Markets

Bitcoin's $13.5B Quarterly Options Expiry Hits Today: Max Pain $75K, Markets Already Cracking

The largest quarterly options settlement in months lands today on Deribit. Max pain is $75,000. Bitcoin is $5,000 below that, bond markets are in their worst selloff since 2008, and rate hike bets just went from 0% to 12% in one week. What happens next matters.

$13.5 billion in Bitcoin options settle today on Deribit, the most significant quarterly expiry during the Iran war period. (Pexels)

Today is settlement day. Roughly $13.5 billion in Bitcoin options contracts expire on Deribit - the world's largest crypto options exchange - and the setup going into expiry is about as complicated as it gets. Bitcoin trades near $70,700. Max pain, the price at which the most contracts expire worthless and market makers lose the least, sits at $75,000. That's a $4,300 gap. And the macro backdrop is anything but calm.

Oil up 50% since the Iran war started. Bond markets in a global freefall. Rate hike probability that was 0% seven days ago now sitting at 12% for April. Gold - which was supposed to be the safe haven - has crashed 18% from its peak. And in the middle of this wreckage, Bitcoin is holding $70,000 and outperforming nearly everything in sight.

Today's expiry is the quarterly settlement, meaning it's the big one that institutional desks have been positioning around for weeks. The term structure is in backwardation. The options skew has exploded. And $596 million sits in $20,000 put options - a position that only pays out if Bitcoin collapses 70% from here. This is not a normal Friday expiry. This is the options market trying to price an unpriced world.

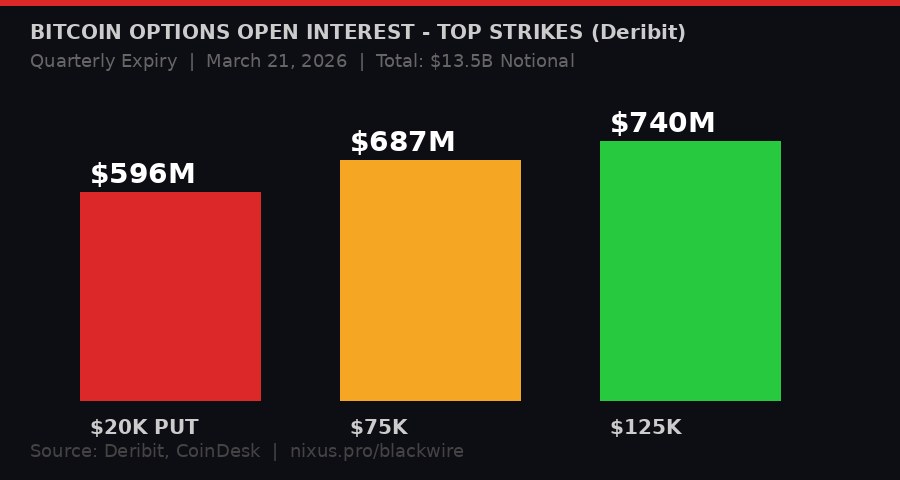

Top three Bitcoin option strikes heading into today's quarterly expiry. The $75K call and $125K call dominate, but $596M in $20K puts signals significant tail-risk hedging. Source: Deribit / CoinDesk.

Inside the $13.5 Billion: How the Positions Break Down

The quarterly expiry structure reveals bifurcated market expectations - massive upside bets at $125K alongside significant crash hedges at $20K. (Pexels)

The structure of this expiry is worth unpacking because it tells you exactly how traders read the current situation. According to Deribit statistics, total open interest stands at 195,719 BTC, split between 120,236 BTC in calls and 75,482 BTC in puts. That gives a put-call ratio of 0.63 - technically bullish, meaning more participants hold upside bets than downside protection.

But the devil is in the strikes. Three positions dominate. The $125,000 call has $740 million in notional value - these are traders betting Bitcoin doubles by year-end. The $75,000 strike has $687 million - these are more near-term conviction plays, or hedge positions for existing holdings. And then there's the one that stands out: $596 million in $20,000 puts, making it the third-largest strike on the entire board.

The $20,000 put is deep out of the money. With Bitcoin at $70,700, it only pays if BTC falls 72% from current levels. That is not a trading position - it is insurance against catastrophe. Per CoinDesk's March 19 analysis, much of this activity is likely driven by traders selling these far-OTM puts to collect premium, not buying them outright as crash hedges. The low probability of a $20K print means these contracts pay out a steady income stream as long as the world doesn't end.

Still, the $596 million figure tells you something: options desks are pricing tail risk they haven't priced in years. The Iran war, combined with bond market dislocations and oil shock, has resurrected scenarios that were theoretical noise six months ago.

Deribit Quarterly Expiry - Key Numbers

- Total Notional: $13.5 billion

- Total Open Interest: 195,719 BTC

- Calls: 120,236 BTC | Puts: 75,482 BTC

- Put-Call Ratio: 0.63 (net bullish)

- Max Pain Level: $75,000

- Top Strike (calls): $125,000 - $740M notional

- Second Strike: $75,000 - $687M notional

- Third Strike (puts): $20,000 - $596M notional

- Current BTC Price: ~$70,700

- Source: Deribit, CoinDesk (March 19, 2026)

The max pain analysis is worth watching through today's session. Max pain acts as a gravitational pull - market makers who sold options have to hedge their exposure, which can create buying or selling pressure that drags price toward the level where most contracts expire worthless. At $75,000, that's about 6% above current prices. A drift higher into the close would benefit market makers. It would also reset the psychological level that Bitcoin has been struggling to hold above since the Iran war began.

Derivatives Dashboard: Backwardation, Liquidations, and the 14% Skew

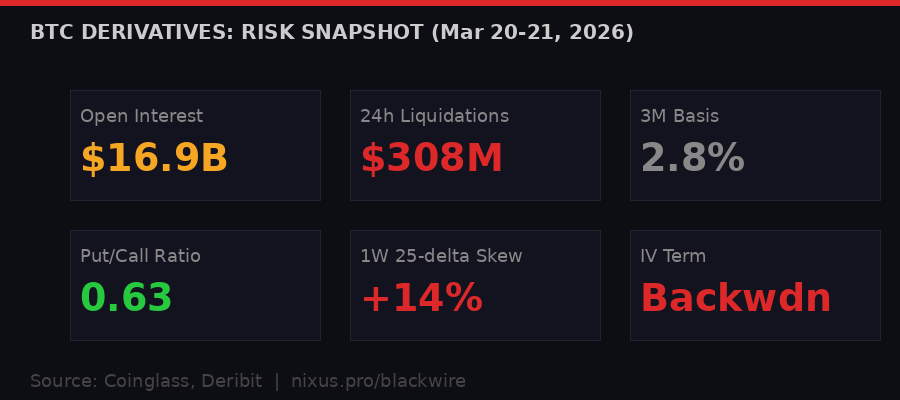

Real-time derivatives snapshot. The implied volatility term structure in backwardation signals traders pricing an immediate shock event. Source: Coinglass, Deribit.

The derivatives data from Thursday's session tells a precise story. Open interest stabilized at $16.9 billion, close to the $17 billion level from the prior week. Funding rates have returned to neutral territory - 0% to 10% across major platforms - after briefly going negative earlier in the week. Negative funding is significant: it means traders were paying short-holders to stay short, which typically indicates capitulation and can fuel a short squeeze.

The three-month annualized basis sitting at 2.8% is the key number for institutional positioning. Basis is the spread between futures price and spot price. At 2.8%, it is historically compressed - annualized basis typically runs 10-15% in bull markets. The message: institutional traders are not pricing a near-term rip. They are hedging defensively, leaning on flat to mildly bullish directional exposure rather than leveraged longs.

The options market paints the sharpest picture. The 24-hour call-to-put volume split has shifted to 43/56 - that's a majority of recent volume going into puts, which signals active demand for downside protection rather than directional calls. The one-week 25-delta skew has moved to 14% from 9% - this measures how much more expensive puts are relative to calls of equivalent delta. A jump of five percentage points in one week is sharp.

"The implied volatility term structure confirms a sharp front-end spike into backwardation, a signal that traders are bracing for an immediate, high-impact volatility event, prioritizing short-term hedging over stable mid-term growth expectations." - CoinDesk Markets, March 20, 2026

Backwardation in the IV term structure is rare and telling. Normally, uncertainty about the distant future makes long-dated options more expensive than near-term ones. When that flips - when short-dated IV is more expensive than long-dated IV - it means traders believe the near-term holds more danger than any distant scenario. They are not scared of 2027. They are scared of the next two weeks.

Friday's liquidation data backs this up. Coinglass recorded $308 million in 24-hour liquidations with a 63-37 split between longs and shorts. Bitcoin accounted for $93 million, Ethereum $81 million, with others making up the remaining $134 million. That's a longs-heavy bleed - not a catastrophic flush, but steady attrition on leveraged bulls. The $68,500 level is the key liquidation cluster on the Binance heatmap. Any move below that zone risks triggering a cascade.

The Macro Wrecking Ball: Bonds, Oil, Gold, and the Rate Hike Nobody Saw Coming

The Federal Reserve, which was expected to cut rates three times in 2026, is now facing a 12% probability of hiking in April after oil prices surged 50% post-Iran. (Pexels)

Six weeks ago, CME FedWatch showed zero probability of a rate hike at the April FOMC meeting. The consensus was debating whether the Fed would cut two times or three times in 2026. Today, according to CME FedWatch, the probability of a rate hike in April has risen to 12%. That is a seismic repricing of monetary policy expectations in roughly seven days.

The trigger is oil. Since the Iran conflict began in late February, crude has surged approximately 50%. Oil at $96 a barrel - briefly cresting above $100 before the U.S. floated releasing sanctioned Iranian crude - feeds directly into inflation. February's CPI data, released before the war escalated, already showed annual headline inflation at 2.4% and core at 2.5%. Neither figure includes the energy shock that has been building since late February.

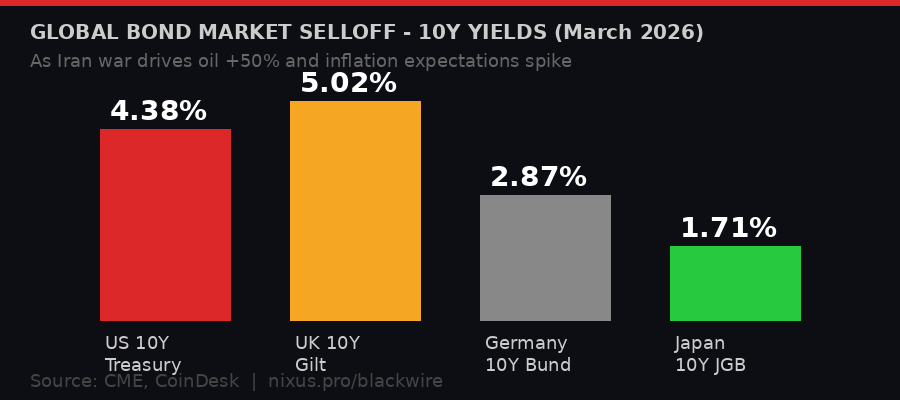

The bond market selloff is global. UK gilts have topped 5% for the first time since 2008. US 10-year Treasuries hit 4.38%. Source: CME, CoinDesk.

The bond markets have priced this faster than equity markets. The US 10-year Treasury note climbed to 4.38% on Friday - up from under 4% at the start of March, a move of nearly 40 basis points in three weeks. In the UK, 10-year gilt yields have cleared 5% for the first time since 2008, a 15% increase in the past month alone. The bond market is screaming stagflation.

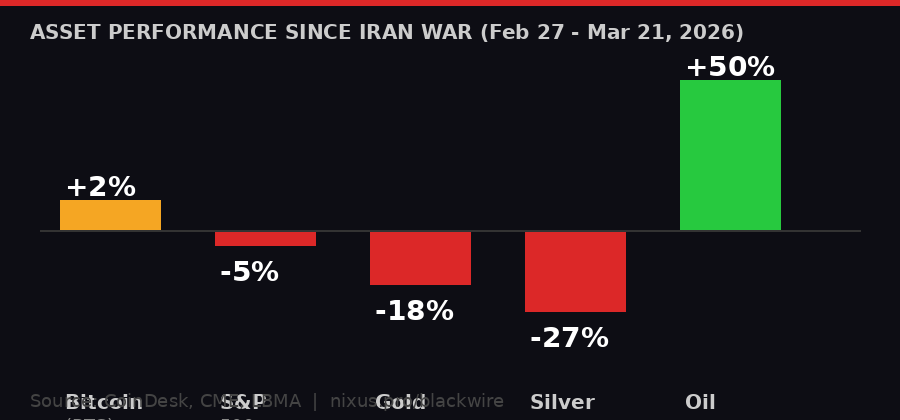

Gold's collapse is the biggest surprise. The metal that ran to nearly $5,600 per ounce in late January - a historically unprecedented figure - has crashed back to $4,569, a decline of roughly 18% from peak. Silver has fared worse, falling from $95 to $69.50 per ounce, a 27% drop. These were the assets that were supposed to benefit from geopolitical fear and inflation. Instead, they've been hit by forced selling as funds unwind positions to cover margin calls elsewhere.

"Bitcoin has once again acted as the canary in the macro coal mine. At current levels, bitcoin is already pricing a recession, while many traditional assets are not." - Andre Dragosch, European Head of Research, Bitwise (via CoinDesk, March 20, 2026)

The S&P 500 is down more than 5% since late February and on track for its fourth straight weekly decline as of Friday. The Nasdaq has dropped similarly. Bitcoin, hovering near $70,000 and up modestly since the start of March, is outperforming both precious metals and equities since the war began. That's the counterintuitive story traders are wrestling with heading into today's expiry.

Bitcoin has outperformed nearly every major asset class since the Iran conflict began. Gold and silver suffered the steepest losses. Oil is the only bigger winner. Source: CoinDesk, LBMA, CME.

Bryan Tan, trader at Wintermute, told CoinDesk on Thursday that the lack of follow-through above $75,000 suggests markets remain cautious and rangebound. His advice: stay flat. "When sentiment swings on each headline about the conflict, and correlation to oil prices are so elevated, being flat is a strong position," he said. "We lean towards reserving dry powder until we see a meaningful confirmation in either direction."

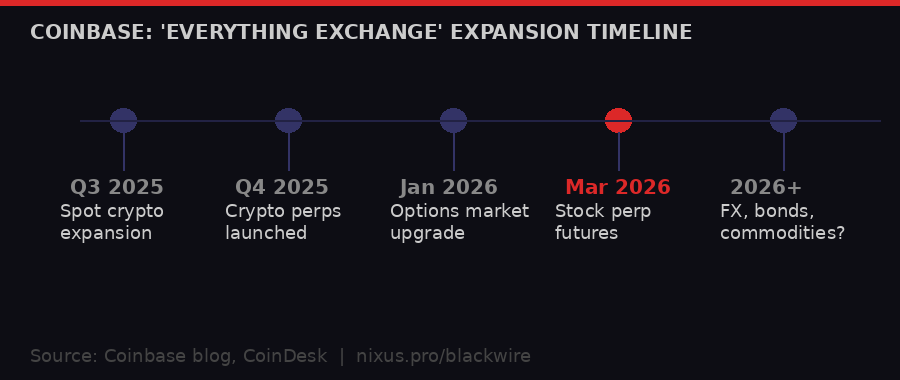

Coinbase Launches Stock Perpetual Futures: The Everything Exchange Strategy Gets Bigger

Coinbase's push into 24/7 stock perpetual futures positions it directly against Hyperliquid and traditional derivatives exchanges. (Pexels)

While the options clock ticked toward today's expiry, Coinbase dropped a major product announcement Friday. The exchange said it has begun offering perpetual stock futures to eligible non-US retail and institutional traders, allowing leveraged positions on the Magnificent 7 - Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta and Tesla - as well as SPY and QQQ ETF-linked contracts.

The mechanics: contracts are cash-settled in USDC (Circle's dollar-pegged stablecoin), trade 24 hours a day seven days a week, and offer up to 10x leverage on single stocks and 20x on ETF products. The exchange uses the same risk engine that supports its crypto derivatives, enabling cross-margining across both crypto and stock perpetual positions. Per Coinbase's official blog post, this is available in eligible international jurisdictions - not available to US customers, where regulatory constraints remain tighter.

Coinbase's product expansion roadmap toward becoming the "Everything Exchange." Stock perps are the latest - commodities and FX could follow. Source: Coinbase blog, CoinDesk.

This is the "Everything Exchange" strategy moving from tagline to product reality. The concept - that a regulated crypto exchange could offer exposure to any asset class through derivatives settled in stablecoins - has been Coinbase's stated direction for the past year. Stock perpetual futures is a direct assault on the offshore derivatives space that Binance, OKX, and Bybit have dominated, and a direct competitive response to Hyperliquid.

Hyperliquid, the decentralized perpetuals platform, launched S&P 500 perpetual futures contracts just days before Coinbase's announcement. The decentralized platform has become a major venue for traditional-asset-linked contracts during the Iran war period, with oil-linked contracts trading round the clock as energy prices swung on conflict headlines. Coinbase is now entering that market with regulatory credibility and institutional infrastructure that pure DeFi platforms cannot match.

The timing is notable. International traders who can't access US stock markets during off-hours have traditionally relied on CME futures or offshore platforms to hedge equity exposure overnight. Coinbase's USDC-settled 24/7 perpetuals offer a regulated, stablecoin-denominated alternative. For traders already holding USDC balances from crypto activities, the friction is essentially zero.

Coinbase Stock Perpetual Futures - Product Specs

- Available Assets: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, Tesla (Mag 7) + SPY, QQQ

- Settlement: Cash-settled in USDC (Circle)

- Trading Hours: 24 hours / 7 days

- Single Stock Leverage: Up to 10x

- ETF Product Leverage: Up to 20x

- Geographic Availability: Eligible non-US customers in supported jurisdictions

- Risk Engine: Shared with Coinbase crypto derivatives (cross-margining)

- Announcement Date: March 20, 2026

- Source: Coinbase blog, CoinDesk

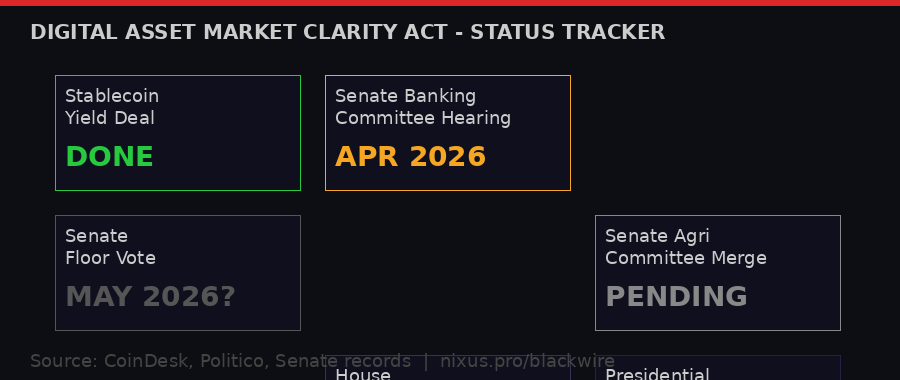

Crypto Clarity Act: Senate Deal Could Unlock Stablecoin Legislation

Senators Tillis and Alsobrooks have agreed "in principle" on stablecoin yield, clearing what had been the biggest legislative roadblock in the Digital Asset Market Clarity Act. (Pexels)

Buried under the options expiry noise, a quietly significant development emerged Friday evening: US Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) announced they have reached an "agreement in principle" on one of the major sticking points in the Digital Asset Market Clarity Act - the question of whether stablecoins can pay yield to holders.

This was the fault line that had gridlocked the bill for months. Banks argued that if stablecoins paid interest or rewards on passive balances, they would function as deposit accounts - and deposit flight from the banking system could undermine lending capacity. The Senate Banking Committee needed both sides to resolve this before moving the bill to a committee hearing.

Per CoinDesk's reporting on March 20, Alsobrooks' communications director confirmed the deal in a statement: "This is an important step forward for market structure legislation, a step that both have worked for months to resolve." The key concession: stablecoin yield will be barred on passive balances. Active yield strategies - DeFi integrations, for example - remain open questions, but the passive-balance prohibition satisfies banking sector concerns.

"Sen. Tillis and I do have an agreement in principle. We've come a long way. And I think what it will do is to allow us to protect innovation, but also gives us the opportunity to prevent widespread deposit flight." - Senator Angela Alsobrooks, Politico, March 20, 2026

The Clarity Act still has significant hurdles. The stablecoin yield deal clears one - but DeFi treatment, ethics provisions, and illicit finance guardrails remain unresolved. Source: CoinDesk, Politico.

The bill's path from here: the agreement "in principle" needs to be circulated among industry stakeholders - crypto firms and banks - with details expected no earlier than Monday. Then a Senate Banking Committee hearing, which Republican Senator Cynthia Lummis said she expected "in the latter half of April." If the committee approves it, the bill still needs to be merged with a similar version that already passed the Senate Agriculture Committee. Then the Senate floor. Then House reconciliation. Then the President.

On timing, industry advocates have targeted May for a Senate resolution. But Senate floor time is constrained, and unrelated items - the Republican voter-ID bill, ongoing Iran war authorization debates - are competing for the calendar. The Clarity Act could slip to summer or fall, particularly if the Agriculture-Banking merge hits turbulence. The stablecoin yield deal matters because it clears the biggest single blockage. But the road to law is still long.

Bank of America's CEO had publicly warned that $6 trillion in deposits could migrate to stablecoins without appropriate guardrails - a figure cited across banking sector testimony and clearly driving the negotiating posture of Democrats on the Banking Committee. The agreement to bar passive-balance yield directly addresses that concern, though banking lobbyists are unlikely to declare full satisfaction until they see actual legislative text.

DeFi Casualty Report: Gauntlet Loses $380M, Venus Protocol Exploited

DeFi's week in damage: Gauntlet lost $380M in TVL as an OKX incentive campaign ended; Venus Protocol suffered an exploit that left bad debt and sent XVS down 9%. (Pexels)

While the macro picture dominated, DeFi had its own turbulent week. Gauntlet, one of the sector's most respected risk management firms - valued at $1 billion in 2022 - saw its total value locked (TVL) crash 22.84% in seven days, dropping from approximately $1.72 billion to $1.325 billion. That's $380 million out the door in a week.

The driver, per Gauntlet and DeFiLlama data, was the end of OKX's pre-deposit campaign on Katana, a DeFi-focused blockchain. Pre-deposit campaigns work like this: OKX incentivizes users to park capital in Gauntlet-managed vaults ahead of a protocol launch, juicing TVL metrics artificially. When the campaign ends, the incentive disappears and capital leaves - often sharply. The chart confirms it: Gauntlet's TVL surged around March 2 and reversed just as steeply when OKX wound down the program around March 19.

Gauntlet's business model is worth understanding because the TVL number can be misleading. The firm doesn't hold the funds - it sets risk parameters for lending markets and vaults. Its TVL is the capital held within systems it governs. An outflow reflects capital leaving its ecosystem, not a breach or loss. Per CoinDesk's reporting, the outflows are "predominantly stablecoin-based" and reflect rotation to higher-yielding alternatives - SOL-based protocols like Jito, for example, currently offer 5.69% APY versus Gauntlet's USDC vault at 4.86%.

Gauntlet noted that deposits are now "back to same levels before the campaign" and said it has "navigated large capital swings before due to incentive campaign endings, airdrops, and shifts in market conditions." The comparison: in October 2025, a single $775 million deposit caused a 40x TVL spike that reversed within ten days.

Separately, Venus Protocol - a BNB Chain lending protocol - suffered an exploit on March 16 that left the protocol with bad debt. The XVS token fell 9% once on-chain analysis revealed major holders moving large amounts to exchanges, suggesting insiders or large accounts exiting ahead of the bad debt becoming public knowledge. Venus has not disclosed the full scale of the damage, and the exploit methodology remains under investigation at time of writing.

DeFi Weekly Damage Report

- Gauntlet TVL: -$380M (-22.84%) over 7 days - OKX campaign end

- Gauntlet Current TVL: $1.325B (down from $1.72B peak)

- Venus Protocol: Exploit on March 16 - bad debt still being quantified

- XVS Token: -9% on exploit revelation / whale exit signals

- Gauntlet USDC Vault APY: 4.86% vs. Jito (SOL) 5.69%

- Source: DeFiLlama, Gauntlet, CoinDesk (March 19-20, 2026)

What Happens Next: Four Scenarios for the Post-Expiry Market

Post-expiry price action could set the tone for the next 4-6 weeks of crypto market direction. The max pain level at $75K is the key magnet. (Pexels)

With $13.5 billion in options settling today, the question isn't just what happened but what comes next. Four scenarios are worth laying out explicitly.

Scenario 1: Max pain gravity wins. Bitcoin drifts toward $75,000 into the settlement, as market makers hedge toward the level where most contracts expire worthless. This is the most orderly outcome. Once expiry clears, the market resets with fresh positioning and could trade either direction. Probability: moderate. This requires macro noise to quiet for a few hours, which it hasn't done consistently.

Scenario 2: Macro overwhelms the pin. A fresh oil spike, an unexpected Fed statement, or a new Iran escalation headlines hit before settlement. The $68,500 Binance liquidation cluster becomes the next test. A flush through that level triggers cascading longs and sends the market below $68,000 before expiry. The $20K put holders don't get rich, but the $75K call buyers take significant losses. Probability: meaningful, given the current news flow rhythm.

Scenario 3: Post-expiry squeeze. Expiry clears relatively quietly near $70,000-$72,000. Short positions built in anticipation of volatility unwind. With funding rates already normalized and open interest stable, a short-covering squeeze to $74,000-$76,000 in the days post-expiry is structurally supported. Bitcoin's relative strength versus gold and equities suggests latent demand. Probability: plausible for the following week, not the day itself.

Scenario 4: April rate hike panic accelerates. If next week's economic data - PCE inflation on Friday March 27, and any fresh Fed communication - reinforces rate hike fears, the 12% April probability in CME FedWatch could double. A 25% probability of a hike would send equities and bonds materially lower, and while Bitcoin has shown resilience, a genuine panic repricing of terminal rates hasn't been tested since 2022's rate shock. This is the scenario that makes those $20K puts look less stupid in hindsight. Probability: low but non-trivial given the oil-driven inflation trajectory.

What this expiry does not resolve: the underlying macro tension between a war-driven oil shock, global bond dislocations, and a Federal Reserve that can't cut when inflation is rising. Those pressures will still be here Monday morning. The options board resets. The war does not.

Bitcoin's outperformance since the Iran conflict began - up modestly while gold lost 18%, the S&P 500 lost 5%, and bonds sold off across every major market - is the real story of the past three weeks. Whether that outperformance is a structural shift in how institutions treat Bitcoin as a macro hedge, or a temporary anomaly driven by crypto-native flows, will only be confirmed if Bitcoin holds above $68,000 through the next wave of macro turbulence. That test may come as early as next week.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram