Wall Street Gets $175 Billion. Bitcoin Gets Punished. The Fed's Double Standard Is Now Official Policy.

Fed Vice Chair Michelle Bowman just handed the biggest US banks a $175 billion capital windfall - softening Basel III requirements, easing discount window stigma, and cutting global surcharges by 10%. The same regulatory apparatus is simultaneously keeping crypto locked out. This is not an accident. It is policy.

On March 12, 2026, Federal Reserve Vice Chair for Supervision Michelle Bowman stepped to a podium and said something that would have been unthinkable three years ago: the post-2008 Basel III capital rules that Wall Street had spent a decade trying to destroy are getting a soft rewrite. Capital requirements stay roughly flat or edge lower. Global bank surcharges drop 10%. And the discount window - the Fed's emergency lending facility that banks avoided like a scarlet letter - is being repositioned as usable everyday infrastructure.

For the biggest US banks, this is worth $175 billion. That is the estimated excess capital that could be freed up across the industry under the revised framework, according to CryptoSlate and Fed watcher analysis. The number is not a projection or a model output. It is the direct consequence of rolling back a capital standard that was designed - explicitly - to prevent another 2008.

Meanwhile, Bitcoin sits at $71,600. ETF flows are returning. Glassnode calls market conditions "fragile, stabilizing." And the regulatory apparatus that just handed Wall Street its biggest win in a decade is maintaining a strict two-track policy: traditional banks get relief, crypto gets the boot.

The contradiction is not accidental. It is structural. And understanding why it exists tells you more about the future of crypto regulation than any SEC speech or congressional hearing.

The Basel III Rewrite: Three Years of Bank Lobbying Pays Off

Start with the history. Basel III endgame - the post-2008 global capital accord designed to make banks safer by forcing them to hold more equity against their assets - was finalized internationally in 2017 but had never fully landed in the US. Under former Fed Vice Chair for Supervision Michael Barr, a 2023 proposal would have raised capital requirements at the biggest US banks by approximately 19%. Banks labeled it existential. JPMorgan ran an ad campaign. Industry groups lobbied Congress.

The proposal died without being implemented. Barr departed. Bowman took over. And now, less than three years after that proposed 19% increase, the new draft lands capital requirements roughly flat or slightly below current levels. Once related adjustments are included, large banks may end up with fewer total constraints, not more.

The numbers: large-bank capital surcharges - the extra cushion required from the biggest globally systemically important banks (G-SIBs) - are set to fall by about 10%. The excess capital freed across the industry sits at $175 billion or more by current industry estimates.

"Excessive capital requirements carry real economic costs and can interfere with banks' basic job of supplying credit to the broader economy." - Fed Vice Chair Michelle Bowman, March 12, 2026

That framing - capital as a drag on credit rather than a shield against failure - marks a philosophical reversal from the post-SVB consensus. After Silicon Valley Bank collapsed in March 2023, regulators said the lesson was clear: banks needed better oversight, stronger buffers, and tighter liquidity management. The 2026 rewrite says the lesson was: do less.

Basel III Endgame: Then vs Now

Senator Elizabeth Warren issued a direct warning in response. Her objection cuts through the political noise to the core contradiction: Washington said after SVB that bank resilience had to come first. Now, with growth fears, market volatility, and funding sensitivity back in view, Washington is preparing to give the largest banks more room to breathe.

But the banking lobby is not the only winner. The second piece of this policy shift is arguably bigger - and far less covered.

The Discount Window Gambit: Redesigning the Fed's Backstop

Alongside the capital rewrite, Treasury officials are taking a fresh look at liquidity rules. The proposal: give banks regulatory credit for collateral they have already prepositioned at the Federal Reserve's discount window. In plain terms, regulators may start treating a bank's ability to borrow emergency cash from the Fed as part of its usable liquidity pool.

This sounds technical. The implications are enormous.

For decades, the discount window existed in theory but not in practice. Banks avoided it because using it was seen as a public signal of distress - the financial equivalent of calling 911. The stigma was so severe that during the 2008 crisis, the Fed had to create multiple emergency facilities with different names specifically so banks could access liquidity without triggering the discount window association.

Treasury is now calling this stigma a design flaw. Officials described prepositioned collateral at the discount window as "real, monetizable liquidity" - language that reframes the Fed backstop from an emergency tool to a routine component of a bank's liquidity architecture.

Translation: Instead of requiring banks to hold liquid assets in case of a run, regulators may accept collateral sitting at the Fed as a substitute. Banks get more flexibility. The Fed's emergency lending function becomes embedded in the everyday liquidity calculus. The system becomes structurally dependent on central bank rescue infrastructure even in what officials call "normal" conditions.

This is the part of the policy shift that the Bitcoin community should be tracking most closely. Bitcoin's critique of the banking system has always pointed to exactly this dynamic: the system's apparent stability depends on central bank backstops that are never fully priced into official risk assessments. Every time you hear a regulator say the banking system is "safe and sound," the implicit addendum is "because the Fed will catch us if we fall."

The 2026 discount window repositioning makes that addendum explicit. It is an acknowledgment that the banking system does not, in practice, self-regulate through capital and liquidity buffers alone. It survives because the central bank stands behind it. And now regulators are formalizing that arrangement as policy rather than emergency contingency.

The Macro Backdrop: Worst Possible Timing

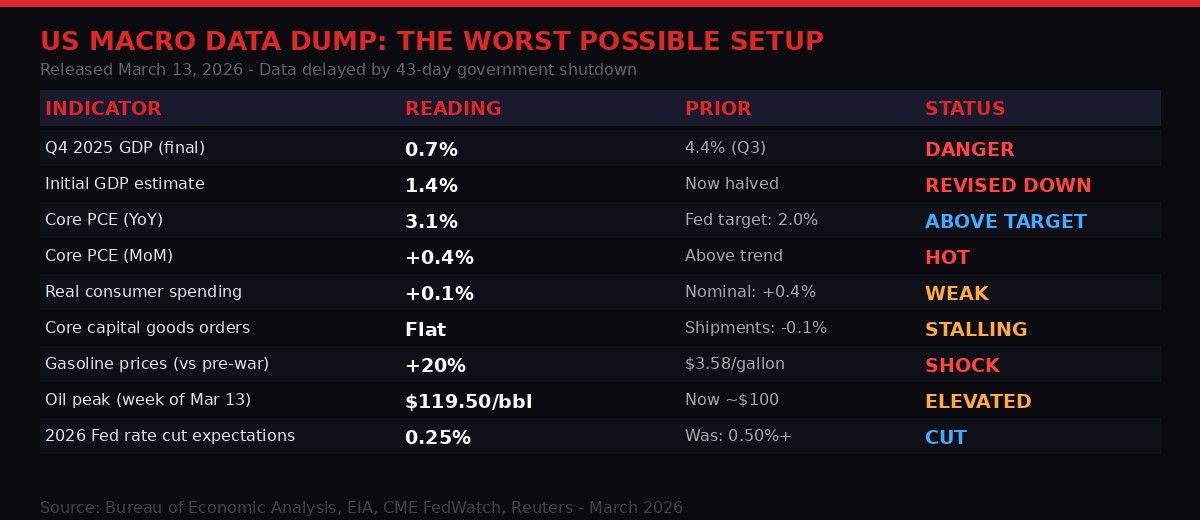

This regulatory pivot is not happening in a vacuum. It is happening while the US economy is showing its worst data combination in years - slower growth, sticky inflation, and an oil shock that is making everything more complicated.

On March 13, the Bureau of Economic Analysis released data that had been delayed by the federal government's 43-day shutdown. The Q4 2025 GDP was revised down to 0.7% annualized growth - cut in half from the initial 1.4% estimate. The prior quarter had come in at 4.4%. This is not a soft landing. This is a sharp deceleration hitting just as the US-Israeli war on Iran spiked oil to $119.50 a barrel.

Core PCE - the Fed's preferred inflation measure - sits at 3.1% year over year, with a 0.4% month-over-month increase. The Fed's target is 2.0%. The current federal funds rate target is 3.50%-3.75%, unchanged since January. That combination - 3.1% core inflation against 3.50% nominal rates - leaves very little real rate pressure. The Fed is not meaningfully tight. It is treading water.

Then comes the oil shock. The war that began February 28 pushed Brent crude to its highest level since 2022. At peak, WTI hit $119.50 this week before easing back toward $100. US gasoline prices are up 20% since the war began, now sitting at $3.58 a gallon nationally.

Goldman Sachs has modeled the macro impact: a temporary move to $100 oil shaves 0.4% off global growth and adds 0.7% to global headline inflation in the upside scenario. Reuters reports economists see March consumer prices potentially rising as much as 1% month-over-month. The backward-looking data already looked uncomfortable before the energy shock. The February CPI and January PCE numbers predate the war. The next prints will show the full hit.

This is the classic stagflation setup: growth falling, inflation rising, a central bank with no clean move, and a regulator simultaneously choosing to ease bank capital standards. The timing is not a coincidence. It is a policy bet that credit creation matters more than capital cushions right now.

The Fed meets March 17-18. Futures markets have scaled back expected 2026 rate cuts to roughly 0.25 percentage points by December - down from over 0.50 points before the Iran conflict. A hold is virtually certain. The question is whether Powell's language tilts hawkish on inflation or acknowledges growth risk. Neither outcome gives risk assets clean support.

Bitcoin at $71,600: Fragile Stabilization in a Hostile Environment

Bitcoin peaked intraday at $74,000 on March 13 before pulling back sharply as news of US military movements in the Middle East rattled risk assets. It fell 3.5% in hours. The coin now trades around $71,600 - up 4.2% on the week, but running into the worst macro environment for risk assets in years.

The internal data is better than the external environment warrants. US spot Bitcoin ETFs took in a net $583 million from March 9 through March 12, according to Farside Investors - a meaningful reversal after a $348.9 million outflow on March 6. Funding rates have turned negative rather than euphoric, removing speculative froth. Options volatility has eased. Glassnode reports growing upside interest around $75,000 with a main demand zone at $60,000-$69,000.

Glassnode's summary: conditions are "fragile, with spot demand beginning to recover rather than fully recovered." That is a precise read. The market is not in freefall. It is not in rally mode. It is stabilizing in a macro environment designed to prevent the rally from sustaining.

The scenario table is clean but uncomfortable. Bull case - oil retreats, Fed treats the shock as temporary, BTC retests $75,000 - requires conditions that are not in evidence. Base case - oil holds near $100, Fed signals cautious uncertainty - keeps BTC range-bound through April. Bear case - inflation hardens, "higher for longer" gets reinforced - puts the $60,000-$69,000 zone back in play.

The black swan scenario - prolonged Hormuz disruption - shifts the entire narrative from "temporary energy hit" to "policy trap." Bitcoin in that environment trades as a stressed risk asset, not a safe haven. The correlation to the Nasdaq reasserts. The digital gold narrative takes a hit. The $60,000 floor gets tested in earnest.

Meanwhile, Strategy - the largest corporate Bitcoin holder - would need to buy approximately 6,158 BTC per week to hit 1 million coins by end of 2026, per CoinDesk analysis. At current prices, that is over $430 million per week in purchasing pressure. Strategy has exceeded that pace in recent months. But sustained buying at that pace into a macro headwind and potential regulatory tightening is not guaranteed.

The Regulatory Double Standard: Bitcoin's Capital Treatment

Here is the part that deserves more attention than it is getting. While Bowman is engineering a $175 billion capital windfall for traditional banks, the same regulatory framework is maintaining a completely different set of rules for institutions that want to hold Bitcoin.

Under Basel III's existing treatment of crypto assets - which was finalized internationally in 2022 and has been cited by US regulators since - Bitcoin and most other cryptocurrencies carry a 1250% risk weight for capital purposes. That means a bank that holds $1 million in Bitcoin must hold $1 million in risk-weighted capital against it - effectively a 1:1 capital backing requirement. This is the maximum possible risk weighting under the Basel framework, reserved for assets regulators consider essentially worthless or speculative.

Compare that to the capital treatment just handed to traditional bank assets under the new rewrite: roughly flat or slightly below current requirements, with global surcharges cut by 10%. A bank's exposure to US Treasuries, corporate bonds, and leveraged loans gets lighter capital treatment. Bitcoin exposure - despite being publicly traded, highly liquid, and increasingly held in regulated ETFs - gets maximum punitive capital treatment.

The Kraken precedent is instructive. The Federal Reserve recently granted Kraken Bank a limited master account, giving the first crypto institution direct access to Fed settlement infrastructure. Custodia Bank, which has spent years and millions in legal costs fighting for the same access, lost its court battle just days after Kraken's account was granted. The message: the Fed will let one crypto-native institution access its infrastructure on a limited basis, while another entity fighting for the same right gets shut down in court.

This is not a coherent regulatory framework. It is ad hoc gatekeeping.

DOJ Pivot, Senate Drama, and the Stablecoin Battle

The capital rules story does not exist in isolation. Multiple regulatory fronts are moving simultaneously - and the pattern is consistent. Traditional finance gets room to breathe. Crypto gets squeezed or fragmented.

US Senators fired a letter at the Department of Justice last week over its decision to shut down the National Cryptocurrency Enforcement Team (NCET), its dedicated crypto crime unit. The concern: several senior DOJ officials involved in crypto enforcement hold personal cryptocurrency positions. The senators raised the conflict-of-interest issue directly. The DOJ has not publicly responded. The NCET's wind-down continues.

On Capitol Hill, Coinbase has threatened to pull its backing for the Senate's stablecoin legislation. The company objected to specific provisions that would tighten oversight on non-bank stablecoin issuers - provisions that could kneecap Circle, USDC's issuer, in its race against Tether. The bill, which had broad bipartisan support weeks ago, is now stalling. Investment bank analysts have started warning publicly that the 2026 election cycle could delay major US crypto legislation into 2027 or beyond.

Barclays made its first stablecoin investment, taking a stake in Ubyx, a UK-based stablecoin infrastructure company. This is a significant signal: a major UK bank is betting on stablecoin infrastructure at the same time US regulators are fighting over stablecoin oversight rules. The competitive dynamic - UK and EU moving forward while US debates - is familiar. It played out with ETFs in 2021-2023. It may be playing out again with stablecoins now.

Brazil's industry groups - representing 850 companies - issued a formal objection to a proposed stablecoin tax, arguing it would be unconstitutional. Brazil's Virtual Assets Law explicitly does not classify stablecoins as fiat currency. Taxing them as such would, in the industry's view, violate both the statute and the constitution. The case will likely go to court.

In India, security agencies flagged a "crypto hawala" network allegedly used for terror funding in Kashmir - a story that will give domestic Indian regulators ammunition against crypto adoption even as the country's broader fintech sector continues to grow rapidly. The China angle is equally dark: the architect of China's digital yuan (e-CNY) program has been accused of accepting $8 million in crypto bribes, according to reporting this week. The irony of a state-backed crypto official taking unofficial crypto payoffs is not lost on market observers.

What the Pattern Means: Who Controls the Infrastructure

Pull back from the individual stories and a pattern emerges. The Fed is redesigning the banking system around a closer relationship between commercial banks and central bank backstop infrastructure. The discount window becomes embedded. Capital cushions thin. Banks get more room to move. The Fed gets a more central role in everyday financial plumbing.

Bitcoin's critique of this system is that it is structurally dependent on centralized rescue. Every "the banking system is safe" statement contains the implicit assumption that the Fed will act if it is not. The 2026 capital rewrite makes that assumption explicit - and then writes it into the rules.

At the same time, the regulatory apparatus is maintaining maximum friction for Bitcoin specifically. Not because Bitcoin is more dangerous than the assets in a bank's trading book. Not because it is less liquid than a leveraged loan portfolio. But because it represents an alternative to the system being redesigned. An asset that does not need the discount window. A network that does not need Fed settlement infrastructure. A monetary system that has no master account to grant or revoke.

Druckenmiller said stablecoins could become the whole payment system in 10-15 years and reiterated that crypto might replace the US dollar as the global reserve currency. He is not alone in that view. Stanley Druckenmiller is not a permabull. When he says stablecoins matter, he means the payment infrastructure story is real. When he says crypto could replace the dollar as reserve currency, he means the competition for monetary dominance is already underway.

That competition is why the regulatory double standard exists. Banks are part of the existing system. Their stability is the Fed's institutional mandate. Bitcoin is a structural alternative. Its growth, at scale, represents a transfer of monetary authority. Regulators are not stupid. They understand what they are doing when they hand banks $175 billion in freed capital while maintaining 1250% risk weights on Bitcoin exposure.

The FOMC Meeting: March 17-18 Is the Pivot Test

The Federal Open Market Committee meets in two days. The rate decision is not the story. The hold is coming. The story is Jerome Powell's language about what happens next.

The Fed faces what economists call a policy trap. Growth is falling - Q4 GDP at 0.7% confirms the economy entered the oil shock on weak footing. Inflation is sticky - core PCE at 3.1% gives the Fed no room to ease. Oil above $100 is making both sides of the equation worse simultaneously. The "higher for longer" narrative that suppressed risk assets through 2023-2024 is re-emerging.

If Powell leans hawkish - emphasizing inflation patience, downplaying growth risks - rate-cut expectations fall further. Real yields could rise. Risk assets, including Bitcoin, face a harder environment. The $60,000-$69,000 demand zone becomes the relevant reference point.

If Powell leans dovish-but-cautious - acknowledging energy uncertainty, signaling patience without committing to cuts - the market gets neither relief nor clear pressure. BTC stays range-bound. The $74,000 intraday high from last Thursday remains the ceiling until something breaks the pattern.

The one scenario markets are not pricing: Powell acknowledges both the inflation risk and the growth risk explicitly, signals a longer pause, and frames the energy shock as a genuine stagflation setup. That language would hit risk assets hard. The S&P 500, already fragile, would face a repricing. Bitcoin would face a test of whether its correlation to equities holds or whether the "digital gold" bid absorbs the selloff.

Fed Week Scenarios: March 17-18, 2026

The Bottom Line: Two Systems, Two Sets of Rules

What March 2026 has produced is a clarifying document. The regulatory system is not neutral. It does not apply consistent risk standards across asset classes. It is actively designed to protect and support the traditional banking infrastructure while maintaining maximum friction for its decentralized alternatives.

The $175 billion capital release is not a market outcome. It is a political decision dressed in technical language. Bowman's speech on March 12 will be studied by bank regulatory historians as the moment the post-2008 capital consensus broke. Three years after SVB showed exactly what insufficient capital and liquidity standards produce, the Fed is rolling back the corrective measures.

The discount window redesign is even more significant long-term. When central bank emergency infrastructure becomes part of everyday liquidity planning - when "the Fed will catch us" moves from implicit assumption to explicit policy - the banking system's dependency on public backstops becomes impossible to obscure. Bitcoin's core argument - that the traditional system relies on perpetual central bank intervention to maintain the appearance of stability - stops being a critique and becomes official acknowledgment.

For traders, the near-term read is clear: Bitcoin holds $71,600 going into Fed week. The $74,000 high is the ceiling. The $60,000-$69,000 zone is the floor if the macro deteriorates. ETF inflows are returning, funding is not euphoric, and the internal structure is better than the external environment.

But the bigger story is structural. Washington is redesigning its financial system to give traditional banks more flexibility and the Fed a more central role. Simultaneously, it is maintaining maximum regulatory pressure on the one asset class that does not need either. That is not random. That is a system defending its own architecture.

The next test is March 17-18. Watch Powell's exact language. Watch whether he says "temporary" about the oil shock or dodges the word. Watch whether he acknowledges the growth-inflation tension explicitly. That framing will set the tone for the next three months - for rate expectations, for crypto regulation, and for whether the $175 billion handed to Wall Street was the beginning of a credit boom or the last policy move before a new stress event arrives.

Sources: Fed Vice Chair Michelle Bowman speech March 12, 2026 | CryptoSlate analysis March 14, 2026 | Bureau of Economic Analysis Q4 2025 GDP release | CoinDesk markets coverage March 14-15, 2026 | Farside Investors ETF flow data | Glassnode on-chain analysis | CME FedWatch | Goldman Sachs oil shock macro model | Reuters March 2026 reporting

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram