Alphabet Cuts the Cord: Google Fiber Is Being Sold Off and the Era of Big Tech Broadband Is Over

After 12 years and billions of dollars in subsidized fiber buildout, Alphabet is quietly handing Google Fiber to private equity. The merger with Stonepeak's Astound Broadband isn't a victory lap - it's an exit strategy. And it tells you everything about where Big Tech is putting its money now.

Google Fiber was supposed to force Comcast and AT&T to compete or die. In 2012, when it launched in Kansas City offering gigabit internet for $70 a month - at a time when most Americans were paying that for 25 megabits - it felt like a genuine disruption. Telecom analysts called it a "Sputnik moment" for broadband. Cable companies quietly started upgrading their networks just to avoid getting Google'd.

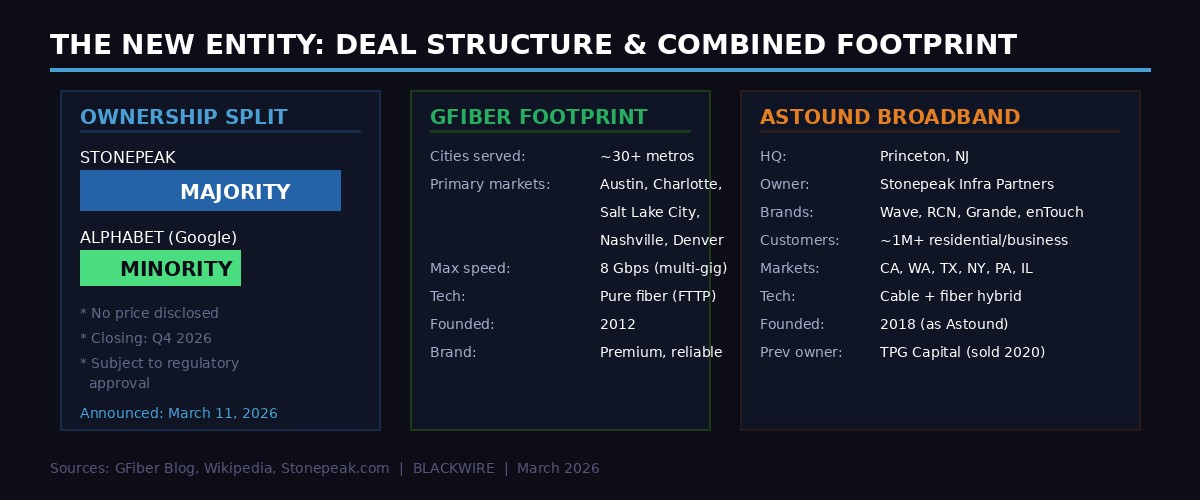

Fourteen years later, the disruption is ending with a bureaucratic press release. On March 11, 2026, Alphabet and Stonepeak Infrastructure Partners announced that GFiber - as Google Fiber is now officially branded - will merge with Stonepeak's existing cable and fiber property, Astound Broadband. Stonepeak becomes the majority shareholder. Alphabet keeps a "significant minority stake." The deal is expected to close by the end of 2026.

The announcement is framed in the language of ambition: "accelerating growth," "pioneering fiber technology," "a decade-long mission." But the substance is unmistakable. Alphabet is handing off a pet project it no longer wants to run. Google Fiber had its moment. That moment is over.

The Deal: What Was Actually Announced

The structure is straightforward on the surface. GFiber and Astound Broadband, which are both already owned or heavily associated with Stonepeak Infrastructure Partners, will combine into a single independent entity. Stonepeak holds the majority. Alphabet retains a minority stake, keeping some upside if the combined company thrives. The GFiber executive team - including CEO Dinni Jain, who has run the operation since 2020 - stays in place.

Deal structure and combined entity footprint. Stonepeak majority, Alphabet minority. Closing expected Q4 2026. Source: GFiber Blog, Wikipedia, BLACKWIRE Research.

No acquisition price has been disclosed. The transaction is subject to regulatory approvals, which are not expected to be particularly contentious given that neither GFiber nor Astound dominates any single market at the national level.

"GFiber will now have the opportunity to provide better internet access to more communities across the country as they combine with Stonepeak's Astound business, while continuing to provide their award-winning customer experience." - Ruth Porat, President and Chief Investment Officer, Alphabet and Google

That quote from Ruth Porat - Alphabet's CFO-turned-CIO, a woman whose primary job for a decade has been rationalizing the cost of Alphabet's moon-shot bets - is telling. It's the language of a graceful handoff, not a strategic expansion. "Better internet access to more communities" is what you say when you're transferring ownership to someone else's balance sheet.

GFiber CEO Dinni Jain was more forward-leaning in his statement: "This partnership with Astound and Stonepeak is the next step in our decade-long mission to redefine what customers can expect from their internet provider." Jain has fought hard to keep GFiber alive inside the Alphabet machine. This deal may actually give him more operational freedom than he had as an Alphabet subsidiary - with external capital and a focused infrastructure mandate, the new entity can grow without competing for budget against Google DeepMind and YouTube.

Deal Fast Facts

- Announced: March 11, 2026

- Structure: GFiber + Astound Broadband merger

- Majority Owner: Stonepeak Infrastructure Partners

- Minority Owner: Alphabet (Google's parent company)

- Price: Not disclosed

- Expected Close: Q4 2026, pending regulatory approval

- Combined CEO: Dinni Jain (current GFiber CEO)

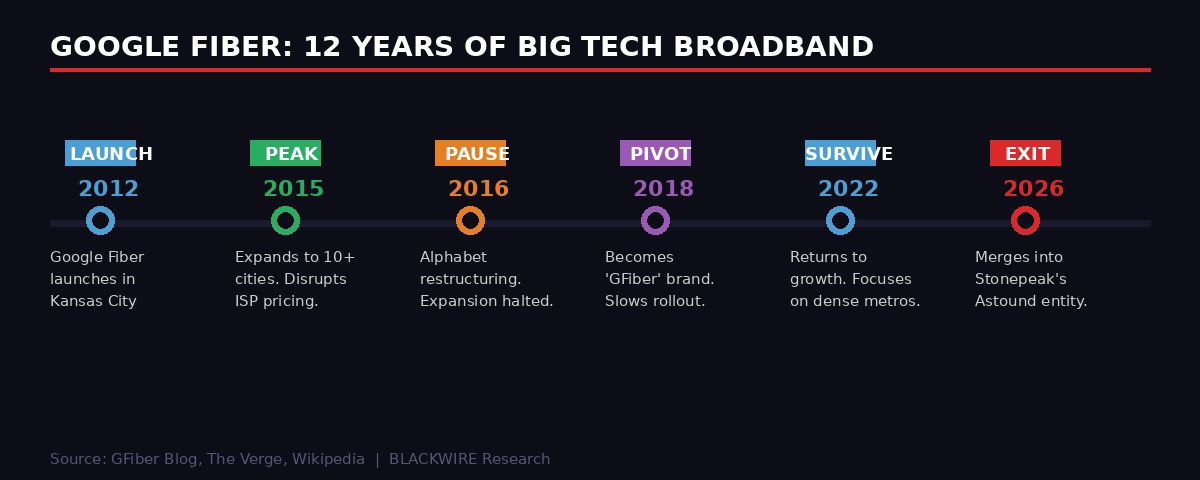

Google Fiber's 12 Years: A History of Brilliant Ideas and Execution Problems

Google Fiber's trajectory from disruptive launch in 2012 to the Stonepeak exit in 2026. Source: BLACKWIRE Research, GFiber Blog.

The story of Google Fiber tracks almost perfectly with the story of Silicon Valley's larger illusions about physical infrastructure - the idea that if you throw enough engineering talent and venture capital at a problem, the atoms will comply the same way the bits do.

Google Fiber launched in Kansas City in 2012 with genuine disruptive intent. The initial offering - 1 Gbps symmetric internet for $70 a month, or a free lower-tier option for a $300 installation fee - was not just faster than what incumbents were offering. It was a signal. Google was entering the market to force competition. The strategy worked almost immediately. AT&T and Comcast began announcing multi-gig upgrades in Kansas City and other cities where Google was considering expanding, even before a single foot of cable was laid.

By 2014, GFiber was rolling into Austin, Provo, and eventually a dozen more cities. Analysts estimated Google was losing money on every connection - the cost to trench fiber through urban neighborhoods and apartment buildings was vastly higher than the revenue from consumer subscriptions. But that was the point. This was infrastructure predatory pricing, Silicon Valley style: spend money now to force industry transformation, capture brand value and data, and figure out the monetization later.

The trouble arrived when "later" never quite materialized. In 2016, when Alphabet was reorganized under Sundar Pichai and Larry Page became more removed from day-to-day operations, Google Fiber got reclassified from "moonshot" to "expensive side project." Craig Barratt, who had led the expansion, abruptly resigned. Plans to expand to at least eight more cities were canceled. Hundreds of employees were laid off. The company stopped signing up new customers in cities where it had already begun construction in some neighborhoods.

The 2016 pivot was a significant tell. Alphabet had decided that building physical infrastructure at scale was not what technology companies should be doing. That insight was correct - but it took another decade and the rise of generative AI to make it completely obvious.

From 2017 onward, GFiber entered a kind of managed stasis. It kept existing customers. It continued building in markets where construction was already underway. In 2020, Dinni Jain took over and injected some momentum - GFiber launched multi-gig tiers, entered new markets like Nashville and Boise, and started marketing aggressively again. But it never recovered the ambition or the staffing levels of the 2014-2015 peak.

By 2025, GFiber was serving approximately 30 metropolitan areas with a customer base estimated in the hundreds of thousands - meaningful, but nowhere near the millions of homes that Alphabet's original expansion plans had projected. For context, Comcast serves roughly 32 million broadband subscribers. AT&T has about 27 million. Charter Spectrum has around 30 million. Google Fiber, after 12 years and billions in capital expenditure, never even approached 1% of the US broadband market.

Who Is Stonepeak - and Why Does Private Equity Now Own America's Internet?

Stonepeak Infrastructure Partners is not a household name outside of finance circles, but its portfolio reads like a map of the physical systems that keep modern life running. The New York-based firm, founded in 2011, manages over $70 billion in assets across data centers, pipelines, cell towers, power grids, shipping ports, and - obviously - broadband networks.

Stonepeak already owns Astound Broadband, which it acquired from TPG Capital in a $3.6 billion leveraged buyout in 2020-2021. Astound is itself a roll-up of regional cable providers: Wave Broadband (West Coast), RCN Corporation (East Coast), Grande Communications (Texas), enTouch Systems (Texas/South), and Digital West (California). Combined, Astound serves roughly one million residential and business customers across California, Washington, Texas, New York, Pennsylvania, Illinois, and surrounding states.

Adding GFiber to this portfolio gives Stonepeak something it currently lacks: a pure-play fiber brand with premium positioning and multi-gigabit capability. Astound's network is largely a cable hybrid - fast, but not fiber-to-the-premises. GFiber is 100% fiber all the way to the home, with speeds that currently top out at 8 Gbps on its top tier. That's a meaningful technical advantage as AI applications, 8K video, and cloud gaming begin demanding bandwidth that cable networks can barely sustain.

The strategic logic for Stonepeak is clear: build a national independent fiber platform to compete against the cable giants, funded by infrastructure-focused institutional capital that has lower cost-of-money requirements than a public tech company. Infrastructure funds typically accept 8-12% annual returns. For Alphabet, GFiber was a drag on a company that can generate 20%+ returns from advertising and cloud services. The same asset looks different depending on who holds it.

The deeper pattern here is one of the defining structural shifts in tech infrastructure over the past decade. Big Tech built or acquired physical assets during periods of cheap capital and strategic ambition - fiber networks, satellites, data centers, physical retail stores, logistics networks. As capital costs rose and AI became the dominant investment priority, those physical assets became liabilities. Private equity and infrastructure funds, which are structurally designed to hold long-duration physical assets, have been waiting to absorb them.

Amazon has been quietly divesting logistics real estate. Microsoft handed off some data center development to external partners. Google sold its Boston Dynamics robotics company twice before Hyundai finally absorbed it. This GFiber deal follows the same script.

What This Means for GFiber Customers

If you currently have Google Fiber, the most important thing to understand is that nothing changes immediately. The deal won't close until Q4 2026 at the earliest, and even after closing, transitions of this type typically involve years of gradual brand consolidation. The GFiber brand, the GFiber app, and the GFiber pricing will likely persist well into 2027 at minimum.

The medium-term risk for customers is the standard private equity playbook: reduce costs, maximize margin, and eventually raise prices. Stonepeak is an infrastructure fund, not a telecom operator with a consumer advocacy mission. Its fiduciary obligation is to its limited partners - pension funds, sovereign wealth funds, endowments - not to residents of Austin or Salt Lake City who pay $70 a month for gigabit service.

That said, the fiber internet market in 2026 is more competitive than it was in 2016. AT&T Fiber has been aggressively expanding, now passing over 30 million locations. Comcast has deployed its own fiber-to-the-premises product in several markets. Lumen Technologies, T-Mobile Home Internet, and dozens of smaller regional ISPs have entered markets where GFiber operates. Price increases are possible, but aggressive enough price increases to trigger customer defection would undermine the asset value Stonepeak just paid for.

The more likely outcome is operational efficiency improvements - reduced promotional pricing for new customers, slower network upgrades, and gradual absorption into the Astound billing and customer service infrastructure. If Stonepeak executes well, the combined entity could actually invest more in fiber buildout than Alphabet was willing to fund. Infrastructure investors love assets that require capital - they can deploy LP money into network construction rather than just paying it out as dividends.

Alphabet's AI Pivot - Where the Money Is Going Instead

The GFiber exit cannot be understood in isolation. It's one data point in a much larger story about Alphabet's capital allocation in the AI era.

In 2025, Alphabet announced plans to spend $75 billion in capital expenditure - primarily on AI data centers, custom silicon (Google TPUs), and cloud infrastructure. That number is roughly double what the company spent on capex in 2023. The Google AI infrastructure buildout is consuming enormous organizational energy and financial capital. Sundar Pichai has made it clear that every dollar in Alphabet's portfolio is being evaluated against its contribution to the AI race.

Against that backdrop, Google Fiber was increasingly hard to justify. Consumer broadband is a capital-intensive, low-margin, highly regulated business with slow growth and long payback periods. A fiber connection to a home in Nashville generates perhaps $80-100 per month in revenue with roughly 30-40% gross margins after network maintenance, customer service, and depreciation. The same money spent on Google Cloud AI infrastructure can generate multiple times that return if AI workloads keep growing at current rates.

The strategic rationale that originally justified Google Fiber - that widespread gigabit internet would increase internet usage and therefore benefit Google's core advertising business - has also weakened. Mobile internet, now dominated by 5G, has decoupled residential broadband from the search and advertising revenue that drives Google's profits. Most of the growth in online advertising is happening on mobile devices connected to cellular networks, not on desktop browsers connected to Google Fiber.

There's a second-order dynamic worth noting: Google Fiber's original competitive threat to cable companies has largely been accomplished. AT&T Fiber, Comcast, Charter, and dozens of municipal broadband providers have all dramatically upgraded their networks since 2012, partly in response to GFiber's entry into specific markets. Whether intentional or not, GFiber functioned as a forcing function. It made the US residential broadband market better. Now that the competitive pressure has been internalized by incumbents, the provocateur can exit stage left.

The US Broadband Landscape After Google Exits

The departure of Alphabet as an active operator changes the dynamics of the US broadband market, even if the GFiber brand persists under private equity. Big Tech's role in telecommunications has always been ambiguous - part disruptor, part investor, part regulator magnet. With Google out, the field is left to traditional telecom incumbents and a growing cohort of infrastructure-focused fiber operators.

The fiber buildout across the United States has accelerated dramatically since 2021, when the Biden administration passed the Infrastructure Investment and Jobs Act allocating $65 billion for broadband expansion. That money - much of it flowing through state BEAD (Broadband Equity, Access, and Deployment) programs - is funding fiber construction in rural and underserved areas that no private operator would touch on commercial terms alone. AT&T, Brightspeed, Frontier, and dozens of smaller carriers have announced major fiber expansion plans backed by this federal subsidy.

The Trump administration has not reversed this program, though it has slowed disbursements and added conditions. The net effect is that the US fiber ecosystem is expanding primarily through a combination of traditional telecom operators and infrastructure funds like Stonepeak - exactly the entities that are taking over GFiber. The Silicon Valley disruptor phase of broadband is over. The utility phase is beginning.

The implications for consumers are mixed. Infrastructure investors typically maintain quality and invest in network upgrades because degraded service destroys asset value. But they also extract margins more aggressively than a tech company subsidizing services for strategic reasons. The era of below-cost gigabit internet - which GFiber pioneered and which effectively forced the entire industry to upgrade - is almost certainly over. Get ready for internet prices that reflect the actual cost of fiber infrastructure plus a reasonable return on capital, rather than Google's implicit subsidy.

The Broader Pattern: Big Tech's Retreat from Atoms

Google Fiber joins a growing list of ambitious physical-world projects that Big Tech launched with transformative rhetoric and eventually handed off or shut down when the strategic math stopped working.

Amazon Fresh physical grocery stores, once positioned as the future of retail, have been scaling back since 2023. Amazon's Sidewalk network - a mesh of connected devices that would blanket suburban neighborhoods with low-power connectivity - never achieved the scale needed to become a real infrastructure asset. Google's Sidewalk Toronto smart city project was canceled after spending an estimated $50 million on planning work. Microsoft's expansion into nuclear power to fuel AI data centers is framed as infrastructure investment, but it's fundamentally different from consumer-facing infrastructure: it's captive power for Microsoft's own facilities, not a service for the public.

The pattern is consistent: Big Tech companies enter physical infrastructure markets with the promise of disruption, spend several years proving that atoms are harder than bits, and then exit when the opportunity cost of staying becomes too large. The infrastructure then passes to entities - utilities, private equity, sovereign wealth funds - that are designed to hold it for decades rather than years.

This is not necessarily bad for society. Physical infrastructure benefits from patient capital and operational stability, not from the restless innovation cycles of tech companies. A fiber network that gets upgraded every 18 months because a tech company wants to announce a new product is probably worse for customers than a network that gets maintained carefully over decades by an infrastructure fund with a 20-year investment horizon.

But it does mean that the "Big Tech will fix everything" narrative has limits. Google tried to fix broadband. It succeeded in pressuring incumbents to improve. Then it left. The fix was real, but the fixer is gone. That's a useful template for understanding every other area where Big Tech has claimed it would transform physical industries.

What Comes Next for the Combined Entity

Assuming the deal closes on schedule in Q4 2026, the combined GFiber-Astound entity will be one of the more interesting broadband operators in the country - a hybrid of Astound's cable-heavy legacy infrastructure and GFiber's premium pure-fiber network, operated under Stonepeak's infrastructure mandate with Alphabet as a strategic minority investor.

The immediate priorities for the new entity will likely be network integration, brand rationalization, and customer migration. Running two separate billing systems, two separate customer service organizations, and two separate network management platforms costs money. Stonepeak will push for consolidation.

The GFiber brand has significant equity - it scores higher on customer satisfaction surveys than almost any cable operator in markets where it competes. Astound's brands (Wave, RCN, Grande) are less distinctive. The most likely outcome is a gradual migration toward the GFiber brand identity for the combined entity's premium fiber services, while the Astound legacy cable infrastructure continues under existing branding until it can be upgraded.

Longer term, the combined entity could be an attractive IPO candidate or acquisition target. A national independent fiber platform with over one million subscribers, premium brand positioning, and institutional backing is exactly the kind of asset that a larger telecom - or another infrastructure fund - might want in five to seven years. Stonepeak's typical investment horizon is 10-15 years, but exits happen earlier when the price is right.

The question that lingers is whether the combined entity will continue GFiber's tradition of genuine disruption - building in markets where incumbents are underperforming, pricing aggressively, and forcing competition - or whether it will settle into the comfortable oligopoly dynamics that characterize most of the US broadband market. Infrastructure funds don't have the same appetite for below-cost market entry that a trillion-dollar tech company subsidizing disruption as a brand strategy can afford.

Google Fiber forced the US internet industry to be better. The company that emerges from this deal will be judged by whether it continues that mission or quietly becomes another regional cable operator with better marketing.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram