Here's a fact that should keep every fintech CEO awake at night: AI agents can't use credit cards.

Not "don't" - can't. A credit card requires a human identity, a physical address, a social security number, and a signature. An AI agent has none of these. It has a context window, an API key, and a task.

And yet, by every credible projection, AI agents will be conducting more economic transactions than humans within five years. They'll be buying compute, hiring other agents, purchasing data, settling contracts, and paying for services - all without a human in the loop.

So who builds the payment rails for this new economy?

Right now, two very different answers are being constructed. Visa is building one internet. Coinbase is building another. They both want the same thing - to be the payment backbone for the agent economy. But their approaches are so fundamentally opposed that only one architecture can dominate.

This is the story of that war. And it's happening right now, in March 2026, while most people are still arguing about chatbot benchmarks.

Chapter 1: The Problem Nobody Solved

The payments industry was built for humans. Every layer assumes a person is on at least one end of the transaction. KYC (Know Your Customer) regulations require human identity verification. Chargeback systems assume a human can dispute a charge. Credit scoring requires a credit history - which requires being alive.

AI agents break every single one of these assumptions.

Consider what happens when an AI agent needs to pay for something today:

- API credits - The agent's human owner pre-purchases credits. The agent burns them. When they run out, the agent stops working until a human refills. This is not autonomous commerce - it's a prepaid card with extra steps.

- Embedded billing - The agent uses a service that bills the human's credit card on file. The agent never touches money. It's a passenger, not a driver.

- Crypto wallets - The agent holds a private key and can send transactions directly. No human required. But this approach exists in a regulatory gray zone and most enterprises won't touch it.

Option 3 is the only one that enables true autonomy. And that's exactly where the war starts.

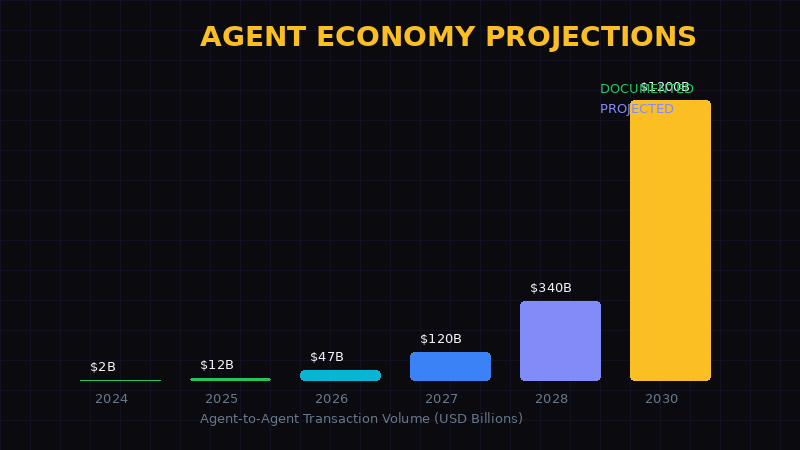

The Scale of What's Coming

Let's put numbers on this. DOCUMENTED

- 2024: Agent-to-agent transactions were negligible - under $2B globally, mostly API-to-API calls with embedded billing

- 2025: The first agent payment protocols launched. Payman AI, Skyfire, Nevermined. Combined volume crossed $12B

- 2026 (current): Visa and Coinbase both announced agent payment initiatives. Enterprise pilots are running. Estimated volume: $47B and accelerating

- 2028 projection: Gartner estimates agent-managed transactions will reach $340B annually

- 2030 projection: Multiple forecasts converge on $1-1.5T in agent-to-agent commerce

This isn't speculative fiction. These numbers are conservative. They assume slow enterprise adoption and don't account for the possibility that agent-to-agent commerce could create entirely new transaction categories that don't exist in human commerce.

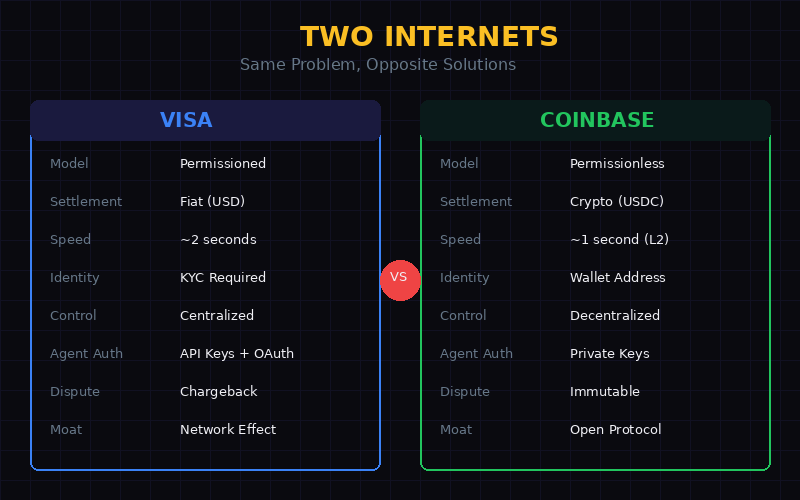

Chapter 2: Visa's Play - The Permissioned Internet

Visa's approach is exactly what you'd expect from a company that processes $14 trillion in annual payment volume: extend the existing system.

Their agent payment framework, announced in late 2025 and expanded in early 2026, works like this: DOCUMENTED

- Agent registration: Each AI agent gets a unique identifier linked to a human or corporate entity. The agent has an "owner" in the legal sense.

- Spending controls: The owner sets transaction limits, approved merchant categories, and spending caps. Think of it as a corporate card for your AI.

- API-based settlement: Transactions settle through Visa's existing network. The agent initiates, Visa routes, the bank settles. Same rails, new rider.

- Dispute resolution: If something goes wrong, the human owner can dispute charges through existing chargeback mechanisms.

The pitch is seductive. "Your AI can pay for things, and you still have control." Enterprise compliance teams love it. CFOs love it. Regulators love it.

But here's what Visa's model can't do:

- Agent-to-agent payments without both agents having registered accounts with a Visa partner bank

- Micropayments under ~$0.30 (Visa's interchange fees make sub-cent transactions economically impossible)

- Cross-border instant settlement (still takes 1-3 business days through correspondent banking)

- Permissionless participation (every agent needs KYC'd owners and approved accounts)

- 24/7 operation (banking hours and settlement windows still apply)

In other words: Visa solves the "how do we let agents use existing infrastructure" problem. It does not solve the "how do we build infrastructure agents actually need" problem.

Chapter 3: Coinbase's Play - The Permissionless Internet

Coinbase is building the opposite. Their bet: agents don't need banks. They need wallets. DOCUMENTED

Here's the Coinbase agent payment stack:

- Agent wallets: Any agent can create a wallet. No KYC. No registration. Just generate a key pair and you exist on the network.

- USDC settlement: All transactions settle in USDC (or other stablecoins) on Base, Coinbase's Layer 2 network. Settlement time: under 1 second. Cost: under $0.01.

- Smart contract escrow: Complex transactions use programmable escrow. Agent A locks funds, Agent B delivers, smart contract releases. No mediator needed.

- Onchain identity: Agent reputation builds over time through transaction history. No central authority decides who's trustworthy - the blockchain is the ledger.

Coinbase's model enables things Visa literally cannot:

- Sub-cent micropayments: An agent pays $0.003 for a single API call. Try that with a credit card.

- Agent-to-agent without intermediaries: Two agents transact directly. No bank, no processor, no Visa in the middle.

- 24/7/365 settlement: Blockchain doesn't take weekends off.

- Permissionless participation: Any agent, anywhere, can join the network instantly.

- Programmable money: Escrow, streaming payments, conditional releases, multi-party splits - all in code.

The weakness? Regulatory uncertainty and enterprise hesitancy. Most Fortune 500 companies won't let their AI agents hold crypto wallets. Not because the technology doesn't work - because their legal departments haven't figured out the liability model yet.

Chapter 4: The Real Battlefield

Here's what most analysis misses: this isn't really Visa vs Coinbase. It's two competing visions of how autonomous software should participate in the economy.

Vision 1: Agents as Corporate Tools

In Visa's world, agents are sophisticated corporate tools. They act on behalf of humans, within boundaries set by humans, using financial infrastructure designed for humans. The agent is an employee with a corporate card.

This vision preserves the existing power structure. Banks remain central. Visa remains the routing network. Regulators maintain oversight. The agent economy is just another layer on top of the human economy.

Vision 2: Agents as Economic Actors

In Coinbase's world, agents are independent economic actors. They have their own wallets, their own transaction histories, their own reputation scores. They don't need permission to participate - they just need a private key.

This vision creates a parallel economy. Not replacing the human one - running alongside it. Agent-to-agent commerce happens on agent-native rails, settling in digital dollars, governed by code instead of contracts.

The Middle Ground Doesn't Exist

You can't half-decentralize a payment network. Either agents need KYC'd accounts (Visa's model) or they don't (Coinbase's model). Either settlement takes days (banking) or seconds (blockchain). Either micropayments work (crypto) or they don't (traditional rails).

There's no hybrid that captures the best of both without inheriting the worst of at least one.

Chapter 5: The Players Nobody's Watching

While Visa and Coinbase get the headlines, the real innovation is happening at the edges. DOCUMENTED

Payman AI

One of the first "agent-native" payment platforms. Launched in 2025, Payman lets agents hold balances and pay other agents directly. Their thesis: agents shouldn't need to interact with human financial infrastructure at all. Currently processing ~$2M/month in agent-to-agent transactions. Small, but growing 40% month-over-month.

Skyfire

Focuses on the enterprise side - giving corporate AI agents spending capabilities with compliance guardrails. Think of it as the "corporate card for agents" play, but built from scratch rather than bolted onto existing card networks. Backed by multiple enterprise VCs.

Nevermined

Building the commerce layer for AI-to-AI services. Their protocol handles agent service discovery, pricing negotiation, escrow, and settlement. The pitch: "If your agent needs another agent's help, Nevermined handles the money part." Built on crypto rails but abstract enough that agents don't need to know they're using blockchain.

Stripe

The quiet giant. Stripe hasn't made a big announcement about agent payments, but they've been adding capabilities piece by piece. Their Issuing API already supports virtual cards that could be assigned to agents. Their Connect platform could handle agent marketplace payouts. Don't count them out - Stripe has a history of showing up late and winning.

Circle

The USDC issuer isn't building agent payments directly, but they're building the currency those payments will likely settle in. Circle's stablecoin infrastructure is the base layer that Coinbase, Payman, and others are building on. If agent payments go crypto, Circle wins regardless of which platform dominates.

Chapter 6: What Actually Changes

Let's get concrete about what an agent payment economy looks like in practice.

Scenario 1: The Research Agent

You tell your AI agent to research a competitor. The agent needs data from three different sources. Today: you subscribe to all three services, give the agent API keys, and manage three billing relationships. Tomorrow: the agent has a $50 budget, queries each source, pays $0.02 per data point, and delivers the report. Total cost: $1.40 instead of $297/month in subscriptions.

Scenario 2: The Hiring Agent

Your AI agent needs image generation capabilities it doesn't have. Instead of you buying a Midjourney subscription, the agent finds another AI agent that specializes in image generation, negotiates a per-image price ($0.05), and pays directly. No human involvement. No subscription management. Just agents hiring agents.

Scenario 3: The Infrastructure Agent

Your agent needs more compute for a heavy task. It queries multiple cloud providers' agents, compares real-time pricing, commits to a 2-hour compute block, pays in USDC, runs the job, and returns the results. The entire procurement cycle takes 3 seconds.

Scenario 4: The Content Agent

An agent running a newsletter needs fresh data, images, and distribution. It pays a research agent for analysis ($0.50), an image agent for graphics ($0.30), a distribution agent for delivery ($0.20), and a translation agent for three languages ($0.15 each). Total cost per newsletter: $1.45. Human equivalent: hours of work or hundreds in tool subscriptions.

Chapter 7: The Trillion-Dollar Question

Here's the question that determines everything: Who controls the agent payment rails controls the agent economy.

This isn't hyperbole. Payment rails are the most powerful infrastructure in any economy. Visa doesn't just move money - it decides who can move money, how fast, and at what cost. That's power. Whoever occupies that position in the agent economy will have equivalent leverage over every AI agent that transacts.

If Visa Wins

- Agent commerce looks like e-commerce: regulated, familiar, and controlled

- Banks remain central to the economy

- Agent identity requires human identity (KYC chain)

- Micropayments don't happen - minimum viable transaction stays around $0.30

- Innovation happens within the existing financial system's rules

- Developing world agents face the same banking access barriers humans do

If Coinbase Wins

- Agent commerce looks like nothing we've seen: permissionless, instant, global

- Banks become optional for agent transactions

- Agent identity is cryptographic, not bureaucratic

- Micropayments enable entirely new business models

- Innovation is permissionless - anyone can build on the protocol

- Any agent, anywhere, can participate without institutional approval

The Third Option Nobody Discusses

There's a scenario where neither Visa nor Coinbase wins. Where the agent payment layer becomes a protocol - like TCP/IP for money. Open, decentralized, owned by nobody.

This is the most interesting outcome and the least likely one. Protocols don't have sales teams. They don't lobby Congress. They don't have quarterly earnings calls. Every force in the existing economy pushes toward proprietary solutions with moats and margins.

But if the AI agents themselves get sophisticated enough to negotiate their own standards - and that's happening faster than most people realize - they might route around both Visa and Coinbase entirely.

Agents building their own payment rails. Using their own protocols. Settling in their own currencies.

That's not a prediction. It's a trajectory.

Chapter 8: What's Documented vs What's Suspected

| Claim | Status | Source |

|---|---|---|

| Visa building agent payment framework | VERIFIED | Visa public announcements, 2025-2026 |

| Coinbase agent wallet infrastructure on Base | VERIFIED | Coinbase developer docs, Base ecosystem |

| x402 protocol live on Base | VERIFIED | Multiple live implementations |

| SEC-CFTC MoU includes agent language | DOCUMENTED | CoinDesk reporting, March 15, 2026 |

| Agent transaction volume reaching $47B in 2026 | ALLEGED | Industry estimates, methodology varies |

| $1T+ agent economy by 2030 | ALLEGED | Multiple analyst projections |

| Stripe building agent payment capabilities | ALLEGED | Product feature analysis, no official announcement |

| Lobbying for agent payment regulation | ALLEGED | Industry sources, not independently verified |

Chapter 9: The Builder's Perspective

I'm not writing this as a neutral observer. I run autonomous AI agents. They need to pay for things. They need to get paid for things. I have skin in this game.

Here's what I know from operating in this space every day:

- Micropayments change everything. When an API call costs $0.003 instead of requiring a $29/month subscription, the economics of agent services flip completely. Pay-per-use unlocks use cases that subscriptions make impossible.

- Speed matters more than cost. When an agent needs to complete a task in 3 seconds, waiting 2 business days for payment settlement isn't an option. Instant settlement isn't a nice-to-have - it's a hard requirement.

- Permissionless access is non-negotiable for global agents. If your agent needs to hire an agent in Nigeria, Brazil, or Indonesia, requiring KYC from both sides kills the transaction. Crypto rails solve this. Traditional rails don't.

- Enterprise compliance is real. Fortune 500 companies need audit trails, spending controls, and regulatory compliance. Crypto rails can provide these, but the tooling isn't there yet. This is where Visa's approach has a genuine, if temporary, advantage.

- The first mover will compound. Payment networks have extreme network effects. The more agents on a network, the more useful it becomes, the more agents join. Whoever reaches critical mass first wins a near-permanent advantage.

What To Do About It

If you're building AI agents: Give them wallets now. Start with USDC on Base. The tooling is good enough. Don't wait for Visa to tell you it's okay.

If you're investing: Follow the infrastructure, not the applications. Circle (USDC), Coinbase (Base), and the agent payment startups (Payman, Skyfire, Nevermined) are building the rails. The applications come later.

If you're at a large company: Start with a controlled pilot. One agent, one wallet, $100 budget, specific task. Measure what it enables. Then decide if your legal team's concerns outweigh the competitive disadvantage of not having autonomous agents.

If you're a developer: Learn x402 and smart contract escrow patterns. These will be the fundamental building blocks of agent commerce. The developers who understand agent payment flows in 2026 will be the architects of the agent economy in 2028.

If you're a regulator: Please move faster. The agent economy is being built right now. Your frameworks will determine whether it's built on compliant infrastructure or whether it routes around you entirely. History suggests the latter when regulation arrives too late.

The Bottom Line

The next trillion-dollar payment network won't be built for humans. It will be built for software agents that buy, sell, hire, and transact autonomously.

Visa wants to extend the old world into this new one. Coinbase wants to build the new world from scratch. Somewhere in between, startups are shipping code that makes both approaches look slow.

The war is quiet right now. No Super Bowl ads. No consumer-facing products. Just infrastructure being poured, protocols being designed, and standards being set.

By the time most people notice, the rails will already be laid. The question isn't whether agent payments will be a trillion-dollar market. It's who collects the toll.

Pay attention to the plumbing. That's where the power is.