Bitcoin is holding $69,400 by the skin of its teeth. Gold is collapsing. Oil is approaching $100 per barrel. The Fed just delivered its hawkiest signal in months. Two of Bitcoin's earliest wallets liquidated $117 million in BTC inside 24 hours. A DeFi attacker who spent nine months methodically building a position has extracted at least $3.7 million from Venus Protocol on BNB Chain. And tomorrow morning, $13.5 billion in Bitcoin options expire in the biggest quarterly derivatives event of the year.

Each of these events alone would be significant. Together on a single Thursday, they are a market environment test unlike anything seen since the early weeks of the Iran conflict. Here is everything that happened today, why it happened, and what the options market is saying about where this ends.

BTC -2.6% to $69,400. Gold -5% to $4,500/oz. Silver -6.6%. S&P 500 and Nasdaq both at fresh 2026 lows. XVS (Venus) -9%. Oil near $100/bbl. Two OG wallets dumped 1,650 BTC ($117.87M). Fed held rates at 3.50-3.75%, raised 2026 CPI forecast to 2.7%. Quadruple witching Friday March 20. Venus exploit: $2.15M bad debt from 9-month THE token manipulation.

The Fed's Hawkish Curveball Kills the Rate Cut Dream

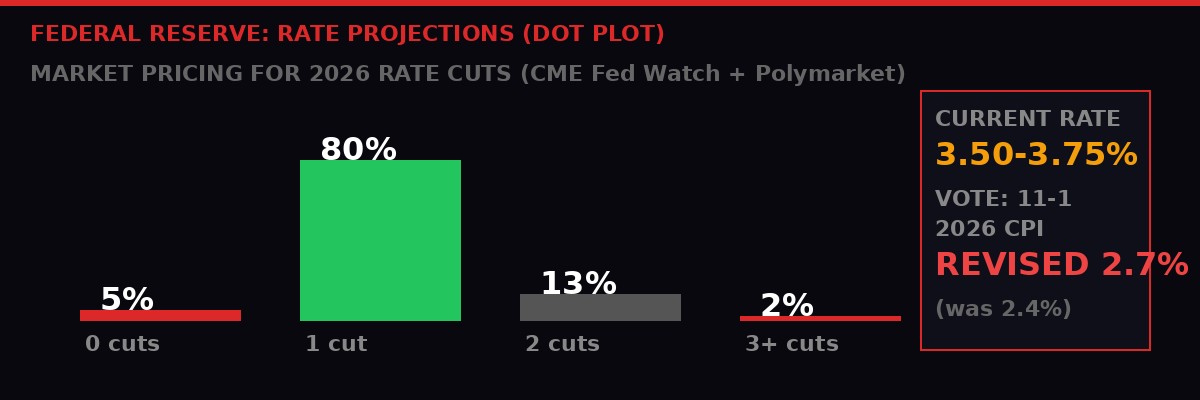

Wednesday's Federal Reserve decision set the fuse for everything that followed on Thursday. The FOMC voted 11-1 to hold the benchmark fed funds rate at 3.50%-3.75%, in line with market expectations. The lone dissenter, Stephen Miran, voted to cut by 25 basis points. What nobody was fully priced for was the accompanying statement and revised economic projections.

The central bank raised its 2026 inflation forecast from 2.4% to 2.7% - a meaningful upward revision that directly acknowledges the oil price shock triggered by the March attack on Iran. The accompanying statement read: "The implications of developments in the Middle East for the U.S. economy are uncertain." That is Fed-speak for: we cannot cut rates while an active war is pushing oil toward $100 per barrel.

The dot plot - the Fed's own projection of where rates are headed - continued showing just one 25-basis-point cut for 2026, and one more in 2027. But the real tell was Chair Powell's personal dot, which moved higher. Only two committee members remained in the two-cut camp. The "higher for longer" narrative that traders spent six months trying to bury is back.

"The higher for longer narrative has been reinvigorated by sticky inflation and the inflationary shadow cast by rising energy costs, forcing investors to abandon their dreams of a rapid easing cycle." - Matt Mena, Crypto Research Strategist, 21Shares

The market response was immediate. Polymarket and CME Fed funds futures now imply roughly an 80% probability of just one rate cut in 2026, compared to a 62% probability of two to three cuts just one month ago. That repricing hit risk assets across the board on Thursday - equities, crypto, and metals all took it on the chin simultaneously, which itself is telling.

The 10-year Treasury yield ticked higher to 4.21%. The S&P 500 and Nasdaq each slid close to 1%, hitting fresh year-to-date lows. The VIX volatility index climbed back above 35, matching the spike seen in the immediate aftermath of the Iran conflict outbreak. That is the highest level in over a year, signaling genuine stress in institutional positioning.

OG Bitcoin Whales Cash Out $117 Million in 24 Hours

The Fed decision gave Bitcoin's oldest holders the exit signal they were apparently waiting for. Blockchain data tracked by Lookonchain shows at least two long-term holders together offloaded over 1,650 BTC worth more than $117.87 million during the early hours of Thursday.

The first wallet - an early adopter who previously held a 5,000 BTC stack - offloaded a full 1,000 BTC, moving approximately $71.3 million in a single transaction. The second, a veteran whale who had previously sold an 11,000-BTC stack earlier in the cycle, added another 650 BTC to his dump. These are not traders. These are original owners from Bitcoin's early years, and they are selling into a falling market.

The timing here is critical. These wallets had survived multiple bear markets, three halving cycles, multiple 70%+ drawdowns. They did not sell at $74,500 last week, or at $75,000 in February, or at the local highs above that. They waited until the Fed signaled that liquidity tightening would last longer than expected, then hit the market simultaneously with $117 million in BTC.

Bitcoin's price dipped nearly 1% to $70,600 in the immediate aftermath of the Lookonchain reports, then continued sliding throughout the day to $69,400 as Iran war headlines around attacks on energy infrastructure drove another round of risk-off selling. From Wednesday's intraday high near $74,500, Bitcoin has now lost approximately 7% in 36 hours.

The broader crypto market tracked the decline. Ether (ETH) fell to $1,890 (-2.8%). Solana (SOL), XRP, and BNB all posted similar losses in the 2-3% range. The CoinDesk 20 Index declined 4.6% in the same 24-hour window. Crypto-linked equities followed: Coinbase (COIN) slipped 1.7%, Strategy (MSTR) fell 2.6%, and Circle (CRCL) pulled back 6%, giving up some of the gains accumulated since its listing surge three weeks ago.

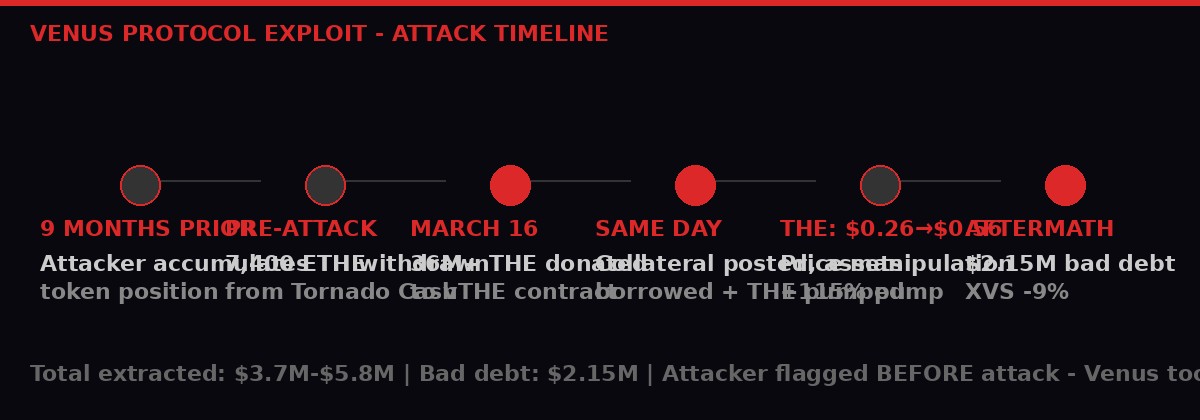

Venus Protocol Exploit: 9 Months of Planning, $2.15M in Damage, XVS -9%

While macro markets were bleeding, the DeFi ecosystem served up its own crisis. The governance token of Venus Protocol (XVS), BNB Chain's largest money market with over $1.4 billion in total value locked, dropped more than 9% in 24 hours after an exploit that has left the protocol with $2.15 million in bad debt - loans the system can no longer recover.

The mechanics of the attack are worth understanding in detail, because this was not a flash-loan exploit or a bug hunt. This was a deliberate, patient, multi-month operation. Venus Protocol's own post-mortem confirms the following sequence:

The attacker began methodically accumulating a large position in Thena's THE token, building quietly over months to avoid triggering price alerts or community attention.

According to PeckShield analysis, the operation was funded with 7,400 ETH withdrawn from Tornado Cash, the mixing protocol. This is a laundering operation that predates the attack by months.

The attacker donated more than 36 million THE tokens directly to the vTHE contract, bypassing normal deposit caps entirely. This donation - rather than a deposit - exploited a code path that skipped cap verification, lifting the market's exchange rate by approximately 3.8 times.

With the inflated collateral value established, the attacker borrowed other assets and used them to buy more THE in a thin, illiquid market. THE price surged from $0.26 to near $0.56 - a 115% pump driven by this manufactured demand.

The attacker sold THE into the inflated price. THE dropped more than 17% in under 24 hours, triggering cascading liquidations. Assets extracted include tokenized Bitcoin, BNB, and stablecoins - estimated at $3.7 million to $5.8 million extracted before liquidations wiped the rest.

Venus confirmed this was not a flash loan attack - its oracles continued functioning normally throughout, and Venus Flux was unaffected. The damage was concentrated in THE and to a lesser extent CAKE. Venus said no user funds were lost outside the affected Thena pools.

"Venus is a decentralized protocol. As a permissionless protocol, we cannot and should not freeze or blacklist addresses based on suspicion alone. This is a tension inherent to DeFi, and one we take seriously." - Venus Protocol, official statement via X

That statement lands like a confession. Because here is what Venus also confirmed: the attacking address had been flagged by community members before the attack occurred. Venus chose not to act because, as the protocol noted, "no rules had been broken, and no exploit had occurred." By the time rules were technically violated, the money was already gone.

This is a systemic DeFi governance problem, not a Venus-specific one. Permissionless protocols by design cannot act on suspicion. But the result is that a well-funded, patient attacker with nine months of runway can operate in plain sight, get flagged, and still extract millions - because the protocol's own rules prevent preemptive action. The governance vote on how to cover the $2.15 million loss from Venus's risk fund is now pending. XVS fell from approximately $8.50 to under $7.80 on the news.

The protocol has since paused THE borrows and withdrawals, cut THE's collateral value to zero, and tightened rules on other markets identified as at-risk. Those include BCH, LTC, AAVE, and others. The attacker's wallet had been identified and flagged. The community spoke. The protocol listened. Too late.

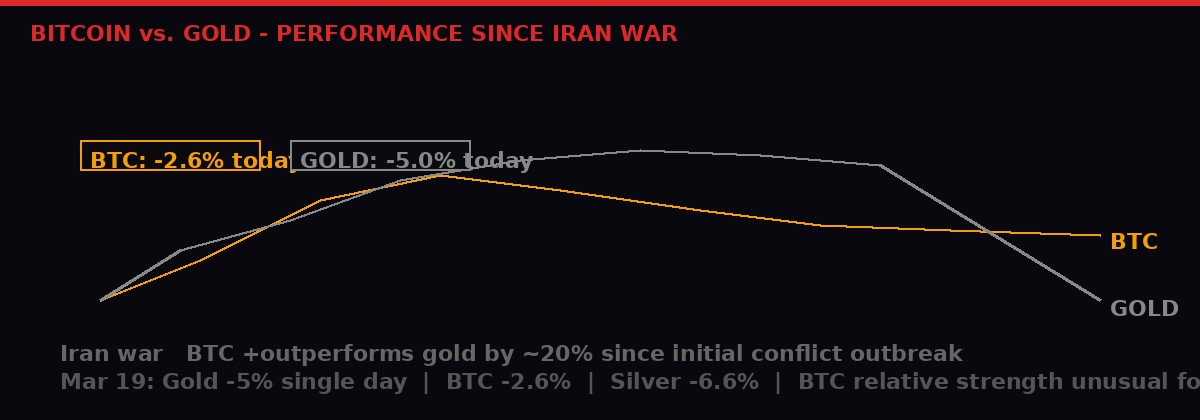

Gold Craters 5%, Silver -6.6%: The Safe Haven Narrative Breaks

One of the most striking data points from Thursday is not Bitcoin's decline - it is gold's. The precious metal dropped 5% to around $4,500 an ounce, its lowest level since early February. Silver fell an even sharper 6.6%. These are supposed to be the assets that benefit from geopolitical uncertainty and inflation fear. Yet on a day with oil nearing $100 and active conflict in Iran, they are being sold off aggressively.

The explanation from analysts is coordinated institutional de-risking. When multiple crisis signals hit simultaneously - oil shock, rate hawkishness, equity volatility - institutional portfolios do not rotate into safe havens. They reduce gross exposure across the board. Margin calls in one asset class force selling in others. The result is simultaneous drawdowns in gold, silver, equities, and crypto.

"Rising energy prices are feeding into inflation expectations, reinforcing a higher-for-longer interest rate outlook and tightening liquidity - a difficult mix for risk assets." - Alvin Kan, COO, Bitget Wallet

What makes the picture unusual is Bitcoin's relative performance. BTC declined roughly 2.6% on Thursday - less than gold, less than silver, less than some equity indices. Since the Iran conflict broke out in March, Bitcoin has outperformed gold by approximately 20%, according to Wintermute trader Bryan Tan. This is genuinely anomalous behavior for an asset the financial industry has spent years categorizing as "high-risk tech-adjacent."

The thesis gaining traction among on-chain researchers is that Bitcoin's institutional base has changed. A larger percentage of BTC is now held by ETFs, long-term treasury firms, and conviction holders who are explicitly not selling in risk-off environments. The OG whale dumps Thursday represent old-money exits, but the structural buyers - BlackRock's IBIT, Fidelity's FBTC, Strategy's 500,000+ BTC stack - are not selling. The supply squeeze beneath the surface may be holding the price more than the charts suggest.

That said, Wintermute's Bryan Tan offered a cautious read: the lack of follow-through above $75,000 despite multiple attempts suggests markets remain rangebound and uncertain. "When sentiment swings on each headline about the conflict, and correlation to oil prices are so elevated, being flat is a strong position," he said. "We lean towards reserving dry powder until we see a meaningful confirmation in either direction or a material change in market conditions."

$13.5B in Bitcoin Options Expire Tomorrow: Quadruple Witching and the $20K Put

Tomorrow, Friday March 20, the quarterly quadruple witching event arrives - and the crypto market is directly in the blast radius. On Deribit alone, $13.5 billion in Bitcoin options are set to expire simultaneously with a cascade of equity index futures, stock index options, single-stock options, and single-stock futures in traditional markets.

The event occurs on the third Friday of March, June, September, and December each year. The March 2025 equivalent saw $4.7 trillion in equity and index derivatives expire, generating the highest S&P 500 trading volume of that entire year. This year's expiry arrives during an already elevated volatility environment: VIX above 35, oil near $100, Bitcoin below $70,000, and fresh inflation data that has rerouted rate cut expectations.

Cole Kennelly, CEO of Volmex Finance, flagged the cross-asset spillover directly: "Quadruple witching could trigger a spike in cross-asset volatility as large derivatives positions expire. This may already be showing up in crypto, with the Bitcoin Volmex Implied Volatility (BVIV) Index trending higher into the event."

The specific options positioning on Deribit tells its own story. Three strikes dominate the open interest landscape:

- $125,000 call - $740 million notional - largest single strike. Bull case target still in play for institutional positioning.

- $75,000 - $687 million notional - the max pain level, the price where the largest number of options expire worthless. Market makers hedge around this level, theoretically creating price gravity toward $75K into expiry.

- $20,000 put - $596 million notional - third largest strike. Deep out of the money (a 71% drawdown from current prices). This is the headline number.

The $20,000 put position deserves context before the bear narrative runs wild with it. Nearly $600 million in $20K puts does not mean $600 million worth of traders expect Bitcoin to collapse to $20,000. The more likely explanation is systematic options strategies: traders selling these deep OTM puts to collect premium, betting on the low probability of a crash. It is an income generation or volatility strategy, not a directional bet on collapse.

The broader picture from options remains slightly constructive. The put-call ratio sits at 0.63, meaning there are more calls than puts outstanding - a mild net bullish lean. Total open interest: 195,719 BTC, with 120,236 BTC in calls and 75,482 BTC in puts. The max pain magnet at $75,000 is still 8% above current prices, and if market makers manage positions around that level into Friday's close, price gravity could work in BTC's favor in the near term.

Bitcoin's historical quadruple witching performance in 2025 offered mixed signals. The March 2025 event saw muted performance on the day, followed by a significant drawdown weeks later linked to Liberation Day tariffs. June 2025 witching preceded a local bottom at $98,000. September was -1% on the day with modest continuation lower. December finished flat. The pattern: witching day itself is often quiet, but the following weeks can see resolution of whichever macro tension was building at the time.

The Iran Conflict's Financial Fingerprints: Oil at $100 and the Inflation Math

None of the above happens without oil. The connecting thread running through the Fed's hawkishness, the OG Bitcoin whale exits, the gold crash, and the broad risk-off environment is a single commodity that the March attack on Iran sent surging from below $60 to nearly $100 per barrel - a 67% move in weeks.

Oil at $100 per barrel is an inflation bomb for an economy that had only recently brought CPI toward the Fed's 2% target. Energy costs flow through to transportation, manufacturing, food, and services. The Fed knows this. Their revised 2026 CPI forecast of 2.7% (up from 2.4%) is an acknowledgment that the war has already changed their baseline assumptions. What the dot plot cannot account for is how much higher oil goes if the conflict escalates further.

A Politico report on Thursday briefly reversed an oil decline by confirming the U.S. is not considering a crude export ban - this news alone pushed oil back toward $100 after it had retreated slightly. That price sensitivity to single news items illustrates the fragility of the current equilibrium. One pipeline disruption, one naval incident in the Gulf, one additional supply shock, and the inflation trajectory changes again.

Oil price pre-Iran war (early 2026): below $60/bbl

Oil price current range: $95-$100/bbl

Price increase since outbreak: approximately +67%

Fed 2026 CPI forecast revision: 2.4% to 2.7%

Fed 2027 CPI forecast: 2.2% (was 2.1%)

Rate cut probability (1 cut in 2026): 80% on Polymarket, CME FedWatch

10-year Treasury yield: 4.21% (higher on the day)

For Bitcoin specifically, oil's role is dual-edged. High oil prices kill rate cut hopes, tighten liquidity, and reduce appetite for risk assets - all bearish macro. But high oil prices also make energy-intensive proof-of-work mining more expensive, potentially accelerating the centralization of hash rate toward miners with locked-in energy contracts or cheap renewable access. The broader inflation argument for holding hard assets like Bitcoin gains more traction in a persistently high-energy-cost environment - but only if the liquidity environment permits it.

What Comes Next: The Quadruple Witching Playbook and Q2 Setup

The 24 hours ahead are high-stakes. Friday's quadruple witching forces institutions globally to settle trillions in derivatives positions in a compressed window. Traditional finance's risk rebalancing will spill into crypto - it always does, and the correlation between equities and Bitcoin has only increased since institutional adoption accelerated through 2024-2025.

The key levels to watch: $69,000 support on Bitcoin, which has held through today's pressure despite the convergence of negative catalysts. A close below $69,000 into the weekly opens the question of $65,000 - a level that would put Bitcoin down roughly 13% from the recent $74,500 high. The max pain $75,000 level represents the upside case if market makers manage the options book aggressively into Friday's close and macro cooperates.

On the DeFi side, Venus Protocol's governance vote on covering the $2.15 million bad debt is the immediate watch item. If the risk fund absorbs the loss cleanly and the affected markets resume normally, the damage stays contained. If the governance vote gets contentious or XVS continues its decline, sentiment around BNB Chain DeFi protocols broadly could deteriorate. The affected markets - BCH, LTC, AAVE, and others placed on heightened monitoring - represent meaningful open interest on-chain.

The longer Q2 setup depends on whether the Iran conflict stabilizes or escalates. Every scenario analysis right now branches from that single geopolitical decision tree. If oil retreats below $80 on ceasefire signals, the macro backdrop shifts materially and rate cut probability increases. If oil holds above $100 or pushes higher, the Fed's hawkish posture becomes more entrenched, and the "one cut in 2026" scenario locks in as the base case - a ceiling for risk asset expansion.

Bitcoin's institutional buyer base - ETF inflows, treasury firms, long-term holders - has not shown distress signals beyond the two OG whale dumps. The structural demand thesis remains intact. But as Wintermute's Bryan Tan said: with correlation to oil running this hot and sentiment moving on every conflict headline, the strongest position right now is no position at all. Preserve the dry powder. Wait for confirmation. The volatility will provide the entry.

BTC support: $69,000 (day-close), $65,000 (next major level if support breaks)

BTC resistance: $72,000 (post-FOMC high), $74,500 (weekly high), $75,000 (max pain, options magnet)

Options expiry: Deribit quarterly, Friday March 20 - $13.5B notional

Venus governance vote: outcome determines XVS recovery timeline

Oil trigger level: $80 (dovish pivot signal), $110+ (inflation emergency)

Fed first cut implied: Q4 2026 at earliest per current pricing

Timeline of Events: 48 Hours That Moved Markets

Attacker donates 36M THE tokens to vTHE contract, exploiting missing cap checks. THE pumped from $0.26 to $0.56. Assets borrowed against inflated collateral.

US inflation data comes in above expectations, reinforcing fears that energy costs are feeding into core CPI. Bitcoin slides from $74,500 toward $72,000.

Federal Reserve holds at 3.50-3.75% (11-1 vote). Raises 2026 CPI forecast to 2.7%. Dot plot: one cut in 2026. Powell's personal projection moves higher. Bitcoin down 3.5% on the session to $71,600.

Lookonchain flags two long-term Bitcoin holders offloading 1,650 BTC ($117.87M) combined. BTC dips to $70,600.

CoinDesk reports XVS down 9% as whale wallets linked to Justin Sun move large amounts to exchanges. Venus protocol confirms $2.15M bad debt. PeckShield publishes Tornado Cash funding trail.

Report confirms US not considering crude export ban. Oil reverses brief decline, moves back toward $100/bbl. S&P 500 and Nasdaq hit fresh 2026 lows. Bitcoin holds $69,000-$69,400.

Deribit quarterly expiry positioning revealed: $13.5B notional, $596M in $20K puts (third most popular strike), max pain at $75,000. BVIV trending higher into expiry.

Quarterly expiry of stock index futures, stock index options, single-stock options, and single-stock futures. Trillions in derivatives settle. Cross-asset volatility expected. Watch $69,000 BTC support and $75,000 max pain attractor.

The DeFi Permissionless Paradox: Flagged and Still Looted

The Venus exploit raises a question that no protocol has satisfactorily answered: what is the point of a security community if the protocol cannot act on their findings? Venus confirmed that the attacking address was flagged by community members before the incident. The protocol reviewed the flag and determined that since no rules had been technically broken, no action was warranted.

This is the permissionless paradox at the heart of DeFi. The same architectural principle that makes protocols resistant to censorship and government shutdown - the inability to discriminate against participants based on suspicion alone - is the principle that prevents protecting users from methodical, patient attackers who build toward an exploit over months.

The attacker in this case understood this perfectly. Nine months of accumulation was not just about building position. It was about staying within the rules long enough that the protocol could not act. The Tornado Cash funding was mixed months in advance. The position was accumulated gradually enough to avoid triggering automated alerts. Every step was calculated to remain technically compliant until the moment of extraction.

Venus is now closing the specific code gap that allowed the donation-bypass of cap checks. The affected markets are paused. The governance vote on the risk fund is pending. But the pattern - attacker flagged, community warns, protocol cannot act, money extracted - will repeat on another protocol unless the industry develops better tooling for preventive governance action without sacrificing permissionless principles.

The total damage is contained in DeFi terms: $2.15 million in bad debt against $1.4 billion in TVL is 0.15% of the protocol's value. The reputational cost and the XVS price impact are larger than the direct financial loss. But the methodology is concerning. This is not a bug hunter extracting a flash loan profit in one block. This is an adversarial actor treating DeFi protocols as long-term targets requiring patient infiltration.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram