir), plus gas-to-liquids plants, petrochemical facilities, and the world's largest artificial harbour, through which the world's largest LNG tankers load and depart.

According to QatarEnergy's official statement and al-Kaabi's Thursday interview with Reuters (Al Jazeera, March 19, 2026), Iran's retaliatory strikes - launched after Israel bombed South Pars on March 18 - hit:

- Two of Qatar's 14 LNG liquefaction trains - the industrial equipment that converts natural gas into liquid form for export

- One of Qatar's two gas-to-liquids facilities - the Pearl GTL or Oryx GTL plant

- Storage tanks, gas installations, and transmission pipelines throughout the Ras Laffan complex

The result: 12.8 million tonnes of LNG production capacity per year is offline. The facilities will take three to five years to repair. Al-Kaabi told Reuters the damaged units cost approximately $26 billion to build. He said the scale of the damage has set the region back "10 to 20 years."

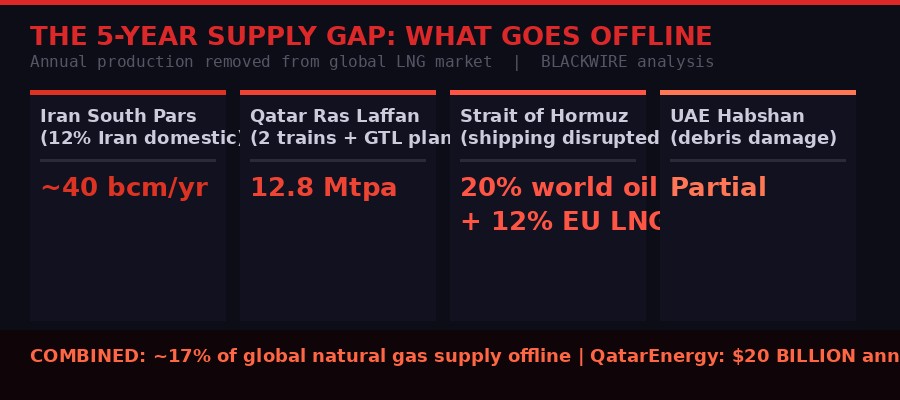

What has been removed from the global gas market - Iran domestic capacity, Qatar LNG trains, and Hormuz transit. (BLACKWIRE infographic / QatarEnergy / IEA data)

On the Iranian side, the South Pars field - Iran's name for its portion of the shared reservoir - took Israeli airstrikes on March 18. Initial damage assessments reported by Al Jazeera and Iranian state media indicated that the attack halted output at two refineries with a combined capacity of 100 million cubic meters per day, and that the damage represents approximately 12 percent of Iran's total domestic gas production (Wikipedia, 2026 South Pars field attack). That number matters less for global markets - Iran consumes most of its South Pars gas domestically - but it matters enormously for Iraq, which relied on Iranian gas exports for between a third and 40 percent of its electricity generation. Iran immediately halted those exports on March 18.

The Mathematics of the Supply Hole

Pipeline infrastructure. When supply removes itself from the market, pipelines go cold. (Illustrative)

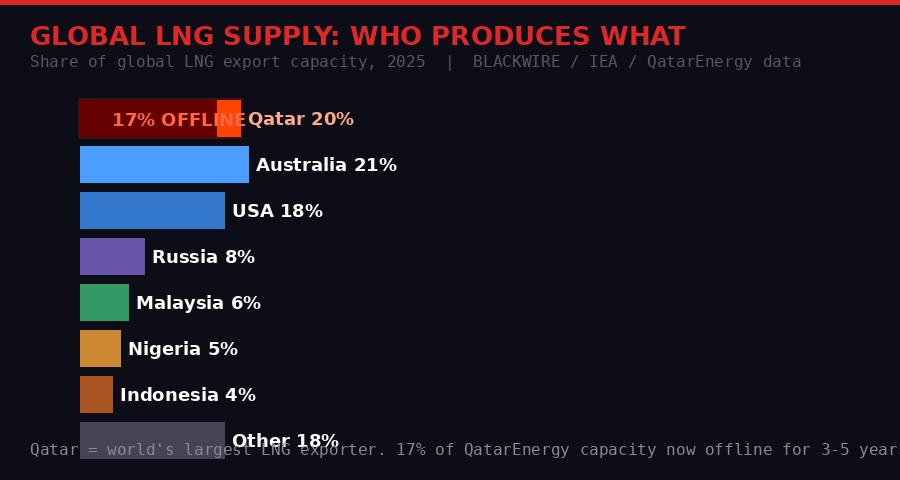

Qatar is, by a significant margin, the world's largest LNG exporter. The company does not merely sell gas - it is the backbone of global LNG trade. Ras Laffan produces approximately 20 percent of the world's total LNG supply, according to Al Jazeera and QatarEnergy's own reporting. When al-Kaabi confirms 17 percent of QatarEnergy's capacity is gone, that figure translates to roughly 3.4 percent of total global LNG supply from Ras Laffan damage alone.

But the headline "17% of global natural gas supply offline" requires understanding three separate, simultaneous disruptions that have compounded in less than three weeks:

Global LNG supply market share by producer - Qatar's dominant 20% position and the 17% offline portion. (BLACKWIRE infographic / IEA data 2025)

First: The Strait of Hormuz. Since the war began on February 28, Iran's IRGC has effectively closed the strait to commercial shipping. As of March 12, 21 confirmed attacks on merchant vessels had reduced tanker traffic to near zero. Approximately 20 percent of global oil supply - and roughly 12 to 14 percent of Europe's LNG imports, mostly from Qatar - transits this 34-kilometre waterway. Even if Ras Laffan were fully operational, it cannot export what ships cannot safely carry out (Wikipedia, 2026 Strait of Hormuz crisis).

Second: South Pars / Iranian domestic production. Iran is the world's fourth-largest consumer of natural gas, behind the US, China, and Russia. South Pars provides 80 percent of Iran's domestic gas supply. The March 18 strikes removed 12 percent of that production - not export capacity, but domestic supply. Iran's consequent halt of gas exports to Iraq cascades: Iraq loses a third of its power generation capacity, immediately and indefinitely.

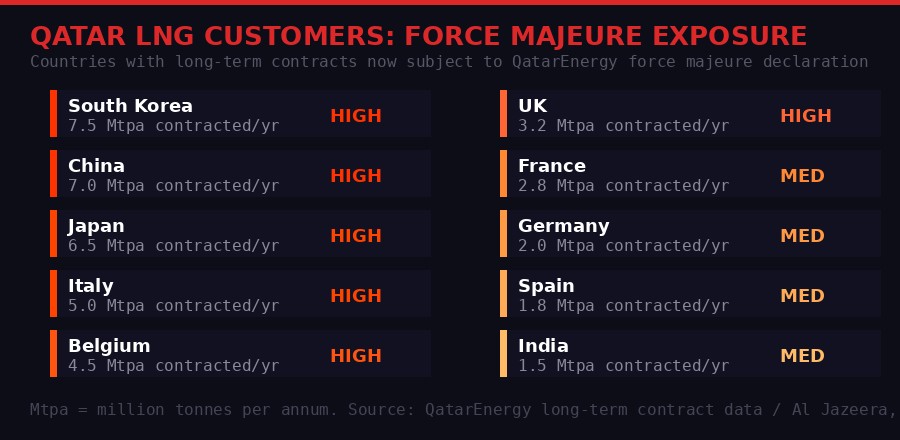

Third: Ras Laffan itself. The direct hit. Two liquefaction trains destroyed, one GTL facility offline, $26 billion of infrastructure damaged. Force majeure declared on long-term contracts with South Korea, China, Italy, Belgium, and others. 12.8 million tonnes per year removed from the market for years.

Layer those three disruptions and the combined impact on accessible global natural gas supply is the figure that has terrified energy markets since Thursday morning: approximately 17 percent offline, with no short-term path to replacement.

Force Majeure: The Legal Earthquake Under the Numbers

Force majeure is the legal mechanism by which QatarEnergy is releasing itself from long-term LNG contracts. (Illustrative)

"These are long-term contracts that we have to declare force majeure. We already declared, but that was a shorter term. Now it's whatever the period is." - Saad al-Kaabi, CEO of QatarEnergy, to Reuters, March 19, 2026

Force majeure is the clause buried in every long-term commodity contract that releases a party from obligations when events outside their control make delivery impossible. QatarEnergy has now invoked it - not for weeks, but for up to five years - on contracts with some of the world's largest LNG buyers.

Named in al-Kaabi's Reuters interview as force majeure targets: Italy, Belgium, South Korea, and China. These are not spot market buyers. These are countries with decade-long contracts, infrastructure built around guaranteed Qatari supply, import terminals and power plants calibrated to specific LNG volumes from Ras Laffan. Being told their supply is gone for five years is not a pricing problem. It is a structural crisis that requires reorienting entire national energy strategies.

Countries with significant Qatar LNG contract exposure now under force majeure risk. (BLACKWIRE infographic / QatarEnergy contract data / Al Jazeera)

The scale of this legal action has no modern precedent in LNG markets. The closest analogues are sanctions-driven supply disruptions - Russia's gas cutoffs to Europe in 2022 - but those were gradual and partially anticipated. This happened in a single night. One missile barrage, and the world's largest LNG exporter is issuing force majeure notices for the next five years.

Al-Kaabi's words to Reuters carry the full weight of what this means: "For production to restart, first we need hostilities to cease." The Ras Laffan site is still in a conflict zone. Damage assessment cannot even begin until it is safe to do so. The three-to-five-year repair estimate is a minimum - it assumes peace, funding, and the availability of specialist LNG plant engineering capacity that is globally scarce.

Europe's Winter Calculation

European cities depend on natural gas for heating. The question now is where replacement supply comes from. (Illustrative)

Europe was still recovering from Russia's 2022 gas cutoffs when this war started. The continent spent three years and hundreds of billions of euros building LNG import infrastructure, signing long-term contracts with Qatar, Norway, and US suppliers, and refilling storage caverns to legally mandated levels. That preparation is now being stress-tested against a scenario that no European energy ministry modelled: simultaneous loss of Qatari LNG export capacity, Hormuz closure preventing the gas that does survive from moving, and the removal of any pathway back to normal within the medium-term planning horizon.

Europe gets 12 to 14 percent of its LNG from Qatar through Hormuz, according to Al Jazeera's background reporting on the Hormuz crisis (Wikipedia). That is not the majority of European gas supply, but LNG is the marginal fuel - the swing supply that balances the market when pipeline gas from Norway runs short or demand spikes in cold weather. Remove the marginal fuel and the entire price structure of the European gas market reprices upward.

Britain's pre-existing gas storage situation - described in earlier BLACKWIRE reporting as having less than two days of reserve capacity at peak demand - makes the UK the most exposed major European economy. With North Sea production declining and pipeline flexibility limited, British gas prices were already elevated before this war. The Ras Laffan strike has removed a direct source of UK LNG supply.

The leaders of Britain, France, Germany, Italy, the Netherlands, and Japan issued a joint statement on March 19 expressing readiness to contribute to "appropriate efforts" to ensure safe Hormuz passage and to stabilise energy markets (Al Jazeera, March 19, 2026). They committed to "working with certain producing nations to increase output." Norway, Australia, and US Gulf Coast LNG exporters are the logical targets of those conversations - but none of them can simply conjure 12.8 million tonnes of annual capacity from nothing. Australia is already running near maximum utilisation. US LNG export terminals are booked years in advance. New capacity requires years of construction.

The IEA's coordinated release of 400 million barrels of strategic petroleum reserves - the largest in its history - addresses oil, not gas. There is no strategic natural gas reserve equivalent. Countries hold gas in underground storage caverns, not in purpose-built emergency stockpiles. When those caverns drain through a cold winter, they drain.

The Price Shock in Context

Energy price spikes since February 28 have been faster than any prior conflict. Analysts no longer dismiss $200 oil. (Illustrative)

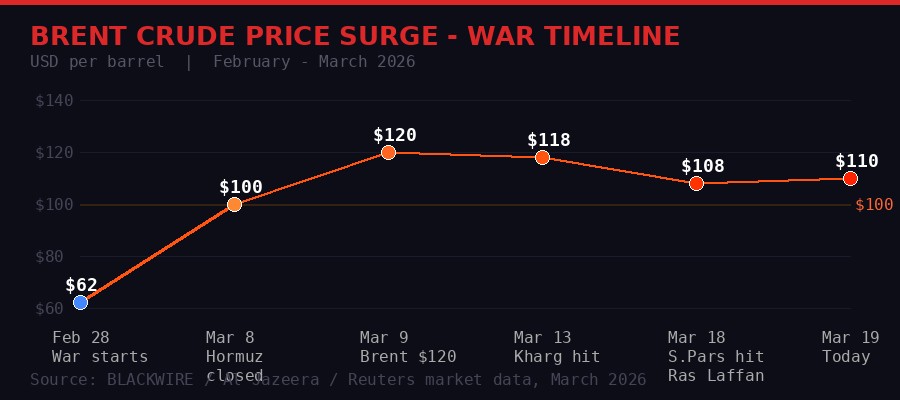

Brent crude price surge from the start of the Iran war. Each escalation has pushed prices higher with no ceiling now visible. (BLACKWIRE infographic / Reuters / Al Jazeera market data)

Oil prices are the visible signal most people track. Brent crude surpassed $100 per barrel on March 8, for the first time in four years. By its peak, it reached $126. The March 18 South Pars strike pushed it back above $108 after a brief consolidation. Analysts at Wood Mackenzie said last week that $150 Brent was expected, with $200 "not outside the realms of possibility" (Al Jazeera, March 19, 2026).

Vandana Hari of Vanda Insights told Al Jazeera: "Benchmark Middle Eastern crudes like Oman and Dubai have already crossed the $150 threshold, so $200 is already within sight, even if not for Brent and West Texas Intermediate."

But oil prices are the blunt instrument here. Natural gas tells the deeper story. Gas is not easily rerouted the way oil is. It moves through fixed pipelines or as LNG on specialised tankers loading from fixed terminals. When the terminals are hit and the shipping route is closed, the gas simply does not move. There is no fungible spot cargo available to plug the gap the way a Saudi Arabia can theoretically open its spigots to replace lost Iranian crude. Gas markets are less liquid, less flexible, and structurally more vulnerable to exactly the kind of targeted infrastructure attack that has now occurred.

European TTF gas futures - the benchmark for continental gas prices - have surged to levels not seen since the worst weeks of the 2022 Russian supply crisis. But analysts covering the 2022 crisis noted at the time that Europe ultimately absorbed the Russian loss because alternative pipeline routes and LNG from the US and Qatar could partially substitute. Today, one of those substitutes - Qatar - is the source of the disruption. Another - Hormuz-transiting LNG - is physically blocked. The buffer that saved Europe in 2022 no longer exists.

What 17% Offline Actually Means for Heating, Power, and Industry

Industrial production is deeply reliant on natural gas - as feedstock for fertilizers, chemicals, glass, steel, and food processing. (Illustrative)

Natural gas is not merely heating fuel. It is embedded in global industrial supply chains at multiple levels, and a sustained removal of 17 percent of global supply does not just mean higher heating bills. It means production cuts, industrial shutdowns, fertilizer shortages, food system stress, and a structural repricing of every good whose manufacture requires heat or chemical feedstocks.

The hierarchy of impacts, from most immediate to most structural:

Heating: The most politically visible. Households across Europe, Japan, South Korea, and China rely on gas for space heating. Price spikes translate directly to higher energy bills, and in Europe's case, the energy poverty crisis of 2022 - when millions of households cut consumption to afford bills - will return with greater severity. Governments will face pressure to subsidise bills again, at enormous fiscal cost, while simultaneously trying to fund war-related defence expenditure.

Power generation: Gas-fired power plants generate a substantial share of electricity in the UK, Germany, Italy, South Korea, and Japan. When gas prices spike, power prices spike. Industries that run 24-hour processes - aluminium smelting, cement production, chemical synthesis - face a choice between operating at a loss or shutting down. European aluminium production was already at historic lows after 2022. Another shock of this magnitude could permanently close capacity that takes decades to rebuild.

Fertilizers: Natural gas is the primary feedstock for nitrogen fertilizer production via the Haber-Bosch process. Approximately half of the world's population is fed by food grown with Haber-Bosch nitrogen fertilizers. When gas prices are high, fertilizer production becomes uneconomical. European and Asian fertilizer plants shut down. Farmers either cannot afford fertilizer or cannot source it. Crop yields fall. Food prices rise. The connection between an Iranian missile hitting a Qatari LNG train and a bread price increase in Lagos or Cairo is not metaphorical - it is a documented supply chain reality from 2022, about to repeat at larger scale.

Plastics and chemicals: Petrochemical production - the basis of plastics, pharmaceuticals, and industrial chemicals - draws on gas and gas condensates. The Asaluyeh complex in Iran, also damaged in the strikes, is one of the world's largest petrochemical clusters. Reduced output from both Iran and Qatar's gas-to-liquids operations compounds the pressure on global chemical supply chains that were only just recovering from post-pandemic and Ukraine-related disruptions.

Semiconductor fabs and data centres: Less obvious but equally real - advanced semiconductor fabrication facilities and large data centres require stable, continuous power. Gas-dependent grids that become unstable or expensive cascade into reliability problems for critical infrastructure. Asian semiconductor production hubs in South Korea, Japan, and Taiwan are watching the situation with alarm: Japan gets 95 percent of its crude from the Gulf, according to US Treasury Secretary Scott Bessent, and South Korea's gas import situation is even more acute.

The 1970s Comparison - and Why This Is Worse

The 1973 oil crisis produced fuel queues across the United States and Europe. The 2026 gas shock is structurally different - and arguably more severe. (Illustrative)

The 2026 Hormuz crisis has been described as "the largest disruption to the energy supply since the 1970s energy crisis" by multiple analysts, including sources cited in Wikipedia's Hormuz crisis article. The comparison deserves unpacking because the structural differences are as important as the surface similarities.

The 1973 oil embargo - imposed by OPEC Arab states in response to US support for Israel in the Yom Kippur War - reduced global oil supply by approximately 5 percent. It lasted about five months. The effect was devastating: petrol rationing in the US and Europe, a 400 percent oil price increase, and a recession that lasted years. But it ended with a political negotiation. Saudi Arabia and the other OPEC states turned the taps back on when the diplomatic calculus changed.

The 1979 Iranian Revolution and subsequent Iraq-Iran War removed Iranian and Iraqi production for a period, again triggering a major oil shock. Again, other producers - Saudi Arabia, the US - compensated over time. The shocks were severe but resolvable through political change and production shifts.

The 2026 crisis differs in three fundamental ways:

Infrastructure damage, not production restraint. The 1970s crises were policy decisions - states choosing to withhold supply. The 2026 disruption is physical destruction of irreplaceable infrastructure. Ras Laffan's destroyed LNG trains cannot be switched back on by political decision. They require engineering, construction, and years of work. Even if peace broke out tomorrow, the repair clock would still run its three-to-five year course.

Natural gas, not oil. Oil is more substitutable. You can burn different grades of crude, you can shift shipping routes, you can release strategic reserves. Natural gas is locked into fixed pipeline infrastructure and specialised LNG terminals. Countries that built their heating and industrial infrastructure around specific gas supply contracts cannot simply switch fuels in a winter. Germany's post-Russian-gas-cutoff adjustment took two years of emergency infrastructure construction, enormous subsidy spending, and significant economic pain - and Germany was starting from a position of peace, not active regional war.

Multiple simultaneous vectors. The 1970s oil shock came from a single policy lever: OPEC's production decision. The 2026 crisis compounds at least four simultaneous disruptions: the Hormuz closure (blocking transit), South Pars damage (Iran domestic), Ras Laffan destruction (Qatar export), and the cascading threat to Saudi, UAE, and other Gulf energy facilities from ongoing IRGC strikes. The IRGC issued evacuation orders for the SAMREF refinery, Jubail petrochemical complex, Al Hosn gas field, and Mesaieed complex on March 18 (Wikipedia, 2026 South Pars field attack). If those facilities are hit, the supply hole deepens further.

"In several respects, the conditions today could allow for an even more dramatic move than the Gulf War, given the larger share of global supply potentially at risk and the wider imbalance between supply and demand that presents." - Chad Norville, President of Rigzone, to Al Jazeera, March 19, 2026

The Countries Most Exposed

Cities across East Asia and Europe face a fundamental gas supply reckoning over the next five winters. (Illustrative)

Japan stands at the apex of exposure. Ninety-five percent of Japan's crude oil comes from the Gulf. Japan is also one of the world's largest LNG importers, with long-term Qatari contracts central to its gas supply strategy. With the Hormuz strait essentially closed and Qatar's production now force majeure'd, Japan's energy security situation is the most acute among major economies. Prime Minister Takaichi has told parliament that Japan is reviewing the scope of possible action "within the limits of its constitution" - but constitutionally constrained military action will not unblock the Strait of Hormuz, and there is no pipeline alternative to Gulf LNG for Japan.

South Korea faces a near-equivalent crisis. One of QatarEnergy's largest LNG customers, South Korea is now named as a force majeure recipient. Its gas-dependent power grid and heavy industrial sector - steel, shipbuilding, petrochemicals - face input cost shocks of an order that could tip the economy into recession.

China's situation is complex. China receives approximately a third of its oil via the Strait of Hormuz, and has significant Qatari LNG contracts. Beijing has been notably quiet during the war - a silence that analyst Yang Xiaotong, writing in Al Jazeera, calls evidence that "when core interests are at stake, even close partners are expendable." China has been negotiating individual safe passage deals with Iran for its own ships. It is managing its exposure bilaterally rather than joining any multilateral response. Whether that approach can continue to insulate Chinese supply through a five-year infrastructure gap is the central question facing Beijing's energy planners.

Iraq is in immediate crisis. Iran halted gas exports to Iraq on March 18, the same day as the South Pars strikes. Between a third and 40 percent of Iraq's electricity generation relied on that Iranian supply. Blackouts have already begun in Baghdad. Iraq's electricity grid was already operating at the margin of stability before the war - this removal of supply is not an inconvenience, it is a governance crisis. The Iraqi government's ability to maintain basic services through a hot Middle Eastern summer without that gas is genuinely in doubt.

Italy and Belgium - both named in al-Kaabi's Reuters interview as force majeure recipients - face their own version of the problem. Italy in particular has been one of the most Qatari-gas-dependent large European economies, having built substantial regasification capacity partly in response to 2022. That infrastructure now has nothing to receive.

What Comes Next: Repair Timelines and Replacement Scenarios

Rebuilding LNG trains requires specialist contractors, years of work, and a secure construction environment. None of those conditions exist yet. (Illustrative)

The three-to-five year repair estimate from al-Kaabi is conditional on the cessation of hostilities. That condition does not exist today. The IRGC has threatened further strikes on Gulf energy infrastructure. Iranian Foreign Minister Abbas Araghchi told reporters on March 19 that Iran would show "ZERO restraint" if its infrastructure is struck again. The Ras Laffan complex - and other Gulf energy facilities - remain active military targets in an active war.

Even assuming peace breaks out rapidly, the reconstruction challenge is formidable. LNG liquefaction trains are among the most complex pieces of industrial machinery in existence. There are a handful of specialist engineering firms globally capable of building them - primarily in the US (Air Products, Bechtel), Europe (Shell, TotalEnergies), and Japan (JGC, Chiyoda). Their order books were already full with expansion projects before this war. Qatar's expansion plans - the North Field East and South expansion projects intended to take Qatari LNG capacity from 77 million to 126 million tonnes per year - have been suspended indefinitely. The engineers and materials required to repair the damaged trains now compete with those same expansion plans, with offshore reconstruction projects, and with the global infrastructure investment surge driven by the energy security shock.

Replacement supply scenarios require honest assessment of lead times. The US Gulf Coast has significant new LNG export capacity under construction or recently commissioned - Sabine Pass, Corpus Christi, Plaquemines LNG. But these are already contracted. Redirecting them to replace Qatari supply for Italy or South Korea means breaking or renegotiating other contracts. Australia's liquefaction capacity is near maximum. East African LNG projects in Mozambique and Tanzania are years from completion. There is no tap anyone can turn in 2026 or 2027 to replace 12.8 million tonnes of annual Qatari LNG output.

The medium-term scenario most favoured by energy analysts is a painful but manageable adjustment: higher prices for three to five years, accelerated investment in non-Gulf LNG supply, faster deployment of heat pumps and electrification in Europe, and increased demand destruction from high prices reducing consumption. The 2022 Russian gas crisis demonstrated that European demand can fall significantly - by 12 to 15 percent - when prices are high enough. That demand destruction is essentially a managed energy poverty regime: wealthy households pay more, poor households cut usage, industrial sectors partially mothball.

The worst-case scenario is that hostilities continue, that the IRGC follows through on its threats to Saudi and UAE energy infrastructure, and that the global gas market loses not 17 percent of supply but 30 or 40 percent - a number that cannot be absorbed through demand destruction alone. At that point, the parallel to the 1970s oil crisis breaks down entirely: the 1970s crisis caused recessions. This would cause something closer to a structural reorganisation of global industrial production.

The Bottom Line

Al-Kaabi, speaking to Reuters from Doha while his company's facility still smoulders from the previous night's missile strikes, put it with a directness that cuts through the diplomatic noise:

"The scale of the damage from the attacks has set the region back 10 to 20 years." - Saad al-Kaabi, CEO QatarEnergy, Reuters, March 19, 2026

Ras Laffan Industrial City took three decades to build. Qatar poured oil revenues into it, attracted foreign investment from Shell, TotalEnergies, ExxonMobil, and ConocoPhillips, and transformed a barren peninsula into the world's most concentrated energy export node. That investment and those decades are not fully destroyed - but a significant portion of the capacity they created is offline, and the war that destroyed it is not over.

The world is now running a multi-year energy supply deficit that cannot be papered over with strategic reserve releases, diplomatic statements, or speculative alternative supply. Somewhere between 12 and 17 percent of global natural gas supply is simply not available. The machines that would produce it are either damaged, blocked from export, or operating in an active war zone that nobody has a clear plan to end.

That is the number governments, corporations, and households need to plan around. Not as a pessimistic scenario. As the base case.

The question is not whether the next five winters will be harder. They will be. The question is how much harder, and whether the political systems of the affected countries can absorb the social pressure that higher energy prices consistently produce - or whether this energy crisis, like some of its predecessors, contributes to the kind of political instability that makes wars longer, not shorter.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSources: Al Jazeera (March 19, 2026 multiple reports); QatarEnergy CEO Saad al-Kaabi via Reuters; Wikipedia - 2026 South Pars field attack; Wikipedia - 2026 Strait of Hormuz crisis; Wikipedia - South Pars/North Dome Gas-Condensate field; IEA Global Gas Security Review 2024; EIA Strait of Hormuz analysis; Wood Mackenzie via Al Jazeera; Vanda Insights via Al Jazeera; OCBC Group Research via Al Jazeera; Rigzone via Al Jazeera.

BLACKWIRE | nixus.pro | March 19, 2026