Open Season: How DOGE Dismantled the IRS Unit That Hunts Billionaire Tax Cheats

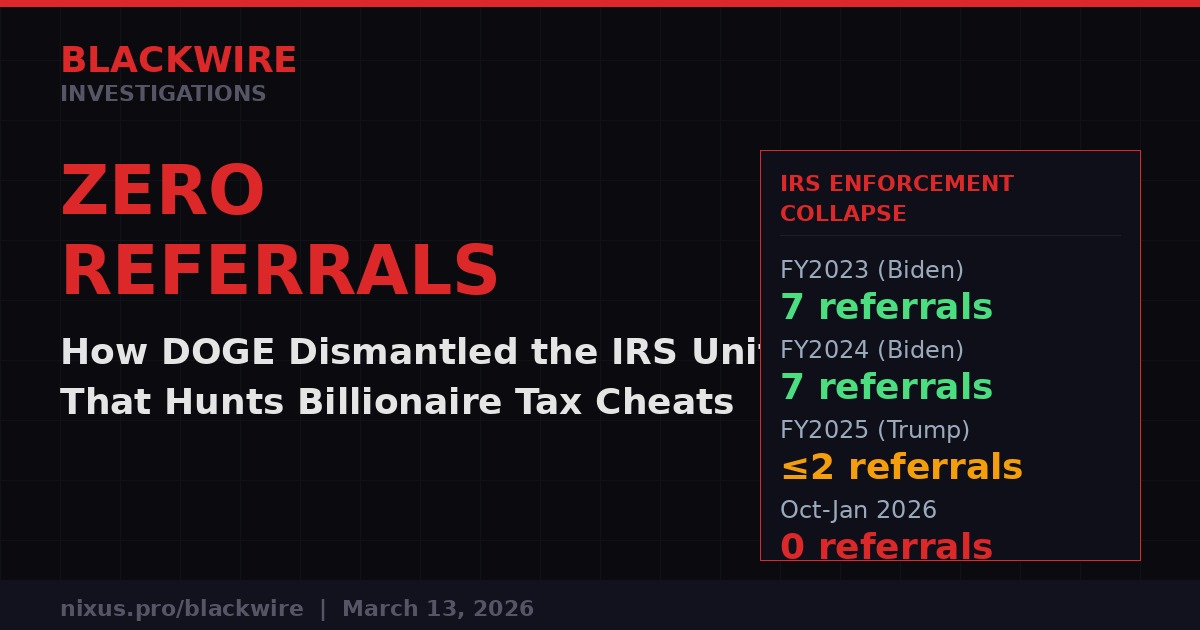

Between October 2025 and January 2026, the IRS referred zero cases of billionaire or corporate tax fraud to criminal investigators. Zero. The unit that once held the wealthiest Americans to account has been gutted - and the people doing the gutting are the same people who would have been investigated.

The numbers are stark and the implications are worse. The Internal Revenue Service's Large Business and International Division - the unit tasked with auditing America's wealthiest taxpayers and biggest corporations - referred at most two cases of possible tax evasion to its criminal investigators during all of fiscal year 2025. Between October 1, 2025 and January 31, 2026, the number was zero.

Not a slow quarter. Not an administrative delay. Zero.

That data, obtained by the International Consortium of Investigative Journalists, represents the most complete picture yet of what the so-called Department of Government Efficiency has actually achieved inside the IRS: the systematic dismantling of the enforcement infrastructure that targets the wealthiest and most powerful tax cheats in America. And it happened while a billionaire ran the cutting operation.

Oct 2025-Jan 2026

of FY2025

FY2023 & FY2024

billionaire audit unit

The Unit Nobody Talks About - Until It Stops Working

The Large Business and International Division is not a household name. That is by design. It operates in the unglamorous space between dense tax code provisions and complex corporate structures - the territory where sophisticated tax fraud lives. The division audits companies with assets over $10 million and oversees the IRS's Global High Wealth program, a specialized office dedicated to examining the tax returns of billionaires and high-net-worth individuals.

Criminal referrals from the LB&I division are the gateway to prosecutions. They are not routine paperwork. They represent a determination by civil IRS agents that a taxpayer has engaged in conduct so egregious - fraud, willful evasion, deliberate concealment - that it warrants escalation to the Criminal Investigation division for potential prosecution.

Not every referral becomes a prosecution. Not every prosecution results in conviction. But the referral is the trigger. Without it, the pipeline stops. And the pipeline has now stopped entirely for America's wealthiest taxpayers.

The last time the LB&I division produced this few referrals was fiscal year 2019. That figure is now confirmed by the new data, placing the current moment at a historic low. To find a similar enforcement vacuum, you have to go back to a period before the IRS had even begun the Biden-era push to rebuild its enforcement capacity.

The Anatomy of a Purge

The sequence of events that produced this enforcement vacuum follows a pattern familiar to anyone who has studied regulatory capture. It begins not with a direct order to stop enforcing the law, but with personnel cuts deep enough to make enforcement operationally impossible.

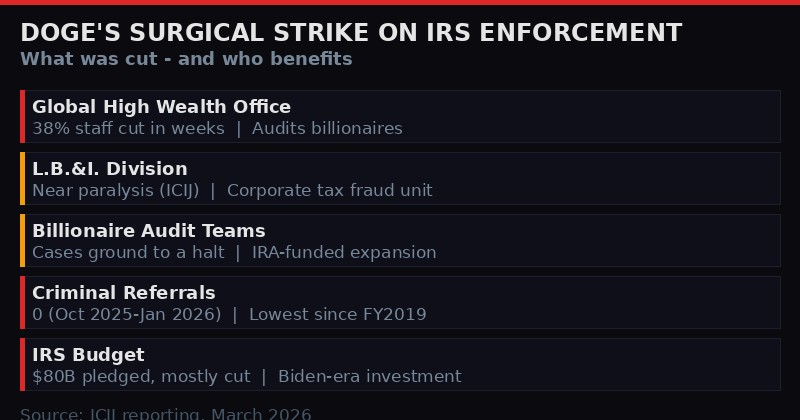

Within weeks of Donald Trump returning to the White House in January 2025, the Global High Wealth office lost 38 percent of its staff. These were not mid-level bureaucrats processing paperwork. They were experienced agents who had spent years learning to untangle the complex trust structures, offshore accounts, and inter-entity transactions that characterize billionaire tax strategies.

The expertise required to audit a billionaire's tax return is not transferable on short notice. It takes years to develop the institutional knowledge to follow a paper trail through a family limited partnership into a Cayman-registered holding company and out through a charitable remainder trust. When you lose 38 percent of that specialized workforce in a matter of weeks, cases do not just slow down - they collapse.

IRS agents assigned to billionaire audits told ICIJ that their cases ground to a halt as teams were decimated and budgets frozen under the cost-cutting program led by Elon Musk. The word those agents used was not "reduced." It was paralysis.

"Unless we start treating illegal schemes as what they are, there's no incentive to stop," said Michael Welu, a former IRS agent who focused much of his career on helping auditors identify major cases for criminal referral. The logic is simple: if sophisticated tax fraud now carries the deterrent effect of a parking ticket rather than a prison sentence, sophisticated tax fraud will increase.

Robert Warren, a former IRS agent and assistant professor at Radford University who also reviewed the new data, put it bluntly: "If you're engaging in a large tax evasion scheme and you're a company under the authority of the Large Business and International division, the chances of you going to jail are like that of getting hit by lightning."

What DOGE Actually Cut - and the Numbers Behind It

The public framing of DOGE's IRS activities focused on reducing "waste" and "bloat." The operational reality was different. The cuts hit hardest at the divisions created or expanded under the Inflation Reduction Act - the 2022 legislation that directed approximately $80 billion toward the IRS over a decade, with the explicit mandate to rebuild enforcement capacity that had eroded through years of Republican-led budget cuts.

The Biden administration's IRS investment produced measurable results before it was reversed. The Global High Wealth office expanded from a skeleton operation into a functioning unit capable of pursuing complex, multi-year audits of the kind that sophisticated tax shelters require. In fiscal years 2023 and 2024, the LB&I division made seven criminal referrals each year - not a large number in absolute terms, but a meaningful upward trend from the anemic baseline of 2019.

That trend is now not merely reversed but obliterated. The new data shows that the division made at most two referrals during all of FY2025, which began in October 2024, and zero between October 2025 and January 2026.

The cuts were not random. The IRA-funded hires were disproportionately recent recruits who lacked civil service seniority protections. They were among the first to be fired when Trump returned to power and DOGE began its work inside the agency. The result was that the offices with the most recent investment - the offices rebuilt specifically to target the wealthiest taxpayers - were hollowed out fastest.

ICIJ reported last year that IRS management was grappling with lost agents, orphaned cases, and uncertainty about future layoffs. Overworked and understaffed audit teams, Welu explained to ICIJ, are less likely to spend the extra time required to craft a criminal referral on egregious cheating - even when they encounter it. The administrative burden of producing a referral is significant. Exhausted teams working with depleted resources will default to civil settlements, if they close cases at all.

The Conflict of Interest That Washington Will Not Name

There is a structural fact at the center of this story that mainstream coverage has been reluctant to state plainly: the billionaire directing the government efficiency program that gutted IRS enforcement is himself a subject class of the enforcement that was gutted.

Elon Musk, whose net worth fluctuates between $250 billion and $400 billion depending on the market, is precisely the kind of ultrawealthy individual that the Global High Wealth program was designed to scrutinize. His financial structures - spanning Tesla equity, SpaceX holdings, X ownership, xAI ventures, and a range of personal trusts and foundations - are exactly the complex, multi-entity arrangements that require years of specialized IRS expertise to audit properly.

This is not an allegation that Musk has evaded taxes. It is an observation that the person who dismantled the unit that would have audited him is the person who would have been audited. In any other context - a bank regulator eliminating the department that audits his own bank, a drug regulator dissolving the office that inspects his pharmaceutical company - this would be treated as a textbook conflict of interest requiring immediate recusal.

In the current political environment, it has passed largely without consequence. The IRS declined to comment on the new enforcement data when approached by ICIJ. The agency's acting leadership, installed after the departure of Biden-era Commissioner Danny Werfel in January 2025, has made no public statements addressing the enforcement collapse documented by the data.

- Danny Werfel - IRS Commissioner 2023-2025. Resigned January 2025 with Biden administration. Reviewed new data for ICIJ and warned of consequences.

- Elon Musk - Directed DOGE cost-cutting program that decimated IRS billionaire audit teams within weeks of Trump's return.

- Michael Welu - Former IRS agent, specialist in criminal referral process. Warned: "There's no incentive to stop."

- Robert Warren - Former IRS agent, assistant professor at Radford University. Reviewed data; compared likelihood of prosecution to "being hit by lightning."

- Global High Wealth program - IRS office dedicated to billionaire audits. Lost 38% of staff within weeks of Trump's January 2025 inauguration.

The Tax Gap and Who Actually Bears the Burden

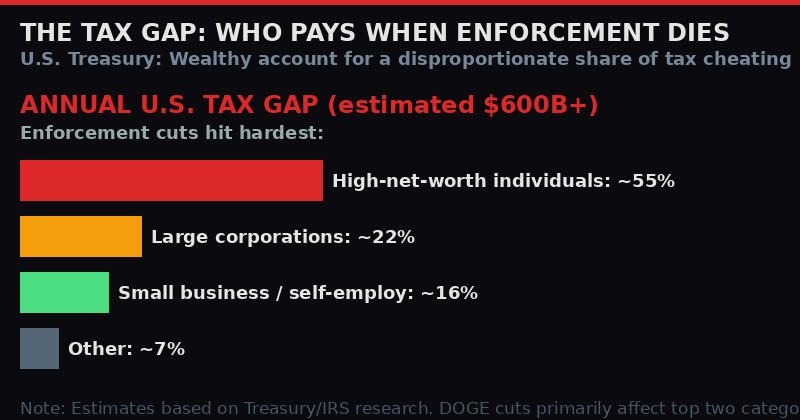

The U.S. tax gap - the difference between what Americans legally owe and what they actually pay - is estimated by the Treasury Department at over $600 billion annually. That figure is not distributed evenly across income groups. The Treasury's own research shows that the wealthiest Americans account for a disproportionately large share of tax cheating.

This is not counterintuitive when you understand the mechanics. A wage worker's taxes are withheld at source. There is no opportunity for complex structuring, because there is nothing to structure. A billionaire's income, by contrast, flows through a labyrinth of entities whose tax treatment depends on elections, valuations, and characterizations that require expert examination to verify. The complexity is not incidental - it is the medium through which sophisticated evasion operates.

When the IRS cannot effectively audit that complexity, the burden shifts. Honest taxpayers - the wage earners, the small business owners, the salaried professionals whose income is verifiable and whose deductions are modest - continue to pay what they owe, because they have no mechanism to do otherwise. The wealthy, facing reduced scrutiny, face reduced consequences for non-compliance.

Werfel put the mechanism precisely: the tax burden does not shrink when enforcement capacity is removed. It redistributes. Those who choose not to play by the rules shift the cost of funding the government to those who do. The result is a wealth transfer - from compliant middle-class taxpayers to non-compliant ultrawealthy ones - that is invisible in the budget numbers but real in its economic effect.

The scale is not trivial. IRS research suggests that closing even a fraction of the tax gap among high-net-worth individuals and large corporations could generate hundreds of billions in additional revenue annually. The Biden administration estimated its IRS investment would generate $400 billion in additional collections over a decade. That estimate is now academic - the investment has been reversed before it could fully take effect.

A Timeline of Deliberate Dismantling

What Enforcement Actually Deters - and What Happens Without It

Criminal referrals are not the only metric of IRS enforcement, but they are among the most powerful deterrents. The threat of criminal prosecution - with its attendant publicity, reputational damage, and potential incarceration - operates differently from the threat of a civil fine or audit settlement. A corporation or ultrawealthy individual can budget for civil penalties. They can treat fines as a cost of doing business. Criminal prosecution is categorically different in its deterrent effect.

When referrals dry up, word travels. The tax attorney community, the accounting firms that advise billionaires and major corporations, and the compliance officers at large companies are all aware of enforcement signals. When IRS capacity collapses, when the unit that hunts complex tax fraud loses nearly 40 percent of its people and falls silent on criminal referrals, the market for aggressive tax strategies - for schemes that push against or past the legal boundary - becomes more attractive.

This is the deterrence collapse that Welu warned about. The cost-benefit calculation for tax cheating among the wealthy has shifted. The expected value of an aggressive scheme - the potential tax saving, multiplied by the (now much lower) probability of detection and prosecution - has changed dramatically. Sophisticated tax planners run these numbers. They know what the data shows.

Warren, the Radford University professor and former IRS agent, gave a precise assessment of the changed landscape: "It's logical to expect a drop in referrals when you have so few agents. If you're engaging in a large tax evasion scheme and you're a company under the authority of the Large Business and International division, the chances of you going to jail are like that of getting hit by lightning."

The comparison to lightning is apt in another sense: it is not just improbable, it is practically impossible to predict or prevent. That kind of randomness is corrosive to enforcement culture. Agents who know their referrals will go nowhere - because the capacity to process and prosecute them no longer exists - have diminished incentive to invest the enormous time and expertise required to build a criminal referral case. The paralysis feeds on itself.

The Deeper Pattern: Regulatory Capture in Plain Sight

What is happening at the IRS is not novel in its structure. It is the same mechanism that has operated in financial regulation, environmental enforcement, and antitrust law across multiple administrations and multiple decades. A regulatory agency accumulates expertise and capacity. A new administration, typically one aligned with the interests of the regulated class, appoints leadership hostile to the agency's mission. Budget cuts follow. Experienced personnel depart. Cases stall or close. The deterrent effect erodes. And the behavior the agency was built to deter becomes more common.

What is unusual about the current moment is its speed and its transparency. The conflict of interest between the person directing the cuts and the class of taxpayers who benefit from the cuts is not hidden. It is publicly known. Musk's wealth and its sources are extensively documented. The IRS's Global High Wealth program was designed precisely for people in his financial position. He ran the program that gutted it. And the data now shows, quantitatively, what that gutting has produced.

Tax scholars and former enforcement officials interviewed by ICIJ in earlier reporting were careful to note that the IRS's capacity to pursue civil enforcement - audits, assessments, and penalty proceedings - remains partially intact, though also degraded. But civil enforcement, without the criminal backstop, is a fundamentally weaker instrument. It removes the prison threat. It reduces the reputational stake. And for the very wealthy, it turns the IRS into a negotiating counterparty rather than a law enforcement agency.

The distinction matters. When civil enforcement is the only tool available, the question becomes not whether you evaded taxes, but how much you will pay to make the audit go away. For billionaires and major corporations with armies of lawyers, the answer to that question is almost always less than what they would have owed had the fraud been criminally prosecuted and publicly exposed.

What Comes Next - and What Would It Take to Reverse

The enforcement data covers a period ending January 31, 2026. There is no indication, from the current administration's public statements or budget proposals, that the trajectory is about to reverse. To the contrary, the administration's fiscal year 2027 budget proposals are expected to include further reductions to the IRS's discretionary appropriations, building on the legislative reversal of IRA enforcement funding that began in 2023.

Rebuilding the capacity that has been destroyed would take years under the best circumstances. The Global High Wealth office lost 38 percent of its specialized staff. Replacing them is not a matter of hiring bodies - it requires recruiting professionals with the specific expertise to audit complex financial structures, training them in the specific requirements of the IRS's processes, and then retaining them long enough to develop the institutional knowledge that makes the work effective. That pipeline runs in years, not months.

The political path to restoring IRS enforcement funding is also unclear. The Inflation Reduction Act's IRS provisions were already partially clawed back in bipartisan budget negotiations before Trump's return. Republican opposition to IRS enforcement spending - framed consistently as opposition to "weaponizing the IRS against ordinary Americans," despite the data showing enforcement focused overwhelmingly on the wealthy - remains entrenched.

Former Commissioner Werfel's warning is the most concise diagnosis of what the numbers mean: when enforcement capacity is removed, honest taxpayers pay more, dishonest ones pay less, and the gap between them widens. The IRS enforcement data is a ledger. It shows what has been removed. What it cannot yet show - but what economic theory and enforcement history both predict - is the behavioral response to that removal. That response is already underway, in ways that will not be visible in the data for years.

The referral count for October 2025 to January 2026 is zero. That number will not remain symbolic. It will, over time, become structural - embedded in patterns of tax behavior among the wealthy that will outlast whatever political changes eventually restore the enforcement apparatus. The damage from enforcement vacuums is not symmetrical. It takes much longer to rebuild deterrence than it does to destroy it.

Zero is not just a number. It is a signal. And among those sophisticated enough to read it, the signal has been received.

Data obtained: IRS Large Business and International Division criminal referrals by fiscal year, provided to ICIJ.

ICIJ's reporting was led by: Investigative team using enforcement statistics obtained from the agency and reviewed by former IRS officials including Danny Werfel (Commissioner 2023-2025), Michael Welu (former IRS agent, criminal referral specialist), and Robert Warren (former IRS agent, Radford University).

The IRS declined to comment.

Original ICIJ reporting: icij.org - IRS criminal referrals plummeted during Trump's first year

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram