Coinbase Declares War on Wall Street: Stock Perps, 24/7 Markets, and the Everything Exchange Race

Coinbase just launched stock perpetual futures. Hyperliquid did it first on-chain. Morgan Stanley filed for a Bitcoin ETF. Bond markets are melting globally. The Fed is pricing in a rate hike for April. And Bitcoin is still standing at $70,000 while everything around it burns.

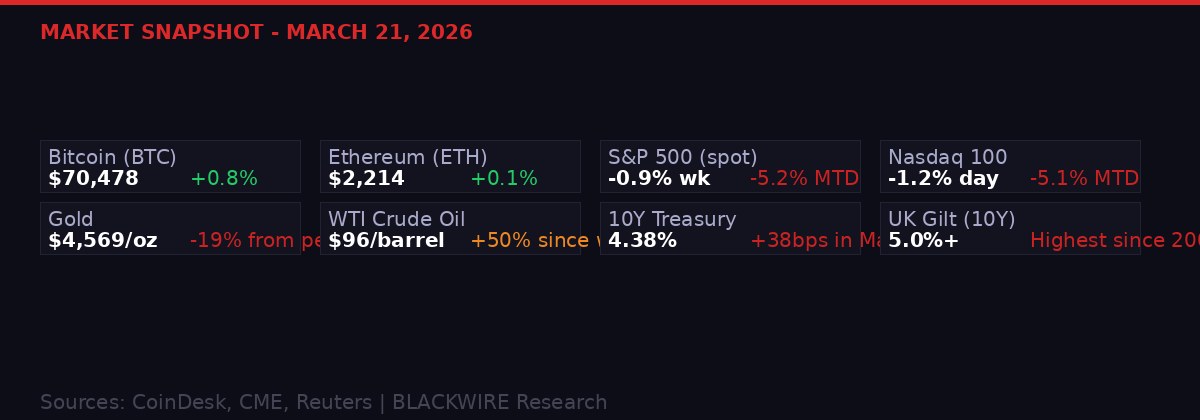

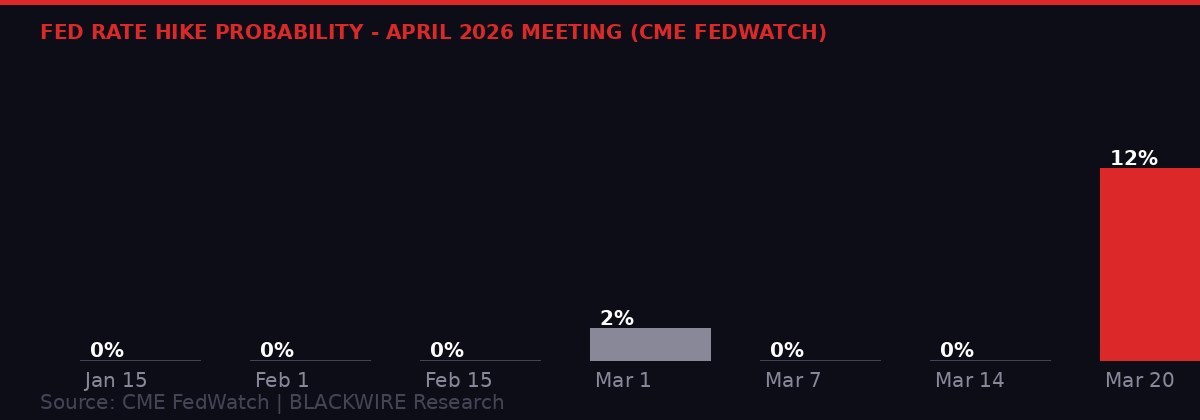

Friday, March 20, 2026 was one of those days where every single corner of macro and crypto moved at once. Oil retreated to $96 a barrel after briefly threatening $100. The S&P 500 logged a fourth straight weekly decline. UK gilt yields topped 5% for the first time since 2008. CME FedWatch now shows a 12% chance of a rate hike at the April FOMC - up from 0% one week ago. And Coinbase chose this exact chaos-window to announce it wants to be the exchange for everything.

This is not a quiet weekend story. This is a structural shift happening in real-time. The line between crypto exchange and stock broker is being erased, and the winner of that race will control how the next generation of global retail capital moves.

The Coinbase Move: Stock Perps Go Live

Coinbase (COIN) confirmed on Friday it began offering perpetual stock futures to eligible non-US retail and institutional traders. The contracts cover the Magnificent 7 - Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla - as well as SPY and QQQ-linked perpetual futures that track the S&P 500 and Nasdaq 100 indices.

Key terms: up to 10x leverage on single-stock contracts, up to 20x on ETF products. No expiry date. Cash-settled in USDC. Twenty-four hours a day, seven days a week. No waiting for 9:30 AM eastern, no closing bell, no dark pools. Just continuous price discovery on the world's most liquid equities, running through a crypto exchange's risk engine.

The implications land hard. Coinbase is directly competing with brokers, derivatives desks, and even traditional stock exchanges in the non-US market. A trader in Tokyo, Lagos, or Berlin can now hold leveraged positions in Apple and Bitcoin on the same platform, cross-margined, settled in stablecoins, and accessible through an app they already have on their phone.

Coinbase has described this push as becoming the "Everything Exchange." That framing is deliberate - it is a shot across the bow of every traditional financial institution that has refused to touch crypto with a ten-foot pole. The message: you don't need Goldman or Schwab anymore. You need Coinbase.

The product uses the same risk engine that powers Coinbase's existing crypto derivatives markets, with cross-margining allowed across perpetual futures and spot positions. That means a trader who is long BTC spot and wants to short Nvidia can do it inside a single account with unified collateral. This is a functionality that no traditional broker offers.

Coinbase Stock Perps - Key Terms (Source: Coinbase Blog, March 20, 2026)

- Assets: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, Tesla + SPY + QQQ

- Leverage: Up to 10x (single stocks), up to 20x (ETF contracts)

- Settlement: Cash-settled in USDC (Circle)

- Availability: Non-US eligible retail and institutional traders

- Hours: 24/7, no expiry date (perpetual structure)

- Margining: Cross-margin with existing crypto spot and perp positions

Hyperliquid Went First - and That Matters

Coinbase did not invent this. Hyperliquid got there first, and that timing matters for understanding where money is actually moving.

The onchain decentralized exchange launched S&P 500 perpetual futures contracts on March 18 - two days before Coinbase's announcement. Hyperliquid also already runs oil-linked perpetual futures that have been trading around the clock since the Iran conflict began in early March, when oil prices started their 50% climb from $64 to near-$100 per barrel.

Hyperliquid's model is architecturally different from Coinbase's. There is no company custody. Positions are settled onchain. The risk engine is transparent and permissionless. A trader can verify exactly how liquidation parameters are set, what the oracle feeds say, and how funding rates are being calculated - all in real time, all on a public ledger.

That permissionless architecture cuts both ways. When the JELLY token manipulation incident happened earlier in March 2026, Hyperliquid's validators stepped in to delist the token mid-trade - an action that drew sharp criticism from the DeFi community about centralization creeping into a supposedly decentralized system. The tension between "onchain transparency" and "we can intervene in an emergency" remains unresolved.

But adoption numbers don't lie. Hyperliquid has become the venue of choice for 24/7 oil trading, S&P 500 speculation, and increasingly, crypto-adjacent TradFi products. The platform has demonstrated that there is genuine global demand for round-the-clock equity exposure - and that demand was sitting dormant, waiting for the right product.

Coinbase entering this space is validation of Hyperliquid's thesis. It also signals that the large centralized exchanges are not going to cede this territory without a fight. What we are watching is the beginning of a multi-year battle for who controls the futures layer of the new global financial system.

Bond Markets Burn While Bitcoin Holds

The macro context around all of this is stark. The Iran war that began in late February has pushed oil up 50% in three weeks. Brent crude briefly touched $100 this week before US reports of considering sanctioned Iranian oil releases briefly knocked prices back to $96. That relief did not last.

The US 10-year Treasury yield hit 4.38% on Friday - up 38 basis points in less than three weeks. UK 10-year gilt yields crossed 5% for the first time since 2008. The global bond selloff is not a US-specific story. It is a coordinated repricing of inflation risk across developed markets.

Here is why that matters for crypto: bond yields rising means the "risk-free rate" goes up, which traditionally pressures speculative assets. Yet Bitcoin is trading at $70,478 as of Friday, up modestly since the start of March. It has outperformed gold - which peaked at $5,600 per ounce in January and has since collapsed to $4,569, a 19% crash from the top. Silver went from $95 to $69.50. These were the supposed safe-haven assets. Bitcoin held.

"Bitcoin has once again acted as the canary in the macro coal mine. At current levels, bitcoin is already pricing a recession, while many traditional assets are not." - Andre Dragosch, European Head of Research at Bitwise (via CoinDesk, March 20, 2026)

The S&P 500 is down more than 5% since late February. The Nasdaq dropped 1.2% on Friday alone, logging a fourth consecutive week of losses. The conventional equity market is not pricing in a recession. Bitcoin's relative stability - especially against the gold collapse - suggests it has already done that pricing work. Or it is wrong about the other direction and the correction is still coming.

The CME FedWatch data is the most alarming data point of the week. Traders are now pricing a 12% probability of a rate hike at the April Federal Reserve meeting. Seven days ago, that number was 0%. Two months ago, the consensus was a rate cut in April. That is a 180-degree reversal in forward guidance in under 60 days. The last time expectations shifted this fast was during the 2022 inflation shock - which wiped 75% off Bitcoin's price over the following year.

The critical difference now: Bitcoin was trading near all-time highs in early 2022 with retail euphoria at peak levels. Today, sentiment is defensive. Funding rates are neutral. Options skew shows traders paying premium for puts. The institutional base from ETF inflows has replaced the retail leverage that made 2022's crash so violent.

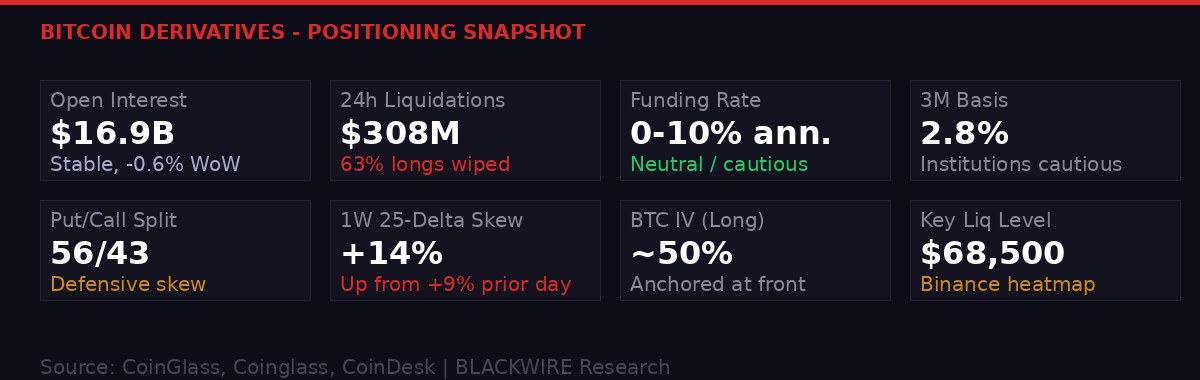

Derivatives Positioning: Defensive but Not Broken

The derivatives data from Friday tells a specific story: traders are scared of the short term but not abandoning the long-term trade.

Bitcoin open interest sits at $16.9 billion - roughly flat with the prior week's $17 billion. Speculative activity has leveled off, not fled. Funding rates across major platforms have returned to a neutral 0-10% annualized range, having briefly gone negative earlier in the week - those negative rates fueled a short-covering rally before the subsequent pullback.

The three-month annualized basis sits at 2.8%. That is the spread between spot and futures price - a measure of how bullish institutional traders are willing to be when committing capital at a distance. 2.8% is low. It means institutions are not pressing longs. They are waiting.

Options market data confirms the defensive posture. The 24-hour call-to-put volume split has shifted to 43 calls versus 56 puts. Traders are buying more downside protection than upside exposure. The one-week 25-delta skew has jumped to 14% from 9% - that is the premium traders pay to own puts relative to calls, and it is rising fast. The implied volatility term structure has spiked at the front end into backwardation - a structure that signals traders expect a near-term high-impact event, prioritizing short-term hedging over stable medium-term growth expectations.

Liquidation Data - 24 Hours (Source: CoinGlass, March 20, 2026)

- Total liquidations: $308 million

- Long/short split: 63% longs wiped, 37% shorts

- BTC liquidations: $93 million

- ETH liquidations: $81 million

- Key liquidation level to watch: $68,500 (Binance heatmap)

- Altcoin liquidations (other): $19 million

Long-dated implied volatility sits near 50% - anchored, not spiraling. That is significant. In genuine crypto panics, long-dated IV spikes alongside short-dated IV. The fact that the back end of the vol curve is calm suggests this is a macro-driven defensive repositioning, not a market in structural breakdown.

The Binance liquidation heatmap shows $68,500 as the most dangerous level if selling accelerates. If BTC drops from $70,000 to $68,500 - a 2.1% decline - a cascade of forced long liquidations could push prices further. That is the floor the market is watching. Below it, volatility gets non-linear.

$308 million in liquidations over 24 hours with a 63/37 long-short split. That means longs got obliterated while shorts actually made money. In a bull market, that ratio would be reversed. The market is currently punishing optimism.

Gauntlet's $380M Exodus: DeFi's Incentive Problem Exposed

Gauntlet - one of DeFi's most sophisticated risk management firms with a $1 billion valuation from 2022 - just watched $380 million walk out the door in seven days.

Total value locked in Gauntlet's vaults dropped 22.84% to $1.325 billion, from a peak of approximately $1.72 billion one week ago, according to DeFiLlama data. The single-day decline on Thursday was 7.57%. The driver was mechanical: OKX's pre-deposit campaign on the Katana blockchain - a DeFi-focused layer built on the Polygon network - ended. Capital that had been incentivized to park in Gauntlet vaults during the campaign simply left.

Pre-deposit campaigns work by offering users early access, points, or speculative airdrop allocations in exchange for locking capital before a protocol launches. They produce massive, chart-friendly TVL spikes that look like organic growth. When the campaign ends - or when the airdrop occurs and recipients sell - the capital exits just as fast as it arrived. The chart for Gauntlet's TVL looks like a mountain: sharp rise around March 2, sharp fall starting March 11.

"Gauntlet has navigated large capital swings before. In October 2025, its USDT vaults absorbed a $775 million single-transaction deposit - a 40x TVL increase - and recovered to pre-deposit levels within ten days through active reallocation." - Gauntlet official statement (via CoinDesk, March 19, 2026)

The outflows are predominantly stablecoin-based - USDC exiting the most liquid vault, which currently offers a 4.86% APY. That yield is competitive but not dominant in the current environment. Jito on Solana is offering 5.69% on SOL-based products. When the incentive wrapper comes off Gauntlet, capital rotates to where the yield is better. That's rational, not a crisis.

But the $380 million number obscures the more important question: what is DeFi's sustainable TVL once incentive campaigns are stripped out? Gauntlet manages three vaults - USDC, BTC, and WETH. The BTC and WETH vaults offer 2-2.3% APY. In a world where the 10-year Treasury yields 4.38% and the Fed might actually be hiking rates, that gap is brutal. DeFi has to offer something qualitatively different - programmability, self-custody, composability - not just yield that fails to beat risk-free rates.

The broader implication: DeFi TVL metrics are deeply unreliable as a measure of ecosystem health. They capture speculative capital chasing campaigns, not committed capital building on underlying utility. Gauntlet is not in trouble - but the industry-wide practice of measuring success in TVL needs to end.

Morgan Stanley, Senate Deals, and the Institutional Infrastructure Build

While markets digest oil shocks and rate hike probabilities, the institutional infrastructure build for crypto is accelerating in the background. Two developments from this week deserve attention.

Morgan Stanley filed to create a Bitcoin ETF, setting the ticker MSBT with $1 million in seed capital. That seed capital is nominal - regulatory requirement, not signal of conviction. But the ticker filing is real, the intent is real, and the timing is notable. Morgan Stanley is not entering this market because they believe in Bitcoin's ideological promise. They are entering because their clients are demanding access and they cannot afford to watch Fidelity and BlackRock capture those assets without fighting back.

The MSBT filing puts Morgan Stanley alongside a crowded Bitcoin ETF field. BlackRock's IBIT, Fidelity's FBTC, and ARK's ARKB have collectively accumulated tens of billions in assets under management since spot ETF approval in January 2024. Morgan Stanley's wealth management arm controls roughly $6 trillion in client assets. Even a 1% allocation to Bitcoin across that base would be $60 billion in inflows. That is the number that makes MSBT significant regardless of the $1 million seed funding.

Separately, Senate negotiations on the Crypto Clarity Act - the omnibus market structure bill that has been stuck in committee for months - appear to have broken through a key stalemate. Senators reached a compromise on the yield provisions, specifically around whether and how stablecoins that pay yield should be classified. This had been a blocking issue: DeFi proponents argued that yield-bearing stablecoins are fundamental to the ecosystem; banking regulators argued they are unregistered securities. The compromise language, according to CoinDesk's reporting on March 20, clears the path for the bill to advance to a floor vote.

A crypto market structure bill passing in 2026 would represent the most significant US regulatory development for the industry since ETF approval. It would provide legal clarity for spot token listings, derivatives products, custody requirements, and the definition of when a token is a security versus a commodity. For Coinbase, which faces ongoing regulatory uncertainty about which tokens it can legally offer, this is potentially transformative. The company has spent hundreds of millions in legal fees defending its listing decisions. A clear framework removes that existential risk.

The combination of Morgan Stanley entering the ETF space and Congress nearing a legislative deal represents two separate vectors of institutional legitimacy arriving simultaneously. In a different macro environment - no Iran war, no rate hike speculation, no bond carnage - these developments would be driving prices higher. The fact that Bitcoin is "only" holding $70,000 amid this backdrop says something important about how heavy the macro headwind actually is.

What Comes Next: Three Scenarios for the Next 30 Days

Markets are being pulled in three directions simultaneously. Oil, rates, and geopolitics are all live variables with binary outcomes. Here is what the next 30 days look like across three scenarios:

Scenario 1: Oil Stays Below $100, Fed Stays Put (Probability: ~40%)

The US releases sanctioned Iranian crude into the market. Oil stabilizes in the $90-$97 range. February inflation data (already at 2.4%) does not get meaningfully worse before the April 29-30 FOMC meeting. The Fed holds rates at current levels and signals patience. Equities stabilize. Bitcoin rallies on the institutional infrastructure news - MSBT, the Crypto Clarity Act, Coinbase's expansion - and tests $75,000-$78,000. Altcoin season resumes with QNT, FET, and DeFi leaders leading.

Scenario 2: Oil Spikes, April Hike Gets Priced at 30%+ (Probability: ~35%)

Iranian production does not return to market. OPEC+ holds cuts. WTI retests $100-$108. March CPI data (published April 10) comes in above 3% headline. CME FedWatch April hike probability surges past 30%. Equity markets accelerate their decline - S&P 500 drops below correction territory at -10% from peak. Bitcoin tests the $68,500 liquidation level, triggers a cascade, and probes $64,000-$65,000 before finding institutional ETF bid. Gold likely rebounds in this scenario as a true safe haven once the "everything sells" panic phase passes.

Scenario 3: Ceasefire / De-escalation Surprise (Probability: ~25%)

Diplomatic breakthrough in Iran talks - back-channel negotiations through Oman or Qatar produce a preliminary ceasefire framework. Oil crashes from $96 to $78 in 48 hours. Bond yields retreat 20-30 basis points. Rate hike probability collapses back to 0%. Risk assets explode higher. Bitcoin gaps above $77,000, equities stage a sharp relief rally. This is the fat-tail upside scenario that the defensive derivatives positioning is currently underpriced for. If it happens, the move will be violent and fast.

Key Dates to Watch - Next 30 Days

- March 28: US Q4 2025 GDP final revision

- April 10: US CPI for March - the inflation print that sets April FOMC tone

- April 29-30: Federal Reserve FOMC meeting - hike, hold, or cut?

- April TBD: Crypto Clarity Act Senate floor vote (if compromise holds)

- Ongoing: Iran war updates - any ceasefire signal will move markets 5%+ instantly

- Ongoing: Oil price action - $100 is the psychological trigger for renewed panic

The Coinbase "Everything Exchange" push is a multi-year strategy, not a week-long trade. But it launches into a macro environment that is genuinely hostile. High rates hurt leveraged speculation. Oil-driven inflation kills consumer spending. Geopolitical uncertainty kills institutional risk appetite. The structural bull case for crypto - regulatory clarity, institutional adoption, ETF flows, exchange expansion - is intact. The near-term trading environment is one of the most dangerous in recent memory.

Bitcoin holding $70,000 while gold crashes 19% from peak, stocks drop 5%+ in a month, and bonds sell off globally is either a sign of remarkable resilience or a sign that the crypto correction simply has not happened yet. The derivatives market is paying premium to hedge for the second interpretation. The institutional pipeline is building for the first. Both are simultaneously true. That is the market you are trading in right now.

Watch the $68,500 level. Watch April 10 CPI. Watch oil at $100. Three variables. Three tripwires. Any one of them fires and the other two follow.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram