Bitcoin Breaks $71K: Powell's Inflation Warning, Collapsing Hash Rate & The End of Cheap Money

The Fed held rates steady as expected - then Jerome Powell dropped a bomb. Rising oil prices from the Iran war are feeding inflation, rate cuts are off the table, and bitcoin is paying the price. Here is everything that happened on March 18, 2026.

The Federal Reserve held its benchmark rate steady at 3.50%-3.75% on March 18, 2026. Powell's press conference sent markets into a tailspin. (Pexels)

Market Snapshot - March 18, 2026 Close

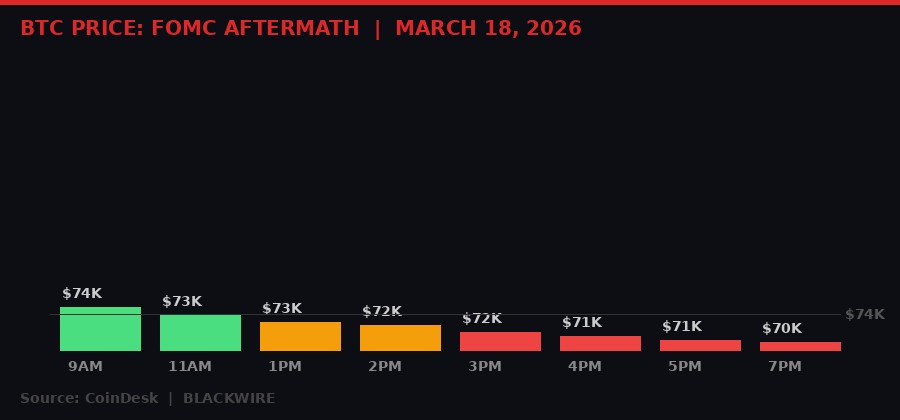

Bitcoin started March 18 holding $74,800. By the time Jerome Powell finished talking, it was printing lows of $70,900. That is a $3,900 round-trip in a single trading session - and the story is bigger than one candle.

The Federal Reserve did exactly what every trader expected: held the federal funds rate range steady at 3.50%-3.75%. No surprise there. Markets had priced in a hold for weeks. What nobody had fully priced in was Powell walking to that podium and saying, bluntly, that Iran war oil prices "for sure" show up in the inflation outlook - and that nobody knows how long they stick around.

That one phrase - "for sure shows up" - wiped billions off crypto valuations in ninety minutes. The S&P 500 and Nasdaq closed at their session lows. Gold, the traditional inflation hedge, sold off 3.1% on the day. When even gold dumps on a Fed hold day, you know something structural is shifting.

The Fed's Inflation Upgrade: What Powell Actually Said

Powell raised the Fed's 2026 inflation forecast to 2.7% from 2.4%, citing energy market disruption from the Iran war. (Pexels)

The FOMC statement itself was dovish in tone. Rates held at 3.50%-3.75%. The committee acknowledged slowing growth. Nothing in the written statement triggered the selloff.

The damage came in the press conference.

Powell acknowledged that policymakers had upgraded their 2026 Consumer Price Index forecast from 2.4% to 2.7%. The reason: energy prices. The Iran conflict and its disruption to the Strait of Hormuz have sent oil prices spiking, and those prices flow directly into transport costs, food production, manufacturing, and consumer goods.

"The oil shock for sure shows up in higher inflation projections." - Federal Reserve Chair Jerome Powell, March 18, 2026 press conference

When pushed on whether this constituted 1970s-style stagflation - slow growth, high inflation, the nightmare scenario - Powell pushed back. "That's not the case right now," he said. "I would reserve the term stagflation for a much more serious set of circumstances." He pointed to unemployment near long-run norms and inflation only modestly above target.

But his next line told the real story: "What we have is some tension between the goals, and we're trying to manage our way through it."

Translation: the Fed is stuck. It cannot cut rates aggressively to stimulate the economy without risking inflation re-acceleration. It cannot hike to kill inflation without killing growth too. The central bank is boxed in by a war it did not start and cannot end.

Markets read that immediately. Crypto, equities, and commodities all repriced lower in the final two hours of the session. Bitcoin, which had been holding $73,000-$74,000 for most of the day, broke through $72,000, then $71,000, and touched $70,900 by evening. Ether fell 6.5%. The CoinDesk 20 index declined 3.1%, with every constituent in the red. Uniswap led the DeFi bloodbath at -4.9%, Aave fell -4.4%.

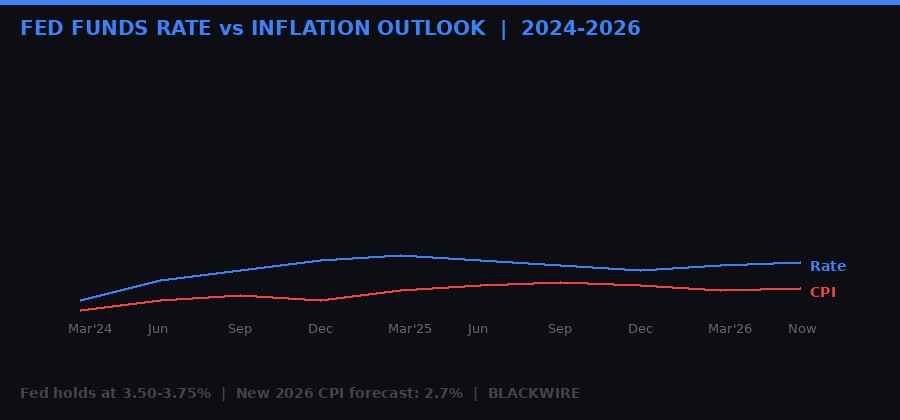

Federal funds rate vs CPI trajectory 2024-2026. The Fed's new 2.7% inflation forecast pushes rate cuts further out. (BLACKWIRE)

Bitcoin Miners Under Siege: Hash Rate Drops 8% in a Week

Bitcoin mining facilities face margin compression as energy costs soar. Hash rate has dropped 8% in one week to 920 EH/s. (Pexels)

While Wall Street was processing Powell's inflation comments, the Bitcoin network was quietly entering a crisis of its own.

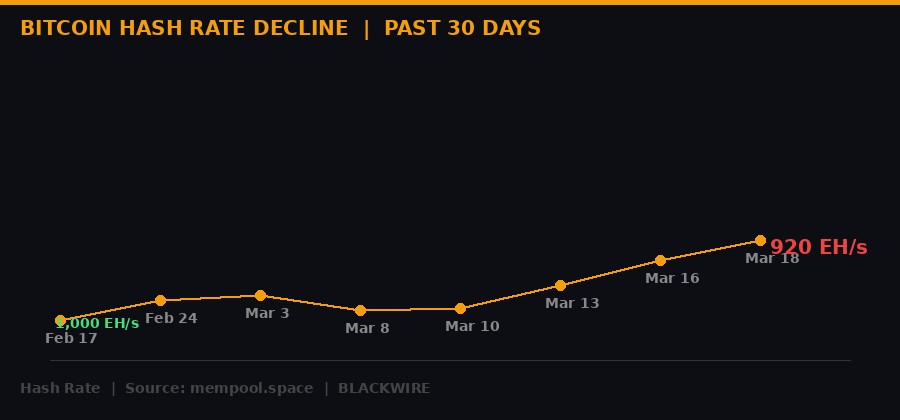

Bitcoin's hash rate - the total computational power securing the network - has dropped roughly 8% over the past week, falling to approximately 920 EH/s from around 1,000 EH/s. That is not normal volatility. That is a coordinated pullback driven by economics. CoinDesk reports that an estimated 8-10% of global bitcoin mining operates in energy markets directly sensitive to the Middle East conflict.

When oil prices surge, electricity costs follow - especially in regions that rely on natural gas for power generation. Miners operating on thin margins shut down rigs. When enough rigs go offline fast enough, the hash rate drops. And when hash rate drops, the network automatically schedules a downward difficulty adjustment to keep block times near 10 minutes.

According to data from mempool.space, Bitcoin is heading for an approximately 8% downward difficulty adjustment - the second-largest negative shift in the past five years. The last time the network saw a drop of this magnitude was in mid-February 2026, which itself was already described as one of the largest difficulty drops on record.

Two back-to-back historic difficulty drops in a single quarter. That is not noise - that is a structural breakdown in miner economics.

Bitcoin hash rate declined from ~1,000 EH/s to 920 EH/s in one week - the second-largest negative shift in five years. (BLACKWIRE / mempool.space)

Historically, miner capitulation phases correlate with price downturns. The logic is simple: miners who shut down rigs often sell bitcoin holdings to cover operational costs, adding sell pressure to the market. At the same time, lower hash rate signals network stress, spooking institutional investors.

The publicly traded miners have been responding to squeezed margins by diversifying aggressively. Companies like Cango have been liquidating BTC holdings to fund AI and high-performance computing pivots. This creates a double whammy for bitcoin price - fewer buyers and more sellers, all at the same time.

Strategy (MSTR), the largest corporate bitcoin holder, fell 5-6% on Wednesday alongside crypto prices. Bitmine (BMNR), the leading Ethereum treasury firm, also dropped in the same range. Galaxy Digital (GLXY) declined nearly 7%. Gemini (GEMI) was the session's disaster, tumbling 15% to near its lowest level since going public last year.

The Permanent Inflation Floor: Why This Time Is Different

The Strait of Hormuz disruption is triggering what energy experts call a permanent de-globalization of energy markets - with lasting inflation consequences. (Pexels)

The dominant market narrative since the Iran war began has been simple: oil spike is temporary, central banks will cut rates once the dust settles, liquidity returns, crypto pumps. It is the same script that played out after every geopolitical disruption since 2008.

But there is a mounting counter-argument: the scars from this war will be permanent.

Energy market expert Anas Alhajji laid out the thesis bluntly on X. The Iran war has exposed something fundamental: energy markets are fragile, and major economies built on cheap, globalized energy supply chains are uniquely exposed. The Hormuz disruption has triggered shortages across India, Japan, and South Korea. China's reserves buffer it for now. Even the supposedly energy-independent United States is feeling ripple effects.

"Once that mindset takes hold, global energy markets will never return to the old model of open, price-driven, largely commercial trade. Instead, capitalist economies will increasingly mirror the Chinese approach: heavy state direction, strategic stockpiling, vertical integration, subsidies for domestic champions, and prioritization of self-reliance over pure cost minimization." - Anas Alhajji, Energy Market Expert, via X (@anasalhajji)

The implications cascade outward. Fertilizer production relies on natural gas. Food prices follow. Semiconductor manufacturing requires helium and sulfur - both commodities flowing through Hormuz. The United Nations has already warned of higher global food prices if the strait closure extends. What started as an oil price shock is transmitting through every supply chain.

From 2008 to 2021, global CPI averaged below 3%, according to Federal Reserve data. That window of ultralow inflation allowed central banks to hold rates at or near zero, pump quantitative easing, and create the liquidity environment that drove every major asset class - stocks, crypto, bonds - to historic highs. The post-2022 rate hike cycle was supposed to be temporary. The Iran war may have made it permanent.

If Alhajji's thesis is correct, every nation is now repricing energy security as a national security issue. That means higher structural energy costs, slower economic growth, stickier inflation, and central banks that no longer have room to open the liquidity tap at will. The era of cheap money that defined post-2008 markets is over.

For bitcoin specifically, this creates a paradox. Higher inflation should theoretically be bullish for a scarce asset. But in practice, "higher for longer" rates increase the opportunity cost of holding non-yielding assets like bitcoin, suppressing price. The market is currently prioritizing the "higher for longer" fear over the "inflation hedge" thesis - and until that changes, the path of least resistance is down.

Nasdaq Gets SEC Green Light for Tokenized Securities Trading

The SEC approved Nasdaq's tokenized securities trading framework on March 18, 2026 - a milestone for blockchain-based equity markets. (Pexels)

Lost in the FOMC noise: one of the most significant regulatory approvals in U.S. financial market history dropped the same day BTC was dumping to $70,900.

The SEC approved Nasdaq's proposal to allow certain securities to trade in tokenized form on the blockchain. The SEC's official approval filing (Release No. 34-105047) greenlights a pilot framework tied to the Depository Trust Company (DTC) for clearing and settlement of tokenized trades.

Under the approved framework, eligible Nasdaq participants can choose to have trades settled as blockchain-based tokens rather than through standard book-entry systems. Tokenized shares trade alongside traditional shares on the same order book, at the same price, with identical rights, same ticker, same CUSIP identification number, and under existing market rules. Settlement timelines and investor protections remain intact.

This is not a crypto exchange launching a synthetic stock product. This is the actual Nasdaq - $28 trillion in listed market cap - getting regulatory permission to run real equity trades on a blockchain. The DTC, which handles clearing for virtually every U.S. stock trade, is the settlement backbone.

Nasdaq had been building toward this for months. It filed for regulatory permission in September 2025. Just last week, it announced a partnership with Kraken to distribute tokenized stocks globally. Intercontinental Exchange (ICE), owner of the NYSE, has been moving in parallel - investing in OKX with plans to launch tokenized stocks and crypto futures.

The $126 trillion global equity market is being put on blockchain infrastructure, incrementally. The irony of this approval landing on the same day crypto crashes below $71K is not lost on anyone who has been watching the space. The structural integration of TradFi and crypto is accelerating even as prices decline.

For traders, the near-term implication is real: tokenized stocks create new arbitrage vectors between crypto-native markets and legacy equity systems. Round-the-clock trading of equity-equivalent tokens removes time zone barriers. Hyperliquid already demonstrated this earlier in the week, with S&P Dow Jones Indices licensing its flagship index for crypto-based perpetual futures trading 24/7.

Kraken's IPO Goes Cold, FTX Pays Out $2.2 Billion

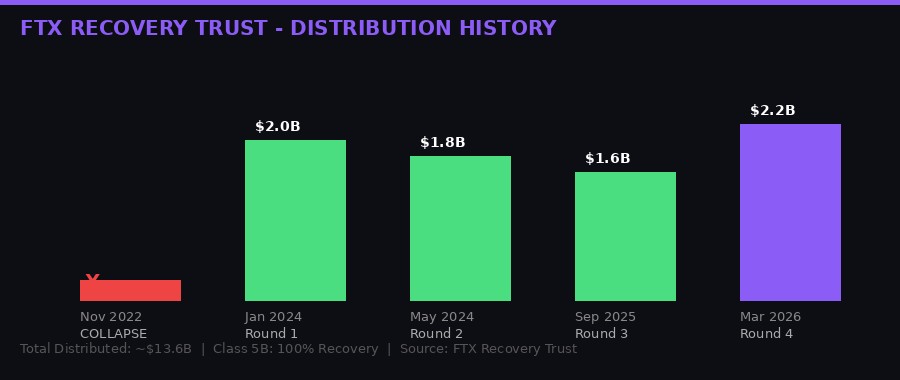

FTX Recovery Trust will distribute $2.2 billion to creditors on March 31 - the fourth major payout since Sam Bankman-Fried's exchange collapsed in November 2022. (Pexels)

While crypto prices fell, two divergent stories played out in the industry infrastructure layer: one company quietly shelved its public market ambitions, another distributed cash to victims of the industry's worst fraud.

Kraken - or technically Payward, its parent - has frozen its IPO plans. The company confidentially filed a draft S-1 with the SEC in November 2025, was valued at $20 billion when it raised $800 million in new funding (including $200 million from Citadel Securities), and seemed on track for a 2026 listing. Two sources with direct knowledge confirmed to CoinDesk the plan is on hold until market conditions improve.

The data backs the caution. BitGo was the only major crypto company to IPO in 2026 so far - and its stock is down 44% from listing. The downturn in crypto prices since October's highs has compressed valuations and dried up investor appetite. The IPO window that produced $14.6 billion in crypto listings in 2025 has slammed shut.

On the recovery side, FTX Recovery Trust announced it will distribute roughly $2.2 billion to creditors on March 31 - the fourth distribution under the Chapter 11 reorganization plan. Funds will flow via BitGo, Kraken, or Payoneer within 1-3 business days.

The payout structure is remarkable: "Class 5A Dotcom" creditors reach 96% total recovery with this distribution. U.S. customer claims in "Class 5B" hit 100% full recovery. "Class 6A" and "6B" also reach 100%. "Class 7" hits 120% cumulative distribution.

Combined with prior rounds totaling over $6 billion, FTX's total recovery distribution now approaches $8.2 billion. Sam Bankman-Fried is serving 25 years. The exchange collapsed in November 2022 with roughly $8-9 billion in customer funds missing. The fact that creditors are getting dollar-for-dollar or better recovery is a function of one thing: bitcoin's price since 2022 has roughly doubled, expanding the dollar value of recovered crypto assets.

FTX Recovery Trust distribution history: from collapse in November 2022 to $2.2B fourth distribution in March 2026. Class 5B U.S. customer claims reach 100% recovery. (BLACKWIRE)

Timeline: 24 Hours That Broke Bitcoin's Consolidation

Bitcoin price action on March 18: from $74,800 pre-session to $70,900 post-Powell. The Fed press conference was the catalyst. (Pexels)

What Comes Next: The Case For and Against a Recovery

The bull and bear cases for bitcoin diverge sharply at current price levels. The Iran war has introduced a structural uncertainty that technical analysis alone cannot resolve. (Pexels)

The bear case is not complicated. Bitcoin sits below $71,000 with hash rate in freefall, miners dumping, equity markets cracking, and the Federal Reserve explicitly telling the market that rate cuts are not coming anytime soon because of a war that shows no sign of ending. Every institution that bought bitcoin as a "rate cut play" is now offside.

Hash rate dropping 8% in one week points toward miner capitulation. Historically, these phases can last weeks. During the February 2026 difficulty drop - previously described as one of the largest in years - bitcoin dropped toward $67,000 before stabilizing. If the hash rate decline continues, another difficulty adjustment of similar magnitude follows. The pattern suggests additional downside pressure.

The strategic positioning also matters. Gemini (GEMI) down 15% in a single session, hitting near-IPO lows, reflects broader sentiment: crypto infrastructure companies are not being valued as growth assets in this environment. The Kraken IPO freeze confirms institutions are not in a rush to bet on a recovery.

The bull case requires believing a few things simultaneously. First, that the Iran war resolves or de-escalates, removing the energy price pressure and opening the door for rate cuts. Second, that bitcoin's scarcity and institutional adoption thesis reasserts itself once the macro headwinds lift. Third, that the Nasdaq tokenization approval and ongoing TradFi integration create structural buying demand that absorbs selling pressure.

The $2.2 billion FTX distribution actually has a credible bull angle. When creditors receive their funds through BitGo, Kraken, or Payoneer, many will choose conversion into digital assets rather than fiat withdrawal. Over $2 billion flowing back into crypto via exchanges could generate meaningful buy pressure in late March - assuming recipients want exposure rather than cash.

Senator Cynthia Lummis, one of the most crypto-friendly legislators in Congress, said Wednesday that market structure bill negotiations are down to "nuance" and the bill will emerge from committee in April. Regulatory clarity remains a structural tailwind for institutional adoption - but regulatory tailwinds do not override macro headwinds in the short term.

The honest assessment: bitcoin's price range for the next four to six weeks depends almost entirely on developments in the Middle East, not on-chain metrics, ETF flows, or development news. If Hormuz stays disrupted and oil stays elevated, Powell cannot cut, institutional buyers stay sidelined, and miners continue capitulating. If a ceasefire or significant de-escalation emerges, the macro picture shifts rapidly and the suppressed buying demand could trigger a violent rebound.

The market is hostage to a war it did not price correctly.

BTC intraday price action on March 18: opened at $74,800, broke to $70,900 post-Powell press conference. Ether fell 6.5% in the same session. (BLACKWIRE)

The Fairshake Fumble and Kalshi's Legal War

Two other stories that define the crypto political landscape on March 18:

Fairshake PAC, the crypto sector's $100M+ political war chest built over the past two years, spent over $10 million trying to defeat Illinois Senate candidate Emily Schaffer in the Democratic primary - and she won anyway. CoinDesk reports this marks the first significant political misfire for Fairshake, which had a near-perfect record in 2024. More than 5% of its entire war chest, gone on one failed primary intervention. The loss does not cripple Fairshake - it still has substantial resources - but it punctures the myth of crypto political invincibility and signals that money alone does not determine electoral outcomes.

Kalshi, the CFTC-regulated prediction market platform, is fighting back against Arizona, which has filed 20 criminal counts accusing it of operating an illegal gambling business and offering election wagering in violation of state law. Kalshi's co-founder called the charges a "total overstep," arguing that Arizona is attempting to challenge federal jurisdiction over a platform regulated by the CFTC. CoinDesk describes it as a federal-state turf war with implications for the broader applicability of federal law over state regulations in prediction market platforms. A loss for Kalshi in Arizona could fragment the prediction market landscape across 50 different state legal frameworks - a regulatory nightmare for the entire sector.

Both stories illustrate the same truth: crypto's political and regulatory wins in 2024-2025 were real, but they did not resolve the underlying tensions between federal oversight, state authority, and electoral politics. Each fight has to be won individually.