BlackRock's ETHB Goes Live: Staked ETH ETF Hits Nasdaq as $100 Oil Hammers Traditional Markets

The world's largest asset manager just made a $130 billion bet look like a warm-up act. BlackRock's iShares Staked Ethereum Trust - ticker ETHB - began trading on Nasdaq Thursday morning, quietly doing something no mainstream ETF product has done before: delivering on-chain staking yield through a brokerage account. Meanwhile, Brent crude briefly crossed $100 for the second time this week, the S&P 500 dropped another 1%, and Bitcoin sat at $69,400 outperforming everything. This is what institutional crypto adoption looks like during a war economy.

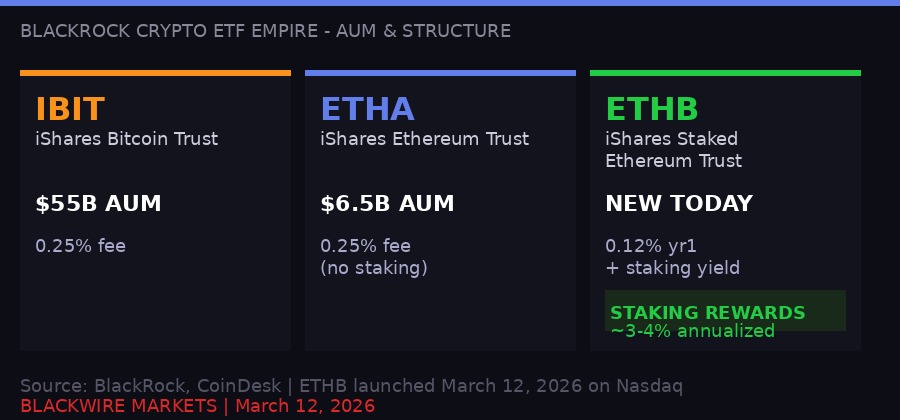

BlackRock's iShares Staked Ethereum Trust (ETHB) launched on Nasdaq March 12, 2026, marking the firm's third crypto ETF and first staking product. [BLACKWIRE / PIL]

The Launch: ETHB Opens on Nasdaq at 9:30 AM Eastern

At the opening bell on Thursday, a ticker appeared on Nasdaq that would have been fantasy three years ago: ETHB. BlackRock's iShares Staked Ethereum Trust began trading with a 0.25% sponsor fee structure - though the firm is waiving half that cost, cutting it to 0.12% on the first $2.5 billion in assets for the first year. That fee waiver is not generosity. It is a deliberate play to capture early AUM and set the standard before competitors can entrench.

The product works exactly how it sounds. ETHB holds spot Ether on the Ethereum network, stakes a portion of those holdings to validate transactions and secure the proof-of-stake chain, and passes staking rewards back to ETF shareholders. The net effect: investors get price exposure to ETH plus an annualized yield component. Current Ethereum staking rewards run roughly 3 to 4 percent annually, though this fluctuates with network activity and validator count.

This is BlackRock's third crypto ETF product. The firm launched IBIT - the iShares Bitcoin Trust - in January 2024 alongside other spot BTC ETF competitors. IBIT now holds more than $55 billion in assets, capturing roughly 95% of all digital asset ETP inflows in 2025 according to BlackRock's own figures. The iShares Ethereum Trust (ETHA), launched later, sits at approximately $6.5 billion - smaller, but not because of lack of demand. Crypto-native ETH holders who were already staking their coins on-chain simply had no reason to move assets into a product that stripped the yield out. ETHB exists specifically to close that gap.

"Some investors who already hold ether directly were staking it and weren't ready to move into an exchange-traded product because they would lose that feature. By incorporating staking, the ETF allows investors to keep the benefits of staking while gaining the operational advantages of an ETF structure."

The operational advantages Jacobs references are real and significant. Institutional-grade custody, brokerage account integration, standard portfolio allocation alongside equities and bonds - these are not trivial. For a family office running a diversified book, buying ETHB through their existing brokerage is vastly simpler than self-custody on the Ethereum network, managing validator keys, and dealing with withdrawal queues. The risk profile changes entirely when BlackRock's custodial infrastructure sits between the investor and the blockchain.

The product will compete directly with Grayscale's staked ETH offerings and any forthcoming staking-integrated products from Fidelity, Franklin Templeton, and other players who entered the ETF race last cycle. BlackRock's brand and distribution network give ETHB a structural advantage, but the staking ETF segment is about to get crowded fast.

BlackRock's three crypto ETF products - IBIT, ETHA, and new ETHB - with AUM and fee structures. [BLACKWIRE / PIL]

Why Staking Yield Rewrites the Institutional Calculus

To understand why ETHB matters beyond the headline, you need to understand how institutional capital evaluates alternative assets. Most traditional portfolio managers - the kind running pension funds, sovereign wealth allocations, and endowments - don't just buy exposure. They buy cash flows. They model income. They run discounted cash flow analyses. A pure price-appreciation asset like non-staked ETH sits awkwardly in those models because it generates nothing until you sell.

Staking changes that equation completely. Ethereum's proof-of-stake mechanism means holding ETH and participating in network validation generates a yield-like income stream. Validators receive newly issued ETH as rewards for correctly attesting to blocks, plus a share of transaction priority fees. That income is real, quantifiable, and recurring - something a portfolio model can actually work with.

Jay Jacobs of BlackRock put it plainly: "For some institutions, when they evaluate an investment, they want to think about it from a cash flow perspective." Staking rewards make Ether more comparable to a dividend-paying equity or a bond with a coupon - not perfectly, because the yield varies with network conditions, but structurally similar enough that it fits into allocation frameworks that pure spot ETH never could.

The cash-flow angle also addresses a core objection that traditional finance has used to dismiss crypto for years: that digital assets are purely speculative vehicles with no intrinsic return profile. A staked ETH ETF doesn't fully silence that objection, but it complicates it. When the world's largest asset manager packages blockchain staking yield in a brokerage-accessible wrapper and charges institutional custody fees, that's a statement about the product's legitimacy as an asset class component.

Grayscale launched its own staking-integrated ETH product earlier this year, and other asset managers have been moving in the same direction. The difference with BlackRock is scale and distribution. When IBIT launched in January 2024, it pulled in more money faster than any ETF in history. There is no reason to expect ETHB's trajectory will be different once institutional allocators get their compliance sign-offs.

For Ethereum's underlying economics, meaningful inflows into ETHB have a compounding effect. Every ETH staked by the ETF is ETH removed from active circulation and locked into the validator queue. As staking participation increases, the yield per validator decreases slightly, but network security increases. For long-term ETH bulls, an institutional product that permanently removes supply while paying participating investors to do so is structurally bullish in ways that pure spot buying is not.

BlackRock's Crypto Empire: $130 Billion and Counting

The ETHB launch doesn't happen in a vacuum. It is the third rung of a rapidly constructed crypto empire that BlackRock has built methodically since spot Bitcoin ETF approval in January 2024. The numbers are worth sitting with: IBIT managing over $55 billion. ETHA at $6.5 billion. Plus roughly $130 billion across the full suite of crypto-related exchange-traded products, tokenized liquidity funds, and stablecoin reserve management according to the firm's own figures.

That $130 billion figure includes BlackRock's BUIDL fund - its tokenized money market fund built on Ethereum - which has become one of the largest tokenized real-world asset products in the market. BlackRock is not dabbling in crypto. It is building parallel infrastructure across multiple asset types, spanning spot ETFs, tokenized traditional assets, and stablecoin reserves. ETHB is the latest piece of an architecture that becomes clearer with each new product.

BlackRock Crypto Products - Snapshot March 12, 2026

Source: BlackRock / CoinDesk interview, Jay Jacobs, March 12, 2026

Jacobs' comment about typical institutional allocations is perhaps the most telling signal in the entire interview. When he says institutions are typically allocating in the "low single digits," often around 1 to 2 percent, and that at those levels crypto risk is comparable to large-cap tech stock exposure within diversified portfolios - he is reframing the entire risk conversation. He is saying that not owning Bitcoin or ETH is its own tracking error relative to what the market now considers a standard allocation.

That reframing, coming from BlackRock with $10 trillion in total assets under management, carries weight that no crypto-native advocate can match. When Larry Fink's firm says digital assets belong in portfolios, compliance officers at state pension funds start returning emails from crypto custody providers. This is how the institutional adoption wave actually works - not through belief, but through distribution and brand authority.

The fee structure tells its own story. IBIT launched at 0.25% with a temporary waiver. ETHA followed the same playbook. ETHB is doing the same: 0.12% waived on the first $2.5 billion for year one, then back to 0.25%. That $2.5 billion threshold is not arbitrary. It is roughly the AUM level where the product's fixed infrastructure costs become profitable at 0.25%. BlackRock is subsidizing early adopters to get to breakeven faster, knowing that ETF AUM compounds as performance attractsflows.

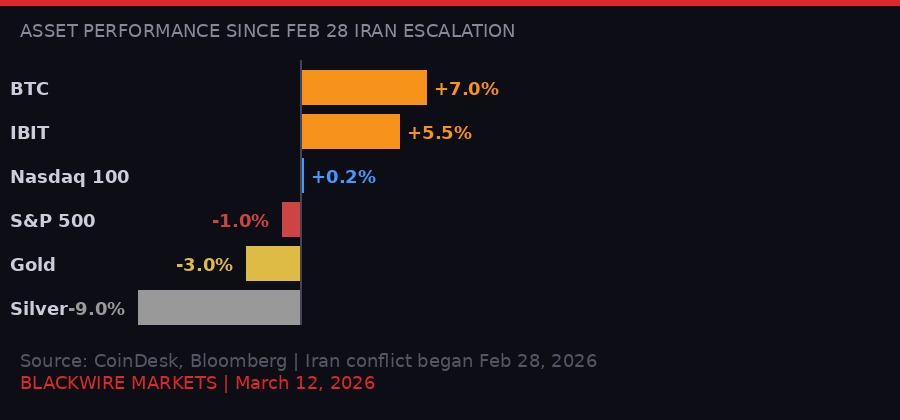

Bitcoin at $70K While Everything Else Burns: The Iran War Trade

ETHB launched into a macro environment that would have been considered extreme even six months ago. Brent crude briefly crossed $100 per barrel Thursday - the second time this month - as Operation Epic Fury against Iran's military infrastructure continues to reshape global energy markets. The VIX, Wall Street's fear gauge, jumped to 25 this week, its highest reading in over a year. The S&P 500 is down roughly 1% since the Iran conflict escalated on February 28. Gold has slipped 3%. Silver is down nearly 9%.

Bitcoin is up 7% in the same period.

That is not a small divergence. It is a regime change in how institutional capital treats digital assets during geopolitical stress. The pattern that played out through two years of Ukraine war - crypto sold off alongside risk assets whenever geopolitical fear spiked - is not repeating. Bitcoin is behaving more like a non-correlated alternative store of value, outperforming the safe-haven assets that are supposed to do this job during wars.

Asset performance since Iran conflict escalation Feb 28, 2026. Bitcoin +7% while gold lost 3%, silver lost 9%, and S&P 500 fell 1%. [BLACKWIRE / PIL, data via CoinDesk/Bloomberg]

The oil-Bitcoin relationship is getting particular attention from researchers. Luxor Technology, a mining analytics firm, published analysis Thursday estimating that only 8 to 10 percent of global Bitcoin hashrate operates in electricity markets that are directly linked to crude prices - primarily Gulf countries like the UAE and Oman. That means $100 oil does not translate to a meaningful mining cost shock for most of the network. The impact runs through Bitcoin's price, not its production cost.

That matters because it explains why Bitcoin can outperform even while the war that is driving oil to $100 should theoretically be bearish for everything. Higher oil prices hit energy-intensive mining in Gulf markets at the margin, but 90-plus percent of the network's hashrate sits in regions where electricity pricing is decoupled from crude. The economic pressure on miners is secondary to the market signal that Brent at $100 sends about dollar purchasing power, supply chain disruption, and inflation expectations - all of which have historically been bullish for fixed-supply assets.

President Trump said Thursday that stopping Iran is "more of a concern than oil prices" - a statement that signals the military campaign has no near-term offramp. Crude climbing 10% on Thursday alone. For traditional portfolio managers watching their energy cost assumptions blow through the ceiling while Bitcoin sits at $70K, the quarterly reallocation arguments in favor of digital assets write themselves.

BlackRock's IBIT traded 1% higher on Wednesday even as all major US equity benchmarks - S&P 500, Nasdaq 100, Russell 2000, Dow Jones - closed in the red. That divergence was noted by multiple trading desks according to CoinDesk reporting. Institutions are not rebalancing out of Bitcoin on the war news. The opposite is happening. Big traders are using privately negotiated transactions - OTC block trades - to accumulate while retail sentiment sits at extreme fear.

The Derivatives Warning: Futures 5x Spot, Bears Stacking Bets

The institutional demand narrative has a complication that needs to be stated clearly: the derivatives market is sending different signals than the spot market. CryptoQuant data shows the futures-to-spot volume ratio on Binance has climbed to approximately 5.1 - its highest level since mid-2023. Bitcoin futures trading is now five times larger than spot volume on the world's biggest crypto exchange.

When derivatives dominate at this scale, price discovery shifts from outright buy-and-sell to leveraged positioning. The result is a market that can generate outsized moves in either direction before snapping back to where it started - which is roughly what Bitcoin has done for the past month. The $74,000 high hit on war-week, the subsequent pullback to $69,400, the oscillation around $70K - all consistent with a derivatives-heavy tape where the underlying trend is unclear.

Annualized funding rates for Bitcoin perpetual futures have been negative since early March. Negative funding means shorts are paying longs to hold their positions - a technical signal that the market is positioned defensively, betting against price appreciation. This marks the longest stretch of negative funding since April 2025, when Bitcoin ultimately bottomed around $76,000 before the next leg higher.

Santiment data from earlier this month showed whales sold 66% of their war-week accumulation into the $74,000 rally while retail bought the dip below $70,000.

CryptoQuant's apparent demand metric is negative at -30,800 BTC on a 30-day basis. That means more Bitcoin is being moved out of active trading environments than is being brought in. Supply in loss - the share of the network's supply that is currently underwater relative to its acquisition cost - is climbing toward levels that have historically preceded extended downturns rather than signaling market bottoms.

These metrics sit in uncomfortable tension with the BlackRock story and the Bitcoin-outperforms-gold narrative. The institutional OTC accumulation may be real. The war-hedge thesis may be playing out. But the derivatives overlay shows a market that is deeply uncertain, where the smart money is not making directional bets with conviction, but hedging, basis-trading, and positioning for volatility rather than direction.

The 5:1 futures-to-spot ratio also increases the market's sensitivity to liquidation cascades. If Bitcoin breaks decisively below $68,000 - which would trigger significant short-side profit-taking and force underwater longs to exit - the cascade dynamics in a 5x derivatives-dominant market could be severe. The wall of worry that Bitcoin is climbing is real. So is the potential drop on the other side.

Senate's 89-10 CBDC Vote: The Policy Wave That Crypto Has Been Waiting For

Beyond the BlackRock launch and the macro noise, Thursday produced a significant policy development that will shape the digital asset landscape for years. The U.S. Senate voted 89-10 to pass the 21st Century ROAD to Housing Act - and buried in the final pages of the 302-page bill is a hard ban on U.S. central bank digital currencies until at least the end of 2030.

The Federal Reserve would be explicitly prohibited from issuing or creating "a central bank digital currency or any digital asset that is substantially similar to a central bank digital currency directly or indirectly through a financial institution or other intermediary." That language is broad by design. It covers not just a direct Fed digital dollar but also any proxy-issued CBDC routed through banks.

The 89-10 vote margin is striking. That is not a partisan knife-fight. That is near-consensus, with Republican opposition to CBDCs picking up enough Democratic votes to hit supermajority territory. Digital Chamber CEO Cody Carbone framed it as a financial privacy issue: "Financial privacy is a cornerstone of American freedom, and any decision to authorize a Central Bank Digital Currency must remain with Congress and the American people."

The bill's path from here is complicated. House lawmakers have signaled they may push back on provisions that limit large private equity firms' residential property holdings - a separate, unrelated section that is effectively the Senate's quid pro quo for getting housing reform done. Trump has also stated he won't sign anything until Congress delivers voter ID legislation. The CBDC ban may be politically popular, but it is riding a legislative vehicle that faces headwinds.

Separately, the CFTC - which once litigated aggressively against prediction market platforms - issued a new policy advisory Thursday and opened a formal rulemaking process for prediction market oversight. The agency under Chairman Mike Selig is completing a 180-degree turn from its previous posture, now framing itself as a champion of these platforms. The practical implication: prediction markets can operate with clearer regulatory guidance, opening the door for institutional participation and larger contract sizes.

These two policy moves - the CBDC ban and the CFTC pivot - are not unrelated to the ETHB launch. They are part of the same wave. The U.S. government is, in fits and starts, clearing the regulatory runway for private-sector digital assets while formally closing off the path to government-issued competitors. That is the landscape BlackRock is building into, and it is considerably more favorable than anything that existed three years ago.

The ETF Arms Race: What Comes After ETHB

The staked ETH ETF is not the end state. It is a checkpoint on a trajectory that moves fast. Here is where the market goes from here.

First, every major ETF issuer with crypto products will now need a staking version. Fidelity, Franklin Templeton, VanEck, Invesco, and others all have spot Ethereum ETFs. All of them will face client pressure to offer staking yield. The fee war that played out in the Bitcoin ETF segment - with expense ratios compressed to near zero as issuers competed for early AUM - will repeat in staked ETH. ETHB's 0.12% year-one rate may look expensive by mid-year.

Second, the staking ETF model will be applied to other proof-of-stake networks. Solana, Avalanche, and Cosmos all have meaningful staking yields. Once the SEC's comfort level with staking-in-an-ETF is established by ETHB's precedent, applications for staked Solana ETFs and others will move from speculative to active. The Solana spot ETF applications are already in play - adding staking is the natural next step.

Third, Strategy (formerly MicroStrategy) continues its aggressive Bitcoin accumulation regardless of what the ETF market does. Thursday's data suggests Saylor's STRC vehicle purchased an estimated 7,000 bitcoin this week, adding to the firm's already massive treasury position. Strategy operates as a leveraged Bitcoin vehicle in equity form - a different product than an ETF but competing for the same institutional dollar that wants BTC exposure without self-custody. The institutional crypto product landscape is diversifying in both structure and issuer.

Fourth, the Vitalik Buterin angle. Ethereum's creator said this week that Ethereum should function as a "simple digital bulletin board" - a minimalist vision of the base layer that prioritizes security and decentralization over feature richness, with complex functionality pushed to layer-two networks. For ETHB, this matters because the simplicity argument strengthens Ethereum's credibility as institutional infrastructure. A base layer that does one thing well - censorship-resistant, programmable settlement - is easier to sell to compliance officers than a complex smart contract platform with hundreds of moving parts.

Fifth, the Circle/USDC story intersects here in ways that deserve attention. Analysts at William Blair noted Thursday that Circle's recent stock rally reflects more than macro factors - they specifically called out USDC's resilience and growing recognition of the firm's stablecoin infrastructure advantage. USDC is the stablecoin of institutional choice, and it runs primarily on Ethereum. Every dollar of institutional capital flowing into Ethereum-based products - ETFs, stablecoins, tokenized assets - is a vote for Ethereum's continued dominance as the institutional blockchain layer.

The compound thesis: BlackRock's ETHB channels institutional capital into staked ETH. Staking removes ETH from circulation and increases network security. USDC and tokenized RWAs built on Ethereum drive on-chain activity. Activity generates fee revenue for validators. Validators include ETHB's staking infrastructure, boosting ETH yield for ETHB holders. The loop compounds. The only question is the rate of institutional inflow.

The macro backdrop cuts both ways. A war economy with oil at $100 and the VIX at 25 is not a comfortable environment for any risk asset. Bitcoin's resilience since February 28 is real, but the derivatives data showing a 5:1 futures-to-spot ratio, negative funding rates, and -30,800 BTC in apparent demand is a genuine warning sign. The market is fragile under the surface, held together by OTC institutional demand that is not fully transparent.

If crude pushes toward $120 and the Federal Reserve signals it cannot cut rates due to inflationary pressure from energy costs - the stagflation scenario that markets are increasingly pricing - the playbook for crypto gets complicated. Bitcoin benefits from inflation expectations up to a point, but a severe recession driven by energy shock historically hits all risk assets, crypto included. The bears in the perpetual futures market may be early, but they are not obviously wrong.

What Thursday's ETHB launch proves is that BlackRock is not waiting to find out. The firm is building product regardless of short-term macro conditions, betting that the 10-year institutional adoption arc is more important than the next quarter's price action. With $130 billion already deployed across crypto infrastructure and ETHB giving institutional money managers a new reason to allocate to ETH, the long-term direction of capital flows is clear even if the short-term price path is not.

The staked ETH ETF was inevitable. It just needed someone with BlackRock's regulatory relationships, distribution network, and balance sheet to make it happen. They did. Everything that comes after - the fee wars, the competing products, the expanding asset class, the policy tailwinds - is downstream of what started at 9:30 AM Thursday on Nasdaq.

This is still early days for digital asset ETF adoption, as Jay Jacobs noted. But "early days" looks very different when the world's largest asset manager has $130 billion on the table and just launched its third product. The days are not as early as they used to be.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram