Dalio's $9 Trillion Debt Wall, Bitcoin's Equity Decoupling, and the Most Confused Market in History

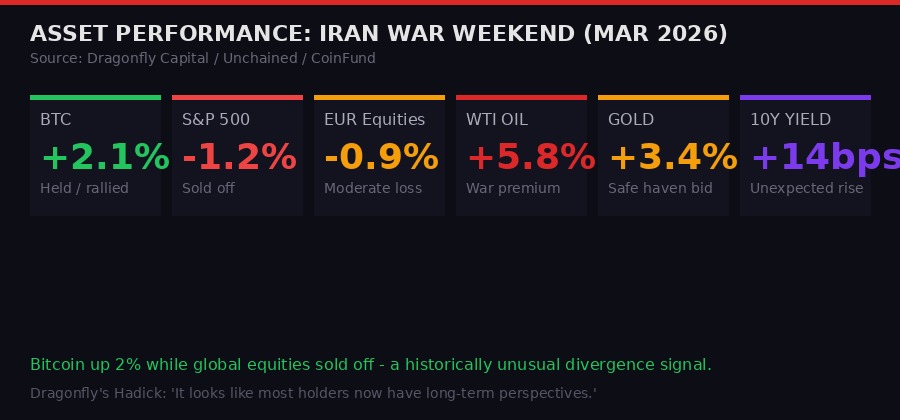

Bitcoin went up 2% while global equities sold off. Bonds are doing the opposite of what every model predicts. And Ray Dalio - the man who built the world's largest hedge fund - just publicly declared that the US has to roll over $9 trillion in debt this year alone. Three events, one week, one conclusion: nobody actually knows what happens next.

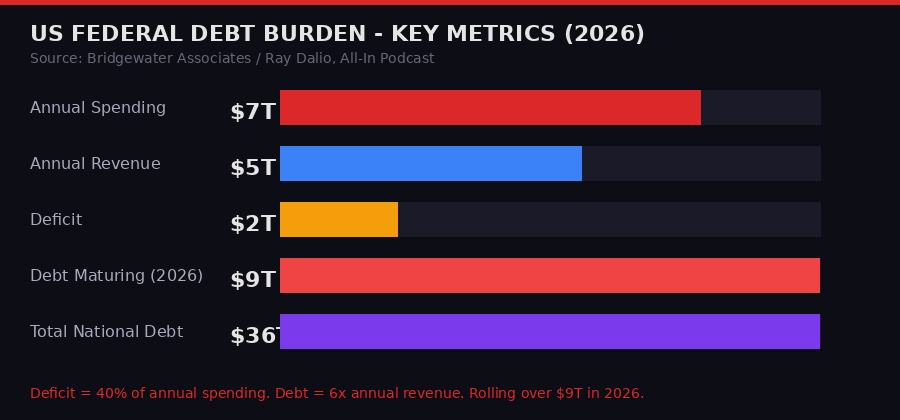

Friday the 13th, March 2026. The Iran war drags into its third week. Oil is still elevated. The 10-year Treasury yield is climbing - not falling, as every textbook says it should when people panic. Bitcoin is up on the week. The S&P is not. And in the background, Bridgewater founder Ray Dalio just dropped a number on the All-In Podcast that deserves more airtime than it is getting: $9 trillion. That is how much US federal debt matures this year and needs to be rolled over into new bonds.

The US government currently spends $7 trillion per year and takes in roughly $5 trillion, according to Dalio's figures cited on the podcast. That is a $2 trillion annual deficit running at approximately 40% of government expenditure. The total national debt now stands at more than 600% of annual government revenue. Dalio's framing is not ideological. It is arithmetic.

Meanwhile, crypto's most prominent institutional voices - Rob Hadick of Dragonfly Capital, Chris Perkins of CoinFund, and Tushar Jain of Multicoin Capital - are all pointing at the same anomaly: crypto held up. Not just held up. In the case of Bitcoin, it actually gained ground over a weekend when every other risk asset was getting liquidated. That is not noise. That is a signal worth parsing.

Snapshot: March 13, 2026 Market State

Ray Dalio and the Five Forces That Are Breaking Everything

Ray Dalio does not do social media hot takes. When the Bridgewater founder spent 40 minutes on the All-In Podcast laying out his macro framework in detail, it was worth writing down. His thesis is built on five forces that he says he has tracked across 500 years of economic history. Those forces are: the debt and money cycle, the wealth and values gap between domestic groups, the rise and fall of great powers, acts of nature, and the technology cycle.

Right now, according to Dalio, all five are firing simultaneously. The debt cycle is at a late-stage extreme. Wealth inequality in Western democracies is at levels not seen since the 1920s. The great power competition between the US and China - plus secondary conflicts involving Iran, Russia, and smaller proxies - is accelerating. Climate disruption continues to be priced as a slow-moving background risk but is increasingly showing up as acute shocks. And AI is rewriting productivity assumptions faster than any economic model can track.

"I've studied these big cycles in history going back 500 years. There are five major forces that determine the trajectory of the economy. They don't operate sequentially - they operate simultaneously, and they compound each other." - Ray Dalio, Bridgewater Associates founder, All-In Podcast, March 2026

The government finance piece is the most immediately actionable. Dalio compares government balance sheets to corporate ones - revenue, expenses, assets, liabilities - but with one critical difference: governments can print money. That printing option has suppressed the full reckoning on debt for decades. But Dalio's argument is that printing to cover deficits has a ceiling, and the US is approaching it faster than most Treasury officials will publicly admit.

The numbers: $7 trillion in annual spending. $5 trillion in annual revenue. $2 trillion deficit. National debt exceeding $36 trillion. And critically - $9 trillion of that debt matures this year, meaning the US Treasury must issue new bonds to refinance it. The buyers of those bonds are increasingly domestic (the Federal Reserve and US banks), because foreign buyers, according to Dalio, now view US dollar-denominated debt as a geopolitically risky asset. That is a structural change that took decades to build and could take only months to unwind.

The Bond Paradox: Why Yields Are Moving the Wrong Direction

Here is the thing that is breaking risk models right now. In a standard flight-to-safety scenario - a war breaks out, equity markets sell off - money flows into US Treasury bonds, pushing bond prices up and yields down. That is the textbook trade. That is what happened in every major crisis from 2008 to 2020.

That is not what is happening in March 2026.

Treasury yields are rising as equity markets sell off. The dollar is simultaneously strengthening. The two normally have an inverse relationship - a strong dollar makes dollar-denominated bonds more attractive to foreign buyers, which should push yields down. Instead, both are climbing together. Rob Hadick, General Partner at Dragonfly Capital (approximately $4 billion in assets under management), flagged this explicitly on the Unchained podcast this week.

"Yields are actually going up right now which is sort of what you would not expect. Bonds obviously move inversely with bond prices, and you would think bonds would be going up along with the dollar. But they're going in opposite directions. I think right now there's just more confusion in the market than ever - you actually have different people trading different markets who are coming to completely different conclusions in a way we haven't seen before." - Rob Hadick, General Partner, Dragonfly Capital, Unchained Podcast, March 2026

The interpretation that fits these data points is stagflation. Rising yields suggest the market expects the Federal Reserve to keep rates elevated - or even raise them further - because inflation is not defeated. But the conditions driving inflation are supply-side: oil prices up due to Iran war, supply chains still fragile from tariff regime shifts, wage pressures from the AI transition. The Fed cannot fix supply-side inflation with rate hikes without causing serious demand destruction. So the market is pricing a scenario where inflation stays high AND growth slows AND rates stay elevated. That is the triple threat of stagflation.

Dalio sees this risk too. His view is that sustained disruption to Persian Gulf oil flows - which control approximately 20% of global supply through the Strait of Hormuz - would lock in a stagflationary backdrop for the remainder of 2026. Trump has publicly stated the Iran conflict will run "at least four weeks." Analysts at multiple desks interpret "at least" as meaning "probably much longer."

Iran conflict = oil supply shock / WTI elevated. US tariff regime = import price inflation. Fed rate hold = credit market stress. $9T bond rollover at elevated rates = government crowding out private credit. Bond yields rising despite equity sell-off = market confusion / stagflation pricing. No clear Fed pivot signal on horizon.

Bitcoin's Decoupling - Signal or Noise?

Bitcoin up 2% on a weekend when global equities were selling off. On its own, one data point. But the way Dragonfly's Hadick framed it - and the way CoinFund's Chris Perkins framed it independently - this was not a coincidence. This was a behavioral signal about who is holding Bitcoin right now, and why they are not selling.

"I actually think it's quite positive that crypto and Bitcoin held up quite well over the weekend. It looks like there aren't necessarily a lot of sellers left. Most of the people holding now have much more long-term perspectives. The crypto markets are not as fragile as maybe the equity markets are right now." - Rob Hadick, Dragonfly Capital, Unchained Podcast

The thesis is structural. The marginal seller of Bitcoin in 2021-2022 was a retail participant - someone who bought near the top, panicked on a negative headline, and hit the market sell button. In 2024-2025, the institutional bid arrived through spot ETFs approved by the SEC. BlackRock's IBIT, Fidelity's FBTC, and a dozen other products absorbed massive inflows from pension funds, endowments, family offices, and treasuries. Those buyers do not panic-sell on a war headline.

Chris Perkins, Managing Partner and President of CoinFund and a former Citi futures and clearing executive, put it this way: the volatility index going up while markets are flat is actually a bullish sign. It means fear is being priced without corresponding selling. When real panic hits, you see both - VIX spikes AND prices collapse. The current setup suggests the market is nervous but not liquidating.

Tushar Jain, Co-Founder of Multicoin Capital, adds another layer: the market is showing apathy, not despair, and historically that is a better bottom signal than panic. Capitulation bottoms are sharp and emotional. Apathy bottoms are long, slow, and boring. The fact that crypto did not crash this week, despite every macro reason it could have, is itself informative.

"We are starting to see apathy in the market which is a good sign - it shows you that a lot of people have just kind of given up or washed out of it. I don't feel like we have hit that negative sentiment yet. But there is capital on the sidelines that is waiting to come in now." - Tushar Jain, Co-Founder, Multicoin Capital, Empire Podcast

The counterargument deserves air time too. Hadick acknowledges a 10-15% correction in the S&P would test Bitcoin's stability. Large ETF holders - institutional money - may have risk limits that force de-risking across asset classes if equity drawdowns breach thresholds. Bitcoin's correlation to equities has historically spiked during genuine financial crises (2020 COVID crash, 2022 FTX/Three Arrows). Decoupling works until it doesn't. The structural question is whether the institutional holding base has genuinely changed the sell behavior - or whether it will capitulate in the next real shock.

Gold Reasserts Itself - Dalio's Reserve Currency Thesis

While the Bitcoin decoupling debate was playing out, gold quietly extended its year-to-date gains. XAU is up over 3% on the week, continuing a multi-month trend that began when the Iran conflict first escalated. Gold is doing exactly what textbooks say it should do when bonds stop being the safe-haven asset of choice.

Dalio's take on gold is more structural than tactical. He pushed back hard on the characterization of gold as a "precious metal" or a "speculative asset." His argument on the All-In Podcast: gold is the most established form of money in human history, and the second-largest reserve currency held by central banks globally. It is the only major store-of-value asset that is not someone else's liability.

"It is the most established money. You have to understand that gold is not a precious metal - it is money. It is the long-term historic asset for reasons that mean it can be transferred. They can't print a lot of it, and it is not dependent on somebody giving you something. If you're holding money, you're holding it in the form of a debt instrument. Gold is different." - Ray Dalio, Bridgewater Associates, All-In Podcast

The implication for portfolio construction is significant. If US Treasuries are losing their safe-haven status - as the current bond market behavior suggests - investors need a replacement. Gold fills part of that role historically. Bitcoin proponents argue it fills a different part: the digital bearer asset that is similarly no-one's-liability but also programmable and globally transferable without custodians.

Neither gold nor Bitcoin can service the US government's $9 trillion debt rollover. That problem belongs to the Federal Reserve and the Treasury in a recursive loop that, according to Dalio, only gets resolved one of three ways: spending cuts large enough to matter (politically near-impossible), growth strong enough to outrun the debt (requires AI-driven productivity miracle), or monetization through inflation (the default historically). None of these are market-friendly in the short term.

The Clarity Act's Yield Language Landmine

Against this macro backdrop, Washington is attempting to pass legislation that would give the crypto industry long-sought regulatory clarity. The Digital Asset Market Clarity Act - referred to uniformly as "the Clarity Act" - has been moving through committee with more bipartisan support than any previous crypto bill. Multiple institutional analysts this week expressed cautious optimism that the legislation could pass in its current session.

But there is a landmine embedded in the current draft that the crypto industry did not see coming: yield language.

The bill as drafted contains provisions around stablecoin yield - specifically whether and how stablecoin issuers can pass interest or yield back to holders. The language, as currently written, would create regulatory complications for yield-bearing stablecoins and DeFi protocols that generate returns. Hadick described the reaction from inside the industry as significant concern.

"That yield language was kind of the thing that caused serious alarm inside the industry. The question is whether stablecoin issuers can pass through yields to holders, and the current draft language creates ambiguity that could effectively ban yield-bearing stablecoins. That is a major provision that could reshape the economics of DeFi." - Rob Hadick, Dragonfly Capital (paraphrased from Unchained Podcast)

Chris Perkins, who has direct experience working with regulators through his CFTC advisory committee role, frames the broader legislative issue differently. His read is that the Clarity Act's passage is essentially contingent on two things: the stablecoin bill passing first (as a companion piece), and the crypto industry demonstrating to skeptical Congress members that the sector has genuine real-world utility beyond speculation.

"Bitcoin and stablecoins have demonstrated clear product-market fit. The crypto industry needs to show more utility and real value to improve its reputation with Congress. The passage of clarity legislation is crucial for the true potential of the crypto market - but it has to be done right. Bad legislation is worse than no legislation." - Chris Perkins, CoinFund, Unchained Podcast

The stablecoin dimension adds a banking sector fight to the crypto legislative drama. The Clarity Act provisions that require stablecoin issuers to hold reserves at specific bank categories have created a divide between large banks and community banks - whose interests are not aligned - according to Perkins. Large banks want stablecoin issuers required to use federally chartered institutions (them). Community banks want access to stablecoin reserve deposits. The fight between these factions is delaying final language more than any ideological crypto debate.

Institutional Adoption as the New Floor

One consistent theme across all three analysts this week: institutional adoption is no longer a forecast. It is a structural fact that sets a floor under the crypto market that did not exist in previous cycles.

Tushar Jain's framing at Multicoin is the clearest. The engagement from the largest asset managers (BlackRock, Fidelity, Vanguard exposure through derivatives), from regulators (SEC, CFTC, OCC all now actively building crypto frameworks), from politicians (bipartisan crypto caucus in Congress), and from tech companies (Microsoft, Google, AWS all building blockchain infrastructure products) represents an institutional underwriting of the technology that is categorically different from 2018 or even 2021.

"There is basically a 0% chance that the crypto industry is over. We have engagement from the largest asset managers, from regulators, from politicians, from the biggest tech companies. Everyone has underwritten this technology. That is categorically different from previous cycles. This time around I'm not worried about existential risk at all." - Tushar Jain, Multicoin Capital, Empire Podcast

The investment implication from Multicoin's current thesis is also worth noting: Layer 1 blockchains are systematically misvalued relative to the applications running on top of them. Jain argues that DeFi protocols generating real, sustainable cash flows should be valued on discounted cash flow models - the same way traditional finance values companies. The market is currently applying speculative premiums to base layer tokens and speculative discounts to applications. That inversion, if his thesis is correct, will correct over the next 12-24 months as institutional capital applies more rigorous valuation frameworks.

Stablecoins are the one area where institutional and retail consensus is essentially unified. Total stablecoin supply has grown to over $225 billion. Cross-border settlement, AI agent payments, DeFi collateral, and emerging market dollar access are all driving structural demand that is largely immune to crypto market cycles. Perkins describes this as the "product-market fit" that gives the entire industry a defensible floor.

Timeline: How We Got Here and What Comes Next

The Forward View - Four Scenarios and Their Implications

Markets hate uncertainty. What they hate more is uncertainty compounding across multiple axes simultaneously. Right now, there are at least four independent variables that could resolve in ways that send markets sharply in different directions.

Scenario 1 - Iran conflict ends fast (4-6 weeks): Oil pulls back, stagflation narrative fades, Fed gets room to cut, risk assets rally broadly. Bitcoin would likely outperform as liquidity returns to the system. This is the scenario that Perkins at CoinFund calls "resolution faster than anticipated." The VIX-up-but-markets-flat signal he cites is consistent with this being the base case - fear priced, not catastrophe.

Scenario 2 - Conflict drags 3-6 months: Oil stays elevated. Stagflation becomes the dominant macro narrative. The Fed is stuck - can't cut without inflaming inflation, can't hike without crashing an already-stressed consumer. Gold continues to rally. Bitcoin's performance depends on whether institutional holders treat it as inflation hedge (bullish) or risk asset (bearish). Dalio would call this scenario "the messy middle." Most consistent with what his historical analysis of prolonged regional conflicts suggests.

Scenario 3 - Clarity Act passes with yield language fixed: Massive institutional inflow signal for DeFi and stablecoin sectors. Multiple analysts estimate $50-100 billion in fresh institutional capital is waiting for regulatory clarity before moving on-chain. A clean bill could be the biggest single-quarter catalyst for crypto since the spot ETF approvals. Probability: Perkins says growing sentiment, but legislative timelines are notoriously unpredictable.

Scenario 4 - Debt rollover stress: The $9 trillion maturity wall hits with insufficient demand from foreign buyers. Treasury yields spike to 5.5-6% range. The Fed is forced back into QE to absorb the issuance. Dollar weakens. This would be the scenario where Bitcoin and gold both function as monetary debasement hedges - and Dalio's gold-as-reserve-currency thesis plays out in real time. This is the low-probability, high-consequence tail that serious macro investors are quietly hedging against.

The honest answer is that no one has a high-confidence forecast right now. Hadick's observation that market confusion is at all-time highs is not hyperbole - it is a reflection of genuine model breakdown when bonds and equities stop their historical correlations simultaneously. The market participants who do best in this environment will be the ones who have sized correctly for uncertainty, who hold assets that perform across multiple scenarios, and who do not over-optimize for a single outcome.

Gold is doing that. Bitcoin is attempting it. The $9 trillion in US bonds that need to be sold this year? Nobody has a good answer for that yet. And that is probably the most important story in global finance in 2026 - and the one getting the least mainstream coverage.

Key Figures Cited This Week

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram