Bitcoin Finally Acts Like a Hedge. NFTs Down 50%. Clarity Act on Life Support.

The Bitcoin Hedge Thesis Just Got Real Evidence

For years, the "Bitcoin as digital gold" narrative was wishful thinking dressed up as macro theory. Every time equities tanked, BTC went down harder. The 2022 rate shock took both to the floor. The 2020 pandemic flash crash hit crypto worse than stocks. Traders learned the pattern: when the VIX spikes, sell everything including crypto.

The Iran war changed that script. As US airstrikes on Iranian facilities entered their third week and global equity markets priced in sustained disruption - S&P 500 down over 1%, NASDAQ down nearly 3%, European indices off 3-4% - Bitcoin gained approximately 2%. Not just held flat. Actually gained.

Rob Hadick, General Partner at Dragonfly Capital - the $4 billion crypto-focused fund - flagged this explicitly on the Unchained podcast this week.

"Crypto has held up surprisingly well despite global equity markets being down. We actually saw crypto hold up pretty well. It doesn't seem like the crypto markets are as fragile as maybe the equity markets are right now." - Rob Hadick, Dragonfly Capital

Hadick's read is that the composition of Bitcoin holders has fundamentally shifted. The leveraged retail speculator who would panic-sell at any negative headline is largely gone - flushed out through the bear cycles of 2022, the FTX contagion, and the grinding losses of early 2025. What remains is a base of long-duration holders: institutions, sovereigns, corporate treasuries, and retail investors who have already lived through the worst and aren't selling into geopolitical noise.

The numbers support this read. Bitcoin's 30-day realized volatility has been declining even as spot prices have range-traded. Exchange outflows remain elevated - meaning BTC is moving off exchanges into cold storage at pace. Open interest in CME Bitcoin futures, the institutional venue, has stayed elevated rather than collapsing as it would in a typical fear-driven unwind.

Chris Perkins, President of CoinFund and former Global Co-Head of Futures at Citi, added another layer: the VIX moving up while equity markets stay relatively flat is itself a bullish signal for Bitcoin. It means uncertainty is being priced in, but the actual selling hasn't materialized yet. Resolution of the Iran conflict - whenever it comes - would likely trigger a sharp rally in risk assets including crypto.

"The volatility index being up while markets are flat is a bullish sign. Bitcoin is showing signs of strength and resilience, indicating a potential bottoming in the market." - Chris Perkins, CoinFund

Ray Dalio, founder of Bridgewater Associates - the world's largest hedge fund at $160 billion under management - has been making a broader macro case that also benefits Bitcoin. Speaking on the All-In Podcast, Dalio outlined what he sees as the five major forces currently shaping the economy: debt dynamics, domestic wealth gaps, values gaps, international conflict, and the natural order of cycles. The through-line across all five is that the US dollar's reserve status faces structural pressure.

Dalio's view on gold - that it is "the most established money" and "the second largest reserve currency" - increasingly applies to Bitcoin in institutional portfolio construction. As the US government runs what Dalio describes as a 40% deficit (spending $7 trillion, taking in $5 trillion), and with $9 trillion in US debt rolling over in the near term, the case for non-sovereign stores of value is straightforward arithmetic.

The bond market is the real warning sign here. Yields are rising when conventional wisdom says they should be falling - investors fleeing to safety should buy bonds, pushing prices up and yields down. The fact that they are not suggests serious confusion about whether the Fed can fight inflation while also dealing with a war-driven supply shock. Stagflation risk is rising fast, and in a stagflationary environment, Bitcoin has a stronger theoretical case than either equities or bonds.

Trump's Europe Tariffs Wiped $875 Million in Hours

The Bitcoin hedge thesis has limits. Those limits showed themselves clearly when Trump's European tariff announcement hit the wires. The announcement - sweeping import tariffs targeting EU goods in what traders interpreted as a broadening of the trade war from Asia to Europe - triggered an immediate liquidation cascade across crypto markets.

$875 million in crypto positions were wiped out within hours of the tariff announcement, according to data aggregated by CryptoNews. The liquidation was broad-based: Bitcoin, Ethereum, and major altcoins all sold off simultaneously. This was not the kind of decoupling performance that the Iran war narrative had been building.

The distinction matters. The Iran conflict is essentially an oil supply shock - a geopolitical crisis with a clear macro transmission mechanism (energy prices, inflation, safe haven flows). Bitcoin has an argument in that scenario: it is a non-sovereign asset uncorrelated to the specific countries fighting. Tariffs are different. Tariffs hit global growth directly, compress corporate earnings, and generate the kind of risk-off panic that still sweeps up crypto alongside equities.

Put differently: Bitcoin may be developing real hedge characteristics against geopolitical risk, but it is not yet immune to macro demand destruction. The investor class that holds Bitcoin is still sophisticated enough to reduce all risk exposure when a significant negative growth shock hits - and a US-EU trade war is exactly that kind of shock.

The $875 million liquidation figure is also a signal of how much leverage remains in the system. Perpetual futures funding rates, which measure the cost of holding long positions, had been elevated before the tariff announcement. The sell-off suggests traders were running crowded longs that got washed out when the negative headline landed. The mechanics remain the same as 2021 and 2022 - leverage builds, a catalyst hits, cascading liquidations follow.

Hyperliquid, the on-chain perpetuals exchange that has emerged as the preferred venue for sophisticated traders, saw massive volume spikes during both the Iran escalation and the tariff shock. Commodity derivatives - particularly oil contracts - are where much of the action has been. According to Rob Hadick, Hyperliquid has seen "significant significant uptake in volume on the commodity side and on the rates side as well." The traditional commodity futures markets, unlike crypto, close on weekends - creating an arbitrage opportunity for on-chain venues that trade 24/7.

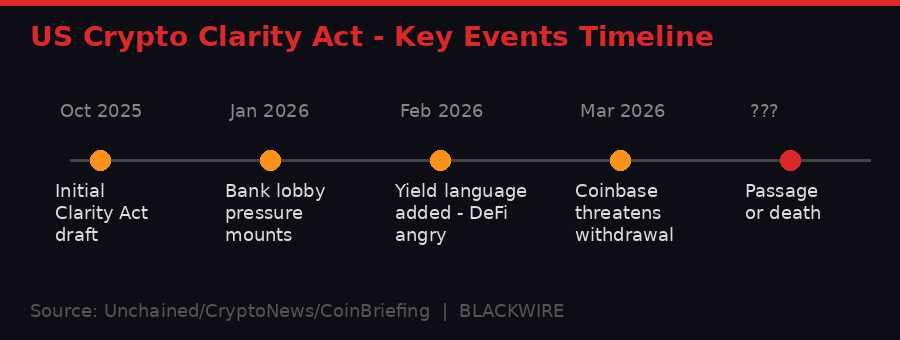

The Clarity Act's Quiet Death - A Yield Clause Is Killing It

The Clarity Act was supposed to be the crown jewel of crypto's political capital. After years of navigating SEC enforcement actions, surviving the FTX collapse, and building bipartisan relationships in Congress, the industry was finally close to a comprehensive market structure bill. Coinbase funded lobbying efforts. Industry leaders testified. The votes looked like they were there.

Now Coinbase is threatening to pull its backing. The issue is a yield clause added to recent drafts of the bill that DeFi protocols and crypto companies argue is broadly written enough to classify yield-bearing products - like staking returns, DeFi lending yields, and even stablecoin interest - as securities. That classification would bring them under SEC jurisdiction, the exact regulatory regime the industry has been fighting to escape.

According to Unchained's DEX in the City podcast, regulators are already "preparing for a world without the Clarity Act" - meaning the SEC and CFTC are quietly developing regulatory frameworks that don't depend on legislative clarity. The SEC has already sent a crypto securities framework to the White House for review, suggesting the agency isn't waiting for Congress to act.

Tushar Jain, Co-Founder of Multicoin Capital, offered a pointed analysis of where the market structure debate stands. The problem, in his view, is not regulatory hostility - it is that the industry failed to demonstrate enough utility to Congress to make the case for light-touch regulation airtight.

"The crypto industry needs to demonstrate more utility and real value to improve its reputation with Congress." - Chris Perkins, CoinFund

The stablecoin bill is in slightly better shape, but it is also tangled in the same fight. If stablecoin issuers are required to hold reserves exclusively at smaller community banks rather than large banks, it disadvantages large financial institutions - who then lobby hard against the bill. Chris Perkins noted bluntly that treating "big banks and community banks as a monolith is misleading" - their interests are not aligned, and the legislative process is being shaped by that misalignment.

The DOJ angle adds another layer of dysfunction. Senators are demanding answers after the Justice Department quietly dismantled its National Cryptocurrency Enforcement Team (NCET), the dedicated crypto crime unit that had handled major prosecutions including exchange hacks, ransomware cases, and sanctions evasion. The shutdown comes at precisely the moment Iranian hacker groups are reported to be actively targeting US banking and crypto infrastructure.

The conflict of interest question is real: several DOJ officials with authority over crypto enforcement hold personal crypto positions, raising questions about whether dismantling the enforcement unit serves the public interest or personal financial interests. This is the kind of institutional rot that the crypto industry's opponents have been warning about since the Trump administration took a hands-off approach to crypto regulation.

The net result is a regulatory environment that is simultaneously more permissive (no enforcement unit, strategic reserve signed, Fed master accounts approved for Kraken) and more uncertain (Clarity Act stalled, SEC quietly building its own framework, stablecoin bill deadlocked) than at any point in the industry's history. Markets hate uncertainty. And right now, uncertainty is the dominant regulatory commodity.

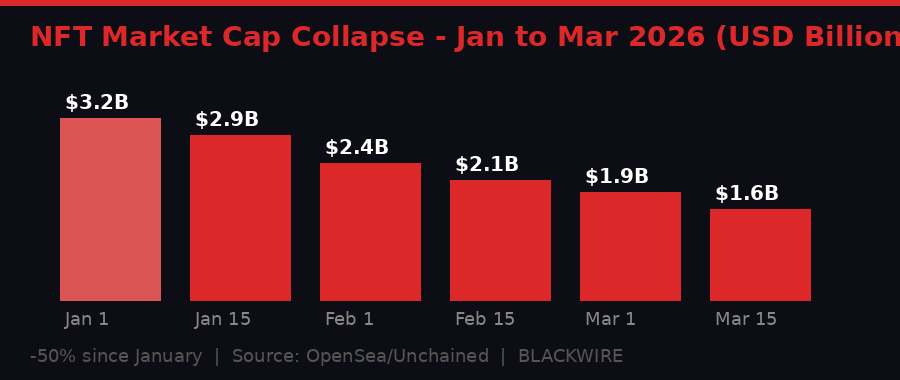

OpenSea Cancels Its Token - NFT Market Down 50%

OpenSea CEO Devin Finzer posted to X on March 17: "A delay is a delay. I'm not going to dress it up, and I know how it lands." The SEA token generation event, which had been scheduled for a March 30 community gathering, has been postponed indefinitely. No new date given. No concrete timeline. Just challenging market conditions and a promise to return when things improve.

The numbers behind the delay are ugly. NFT market capitalization has fallen approximately 50% since mid-January to around $1.6 billion. OpenSea's monthly trading volumes have slipped below $500 million. The platform that once processed billions in blue-chip NFT trades - Bored Apes, CryptoPunks, Azuki - is now generating most of its volume from regular crypto token swaps, not NFTs. More than 90% of its October 2025 trading volume came from crypto swaps under the OS2 rebuild.

This is a structural shift, not a cyclical one. The NFT thesis of 2021 was that digital ownership would create a new asset class: scarce, verifiable, culturally significant. The execution was largely speculative mania - people buying JPEGs hoping someone else would pay more. When the speculative layer was stripped away, the actual utility layer (gaming items, event tickets, verifiable credentials) proved much smaller than the hype suggested.

OpenSea's pivot to broad crypto trading is an implicit admission that the NFT-first model is not sustainable as a standalone business. The irony is that by building OS2 as a multi-chain crypto trading hub, OpenSea is now competing directly with DEXes that were not designed to also handle NFTs. It is a crowded market with better-established competitors.

To soften the token delay blow, OpenSea offered fee refunds for participants in rewards waves three through six, and announced zero-percent token trading fees for 60 days starting March 31. These are retention mechanics - ways to keep users engaged until the market improves enough to justify a token launch. But they also signal that the platform recognizes it needs to spend down goodwill to hold its user base together through a difficult period.

The broader NFT market is not just down in USD terms. Activity - measured by unique wallets interacting with NFT contracts - has fallen sharply. The median sale price for blue-chip collections has collapsed. Floor prices for Bored Apes, which peaked above $400,000 in 2022, are now a fraction of that. The collector class that built fortunes on NFT speculation has largely exited. What remains is a smaller, more utility-focused market that looks nothing like the 2021 frenzy.

Monad Launches on Coinbase - 85,000 Participants, Real Competition

While the regulatory and NFT headlines were grim, one genuine positive landed this week: Monad's mainnet went live, and its first token sale through Coinbase's new platform attracted over 85,000 participants. That is not a rounding error. That is a meaningful user base for a blockchain that, until recently, was known only to institutional investors and DeFi developers.

Keone Hon, Monad's co-founder and CEO, spent eight years leading a high-frequency trading team at Jump Trading before pivoting to blockchain infrastructure. He raised $225 million in Series B funding to build what Monad claims is a "parallel EVM" - an Ethereum-compatible blockchain that processes transactions in parallel rather than sequentially, targeting 10,000+ transactions per second versus Ethereum's roughly 15-30 TPS.

The launch performance has reportedly matched the pitch. According to Hon, "the blockchain itself worked really seamlessly - folks were excited about the UX, speed of transaction processing, compatibility with all wallets. No major issues and the chain itself is really fast and really performant."

What set Monad's launch apart from other recent L1 introductions was the deliberate decision not to run an ecosystem-wide pre-deposit campaign. Pre-deposit campaigns - where protocols incentivize users to stake assets before launch to build liquidity - have become standard procedure, and they often result in mercenary capital that exits immediately post-launch. Monad skipped this step and launched with a broad airdrop distribution instead, attempting to build a genuine user base rather than mercenary liquidity.

The Coinbase partnership is strategically significant. Being the first project to conduct a token sale on Coinbase's new platform provides Monad with both distribution reach - Coinbase's retail customer base numbers in the tens of millions - and an implicit stamp of credibility from the most regulated exchange in the US market. For institutional players watching from the sidelines, Coinbase's involvement signals that Monad has cleared at least preliminary due diligence.

The competitive landscape is fierce. Monad is entering a market where Ethereum remains dominant for DeFi and institutional use, Solana has captured much of the high-throughput trading activity, and a long tail of alternative L1s - Avalanche, Sui, Aptos, Sei - are fighting for the same user base. Tushar Jain of Multicoin Capital offered a framework for thinking about this:

"The market is misvaluing Layer 1s compared to applications. DeFi protocols generating real sustainable cash flows are where the financial value actually is." - Tushar Jain, Multicoin Capital

This is the bear case for Monad and every new L1: even if the chain is technically excellent, the value accrual happens at the application layer, not the infrastructure layer. Ethereum's value comes partly from the Uniswaps and Aaves and Lidos built on top of it. Monad needs to build that ecosystem - or attract existing protocols from Ethereum - to generate the fee revenue that justifies its token's price.

The 10,000+ TPS claim also needs sustained real-world validation. Processing capacity under ideal conditions, with test transactions, is very different from performance under production load with complex DeFi interactions, high-value MEV activity, and adversarial actors probing for weaknesses. The first few months of Monad's mainnet will be the real test - watched closely by both the $225M in investors who funded it and the competitors hoping to find its vulnerabilities.

The Market Structure Shift Nobody Is Talking About

Step back from the individual news items and a deeper structural story emerges. Traditional finance - with its 9-to-4 trading windows, settlement delays, and weekend closures - is increasingly inadequate for a world where geopolitical events and market-moving news happen continuously. The Iran war demonstrated this clearly.

When missile strikes happened at 2 AM on a Saturday, crypto markets processed the news immediately. Oil futures on Hyperliquid - an on-chain perpetuals venue - moved within minutes. Traders could hedge, adjust positions, and manage risk in real time. Traditional commodity futures traders had to wait until Monday morning. By the time the CME opened, the initial price discovery had already happened in crypto markets.

This is the market structure shift Perkins is pointing to when he says "the 24/7 nature of markets allows for real-time collateral management, enhancing liquidity." It is not just about convenience. It is about which venue actually sets prices during the hours when traditional markets are closed. Crypto is increasingly winning that competition.

The Kraken Federal Reserve master account approval - which happened earlier this month - is another brick in this wall. Kraken's banking arm can now settle US dollar transfers through Fedwire, the Fed's core payment infrastructure, without going through intermediary banks. Previous attempts by crypto-focused banks like Custodia were rejected. Kraken's success marks the first time a crypto exchange has plugged directly into the Fed's core payment rails.

Arjun Sethi, Kraken's co-CEO, described the access as allowing the firm to operate "as a directly connected financial institution." The implications are significant: faster fiat on/off ramps, lower settlement costs, and a regulatory relationship with the Federal Reserve that most crypto firms have never achieved. It also makes Kraken harder to destabilize - a company with a Fed master account has a level of institutional backing that gives regulators pause before taking aggressive enforcement action.

Meanwhile, the Block layoffs narrative continues to generate industry anxiety. Jack Dorsey's company cut its workforce by nearly half - from over 10,000 to under 6,000 - in February, and the handful of rehires that followed did nothing to change the headline number. Balaji Srinivasan, Coinbase's former CTO, called this the first "AI cut" and warned the tech industry: "Learn the AI tools and raise your game. Or you might not make the cut, as an employee or as a company."

The crypto sector is not immune. Algorand cut 25% of its workforce. OP Labs, the team behind Optimism, has restructured. Gemini has trimmed headcount multiple times. The companies surviving and growing are those that are rebuilding around AI-augmented workflows - fewer people, more automation, higher output per person. This is the new normal for crypto startups and it will accelerate as AI tools become more capable.

What Happens Next: The Variables That Matter

The variables that determine where markets go from here are knowable, even if the outcomes are not.

1. Iran war duration and oil price trajectory. Trump said the conflict would last "at least four weeks." Given the military realities - 93 million people in Iran, no clear path to regime change via airpower alone, and no ground troops committed - Hadick's assessment that "four weeks is probably an understatement" seems right. Every week the conflict extends is another week of $100+ oil, inflation pressure, and stagflation risk. The longer it goes, the more the Fed's rate cut path gets repriced. Bitcoin can absorb geopolitical uncertainty, but it cannot absorb a recession.

2. Clarity Act fate. The yield clause fight needs a resolution before anything else moves forward. Either the problematic language gets stripped out - which requires Congress members to hold firm against banking lobby pressure - or the bill dies and the SEC framework becomes the de facto regulatory regime. The industry has six to eight weeks at most to force a decision before 2026 midterm election dynamics make any major legislation politically impossible.

3. Federal Reserve guidance. The next Fed meeting will be scrutinized for any signal on how the central bank is thinking about the inflation-growth tradeoff. If the Fed signals it will tolerate higher inflation to support growth, risk assets including crypto get a tailwind. If it signals rate hikes are back on the table to fight energy-driven inflation, expect a significant risk-off move across all assets.

4. Monad's ecosystem buildout. The 85,000 Coinbase participants are a starting point, not a destination. Monad needs DeFi protocols with real TVL, trading venues with actual volume, and applications that can only be built on Monad rather than Ethereum or Solana. The next 90 days will show whether the technical performance translates to developer and user adoption.

5. Institutional allocation timing. Multiple institutional investors - Dragonfly, Multicoin, CoinFund - are explicitly stating they see capital on the sidelines waiting to enter. The question is what triggers that capital deployment. A ceasefire in Iran would likely do it. A positive Fed signal would help. A Clarity Act resolution would add confidence. Any combination of these could be the catalyst for the next leg up.

The macro case for Bitcoin has never been better argued. The regulatory environment has never been more contradictory. The product layer - DeFi, stablecoins, on-chain commodities trading - has never been more technically capable. What is missing is a clear trigger. The market is coiled. It is waiting for someone to release the spring.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram